Operating Income is a financial concept covered in this article. A Measure of Profit from Core Business Operations

The stock market is a device for transferring money from the impatient to the patient.

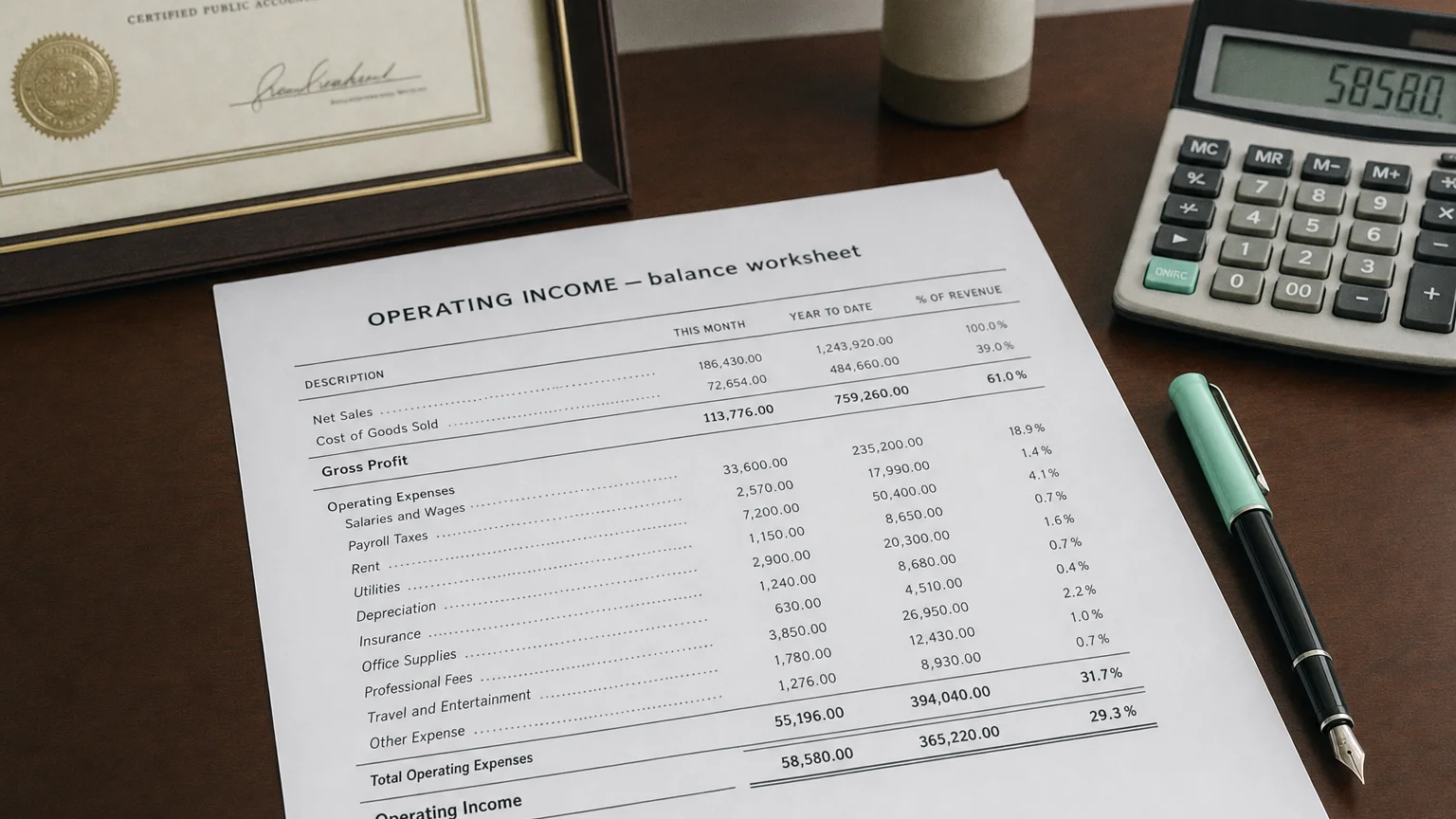

Operating income (also known as operating profit or income from operations) is the profit a company earns from its core business activities after covering all operating costs. In other words, it equals a company’s operating revenue minus its operating expenses. This figure appears as a subtotal on the income statement—before interest, taxes, and other non-operating items are deducted. Operating income represents earnings from normal business operations and excludes any income or expenses from unusual or non-core activities.

How Is Operating Income Calculated?

Operating income is calculated by subtracting all of the expenses of running the business (beyond direct production costs) from the profit earned on sales.

Formula: Operating Income = Gross Profit - Operating Expenses

This can also be expressed by starting from the top of the income statement:

Formula: Operating Income = Revenue - Cost of Goods Sold (COGS) - Operating Expenses

Also Known as EBIT

Because interest payments and taxes are not counted as operating expenses, they are excluded from this calculation. For this reason, operating income is often referred to as EBIT (Earnings Before Interest and Taxes), assuming there are no other non-operating income or expense items.

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Annual Report (1999)

Why Operating Income Is Important

Operating income is a key metric in financial analysis for several reasons:

- Core Profitability: It measures the profit from a company’s core operations, stripping out factors like financing costs and taxes. This makes it a clear indicator of operational efficiency and business health.

- Comparability: Since it excludes interest and taxes, operating income allows analysts and investors to compare companies’ performance on an “apples to apples” basis, regardless of their financing decisions or tax environments.

- Trend Analysis: Management watches operating income over time to evaluate if core business performance is improving or declining. This helps in identifying when cost controls or strategic changes are needed.

- Investor Confidence: It demonstrates how much earnings the business can produce from its regular activities. Consistently positive operating income indicates a potentially sustainable business model.

Operating Income vs. Gross Profit vs. Net Income

Operating income is one of three key profit measures on the income statement, each showing a different level of profitability:

- Gross Profit: This is Revenue - COGS. It shows profit after direct production costs but before any other operating expenses like salaries or rent. It is the highest level of profit.

- Operating Income: This is Gross Profit - Operating Expenses. It shows the profit from core operations after all regular business costs (like salaries, rent, and depreciation) are subtracted. It is more comprehensive than gross profit and sits in the middle of the income statement.

- Net Income: This is Operating Income - (Interest + Taxes + Other non-operating items). This is the “bottom line” final profit after all expenses of any kind have been accounted for. It is the ultimate measure of overall profitability.

Example of Operating Income Calculation

To illustrate, consider a simple income statement for a company:

Income Statement Data

Using the formula, the Operating Income would be calculated as:

Formula: 50,000 (COGS) - 10,000 (D&A) = $15,000

This **15,000 from its core activities. This is the amount available to cover interest and taxes.

Q · 01What is Operating Income?+