Preferred Stock Issuance is a financial concept covered in this article. Cash Inflows from Issuing New Preferred Shares

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

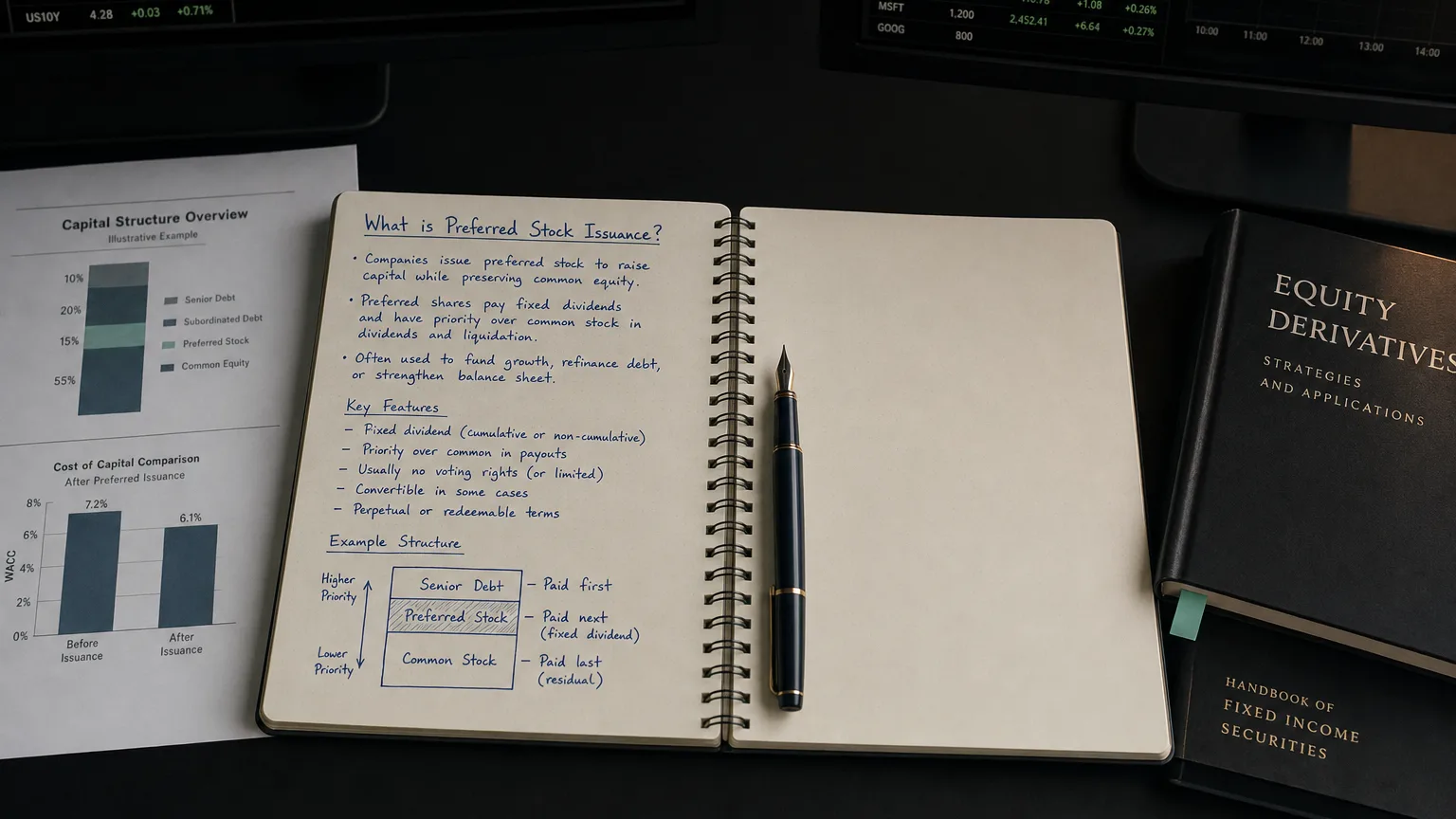

Preferred Stock Issuance represents the cash proceeds a company receives when it issues new preferred shares to investors. This inflow appears in the financing section of the cash flow statement, reflecting a capital-raising transaction where the company sells senior equity claims (preferred dividends and liquidation priority) without diluting common voting control.

What It Represents

Preferred Stock Issuance is the cash the company brings in by selling new preferred shares.

- New primary issuance (not secondary trading)

- Proceeds at issue price (often par + premium)

- No repayment obligation (equity, not debt)

- Creates fixed dividend commitment

It’s a way to raise permanent capital with priority over common but less dilution of control.

Does not include conversions or employee exercises.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

A Simple Example

Company wants $100M without issuing more common shares or taking debt.

- Issues $100M new 6% preferred stock at par

- Receives $100M cash from investors

- Cash flow statement: +$100M Preferred Stock Issuance

- Later redeems 40M Preferred Stock Payments

- Net Preferred Stock Issuance: +$60M

Raised capital with predictable dividend cost.

Common Reasons for Issuance

- Raise growth or acquisition capital

- Refinance existing preferred or debt

- Strengthen balance sheet (equity counts for ratios)

- Appeal to income-focused investors

- Avoid common dilution/voting changes

- Hybrid capital for regulatory purposes (banks)

Accounting and Presentation

- Cash inflow in financing activities

- Labeled ‘Preferred Stock Issuance’ or ‘Proceeds from Preferred Stock’

- Par/face value to Preferred Stock account

- Premium to Additional Paid-In Capital

- No interest expense (unlike debt)

Mandatorily redeemable preferred may be classified as liability.

Impact on Capital Structure

- Increases total equity

- Adds senior claim (preferred dividends first)

- No maturity/re-payment (perpetual unless callable)

- Fixed dividend obligation reduces flexibility

- May improve debt ratios (counts as equity)

What to Watch For

- Size relative to existing preferred (growing burden?)

- Dividend rate vs. alternatives (cost of capital)

- Terms (convertible? callable? cumulative?)

- Net with payments (true capital change)

- Reason (growth vs. refinancing)

Increasing preferred issuance can signal reluctance to dilute common or take debt.