An exploration of the miscellaneous long-term assets on the balance sheet that don't fit into standard categories like PP&E or Intangibles.

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

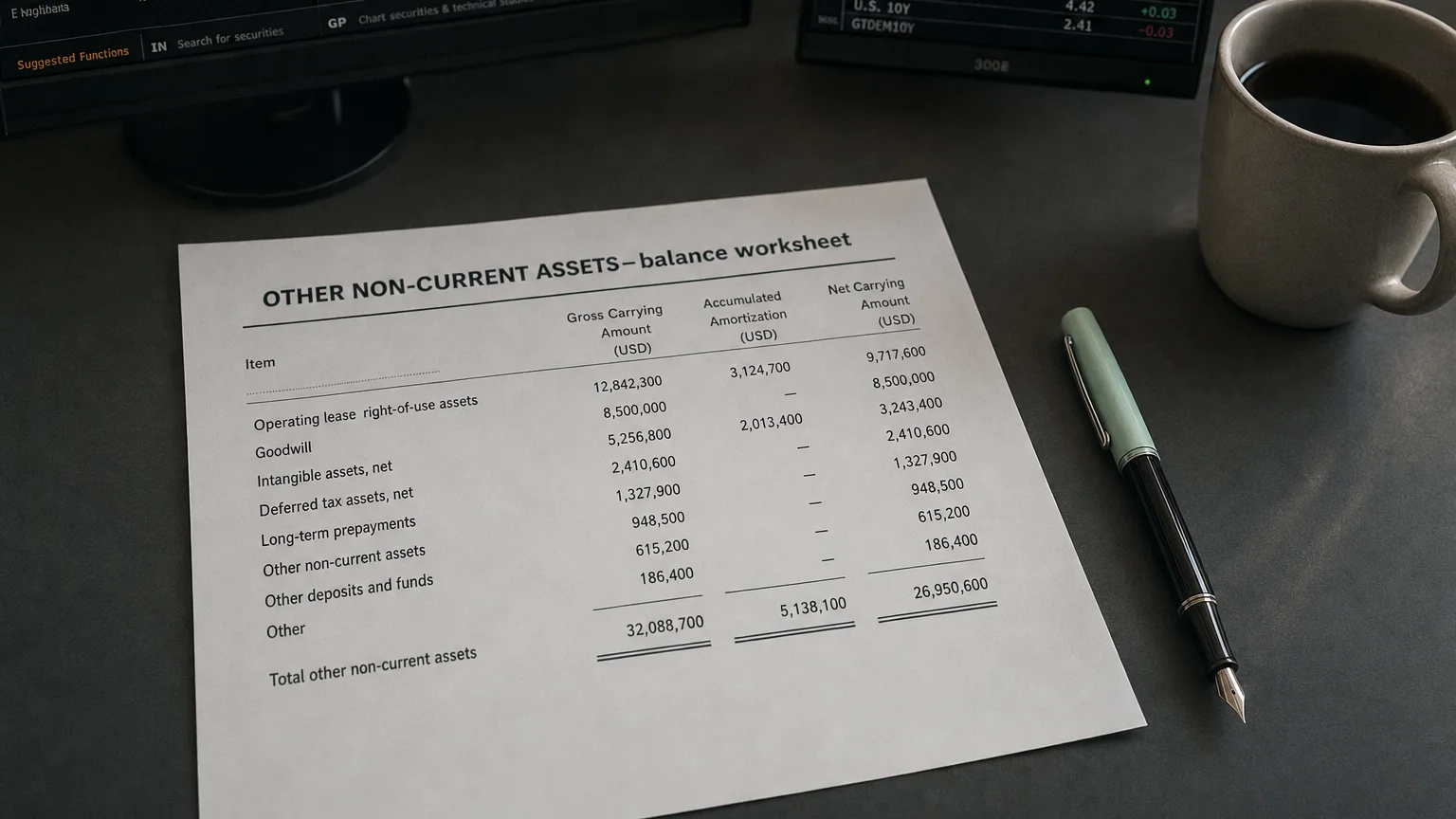

Other Non-Current Assets (sometimes called “other long-term assets”) are a catch-all category for long-term assets that do not fit into the standard non-current asset categories like property, plant & equipment (PPE), intangible assets, or long-term investments. In other words, after listing major non-current assets, any remaining long-term assets are grouped here. This ensures all assets with future economic benefits beyond one year are captured on the balance sheet. These assets are by nature illiquid and not expected to be converted to cash within the next year.

What Belongs in Other Non-Current Assets?

This category can include a wide variety of items that are long-term in nature but don’t belong elsewhere. Common examples include:

- Deferred Tax Assets: Future tax benefits from tax overpayments or losses that can offset future tax bills. The portion realizable beyond one year is non-current.

- Long-Term Prepaid Expenses: Advance payments for services that will be received over multiple years, such as a 3-year insurance policy.

- Long-Term Receivables or Loans: Amounts owed to the company that are not due within one year, like multi-year notes receivable from customers or employees.

- Security Deposits: Deposits paid to landlords or suppliers that will be held for more than a year.

- Cash Surrender Value of Life Insurance: The value a company can obtain by canceling a key-person life insurance policy it owns.

- Unamortized Deferred Costs: Costs paid upfront that are expensed over multiple future periods, such as fees incurred to issue long-term bonds.

- Idle or Surplus Assets: Tangible assets, like land or equipment, that are not currently used in operations and are not actively being marketed for sale.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Key Distinctions from Other Asset Categories

To properly analyze a balance sheet, it’s crucial to understand how this ‘other’ category differs from the main asset groups.

- Versus Current Assets: The primary difference is the time horizon. Current assets support day-to-day operations and are expected to be used or converted to cash within one year. Other Non-Current Assets are illiquid and tied up for longer than a year, so they are excluded from liquidity measures like the current ratio.

- Versus Fixed Assets (PPE): PPE includes tangible assets actively used in operations, like buildings and machinery. Other Non-Current Assets is for items outside of these core operational assets. For example, a dormant piece of equipment awaiting a future use would be in ‘other assets,’ not PPE.

- Versus Intangible Assets: Major intangibles like goodwill or significant patents are listed separately. This ‘other’ category is for miscellaneous or minor intangibles that don’t warrant their own line item. It is a residual category for what’s left over.

Relevance in Financial Analysis

While often smaller than primary asset categories, Other Non-Current Assets are still important for a complete picture of a company’s financial position.

A Potential Red Flag

A large or rapidly growing balance in Other Non-Current Assets can be a red flag for analysts. Because the line item aggregates miscellaneous items, a significant balance requires investors to look to the footnote disclosures to understand what’s inside and assess its quality.

Understanding the components is crucial. Some items, like a deferred tax asset, signal future cash savings and are high-quality. Others, like an idle asset, might be questionable and risk being written off. In financial modeling and valuation, analysts must decide whether to include these assets in measures like Return on Assets (ROA), often excluding non-operating items to get a clearer picture of core operational efficiency.

Ultimately, analyzing this category helps investors understand where a company is deploying cash for the long-term and assess the quality of those assets in supporting future performance.

Q · 01What is Other Non-Current Assets?+