An accounting measure of future tax consequences arising from temporary differences between a company's financial accounting income and its taxable income.

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

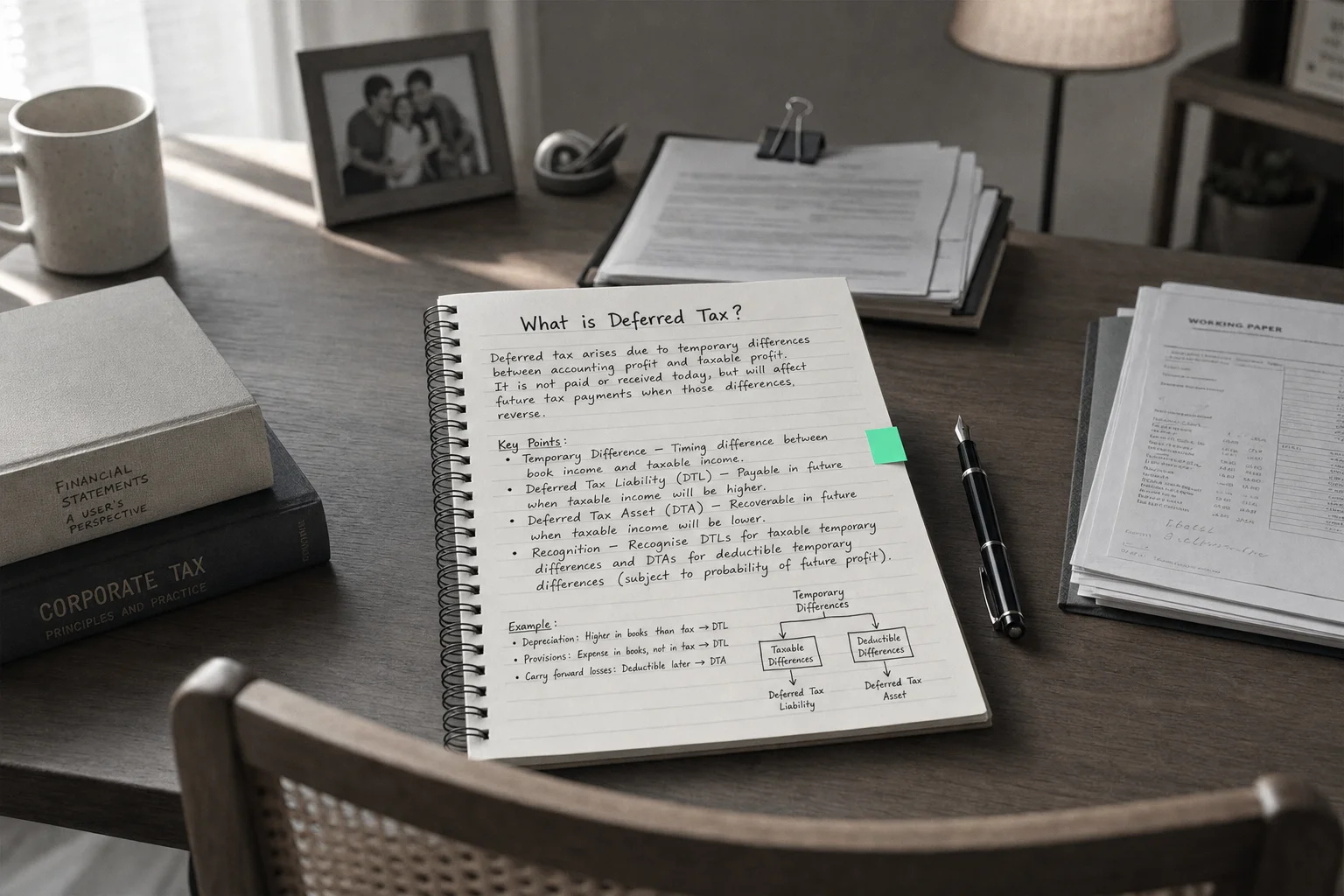

Deferred tax is an accounting concept that arises from the temporary differences between the profit a company reports on its financial statements and the profit it reports to tax authorities. Because income and expenses can be recognized in different periods for accounting versus tax purposes, deferred tax accounts for these timing discrepancies. It is a non-cash item that represents a company’s future tax obligations or benefits.

Deferred Tax Assets vs. Deferred Tax Liabilities

Depending on the nature of the temporary difference, a company records either a deferred tax asset or a liability:

- Deferred Tax Asset (DTA): Represents a future tax benefit. This occurs when a company pays more tax now than it reports as an expense on its income statement. For example, if an expense is recognized for accounting purposes now but is only tax-deductible later, a DTA is created. It’s like a prepayment of tax.

- Deferred Tax Liability (DTL): Represents a future tax obligation. This occurs when a company pays less tax now than it reports as an expense. For example, using accelerated depreciation for tax purposes while using straight-line for accounting creates a DTL. The company saves cash on taxes today but will have to pay more in the future.

How Deferred Tax is Treated on the Cash Flow Statement

Deferred tax adjustments appear in the Operating Activities section of the cash flow statement (under the indirect method). Since deferred tax is a non-cash item, it must be adjusted for to reconcile net income to actual cash from operations.

The Rule for Adjustments

This adjustment ensures that operating cash flow reflects the actual cash taxes paid, not the accrual-based tax expense from the income statement.

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Why This Adjustment Matters for Analysis

Understanding the deferred tax line is crucial for gaining a complete view of a company’s performance and future obligations.

- Bridges Net Income and Cash Flow: The adjustment clarifies how much of the reported tax expense was a non-cash accrual, giving a truer picture of cash generated from operations.

- Indicates Future Tax Impacts: A growing Deferred Tax Liability signals that a company has benefited from lower taxes now but will face higher cash tax payments in the future. A growing Deferred Tax Asset suggests the opposite—the company has prepaid taxes and can expect lower cash tax payments ahead.

- Highlights Tax Strategies: The deferred tax line reveals the impact of different accounting and tax rules. It can signal whether a company is using tax strategies, like accelerated depreciation, to defer tax payments and manage its cash flow.

Presentation on the Cash Flow Statement

In a real-world cash flow statement, this adjustment is typically labeled “Deferred income taxes” and is listed among other non-cash items in the operating section.

Sample Presentation

Cash flows from operating activities:

Net income: 26,863 Amortization: 157** Stock-based compensation: $8,787

In this example, the $157 (in thousands) for deferred income taxes is added back to net income, indicating it was a non-cash expense that reduced reported profit.

Example: General Motors

In 2013, GM’s cash flow statement showed a ‘provision for deferred taxes’ of (35,561) million, which was subtracted. The large negative figure in 2012 reflected a non-cash benefit that boosted net income, so it had to be removed to calculate actual cash flow.