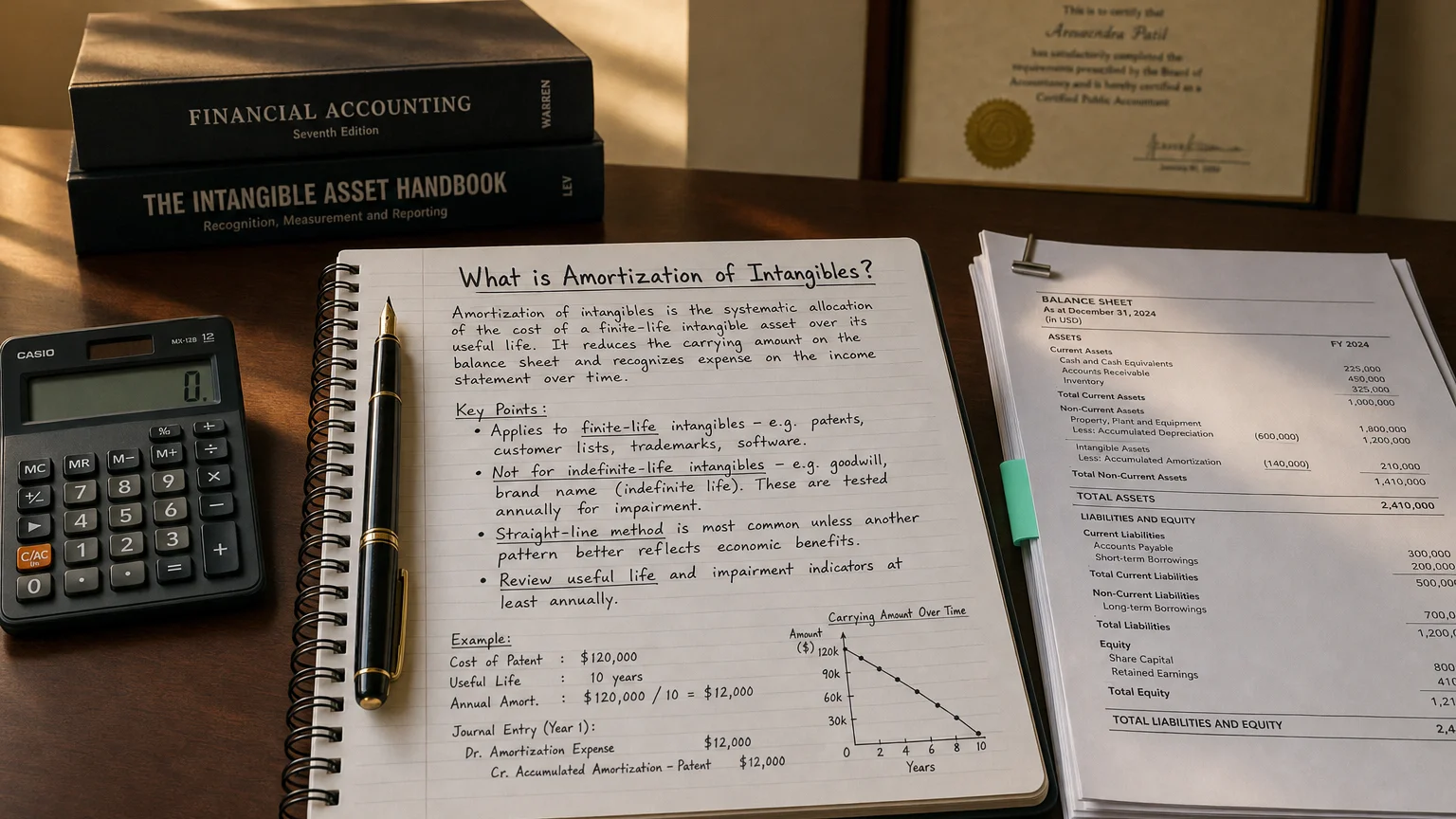

Amortization of intangibles is a non-cash operating expense that allocates the cost of finite-life intangible assets—patents, customer relationships, acquired technology—over their useful lives using the straight-line method.

Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

Amortization of intangibles refers to the periodic expense recorded to systematically allocate the cost of a company’s intangible assets over their useful lives. On the income statement, this appears as an operating expense (often within depreciation/amortization or SG&A expenses) that reduces the company’s reported profit. Below is a comprehensive overview explaining what intangible assets are, what amortization means in this context, why this line item exists, how it’s calculated, and its impact on income and cash flow.

Intangible Assets: Definition and Examples

Intangible assets are non-physical assets owned by a business that have economic value and provide future benefits, even though they cannot be seen or touched. Common examples include patents, trademarks, copyrights, brand names, customer lists, and goodwill (the premium paid during acquisitions). These assets are long-term in nature and are identifiable (meaning they can be sold or transferred separately from the company). Intangibles are recorded on the balance sheet (typically under long-term assets) if acquired or if they have a measurable value, and most are amortized over their useful lives – except for certain indefinite-lived intangibles like goodwill, which are not amortized but tested for impairment instead.

What Is Amortization of Intangibles?

Amortization of intangibles is the accounting process of gradually expensing the capitalized cost (carrying value) of an intangible asset over the asset’s estimated useful life. In other words, rather than taking an upfront one-time expense for an intangible asset’s cost, the company allocates that cost to expense in a structured manner over multiple periods. This is conceptually identical to depreciation (which applies to tangible assets like equipment), except amortization applies to non-physical assets such as patents, trademarks, copyrights, licenses, etc.. Each period’s amortization is reported as amortization expense on the income statement, reducing the company’s revenue in calculating profit. This process only applies to intangibles with finite lives; tangible assets are expensed via depreciation instead.

Purpose of Amortization (Matching Principle)

The amortization line item exists to satisfy the matching principle under accrual accounting – i.e. to match the cost of an asset with the periods that benefit from that asset’s use. If an intangible asset will provide economic benefits over several years, GAAP requires capitalizing it and then recognizing the expense gradually over those years, rather than expensing the full cost immediately. This approach gives a truer picture of profits over time: instead of “dumping” the entire cost into the acquisition year (which would sharply reduce that year’s profit), the cost is spread out so that each period bears a portion of the expense aligned with the revenue or benefit generated by the asset. In essence, amortization ensures costs are matched to the revenue they help produce, providing a more accurate measure of operating performance in each period.

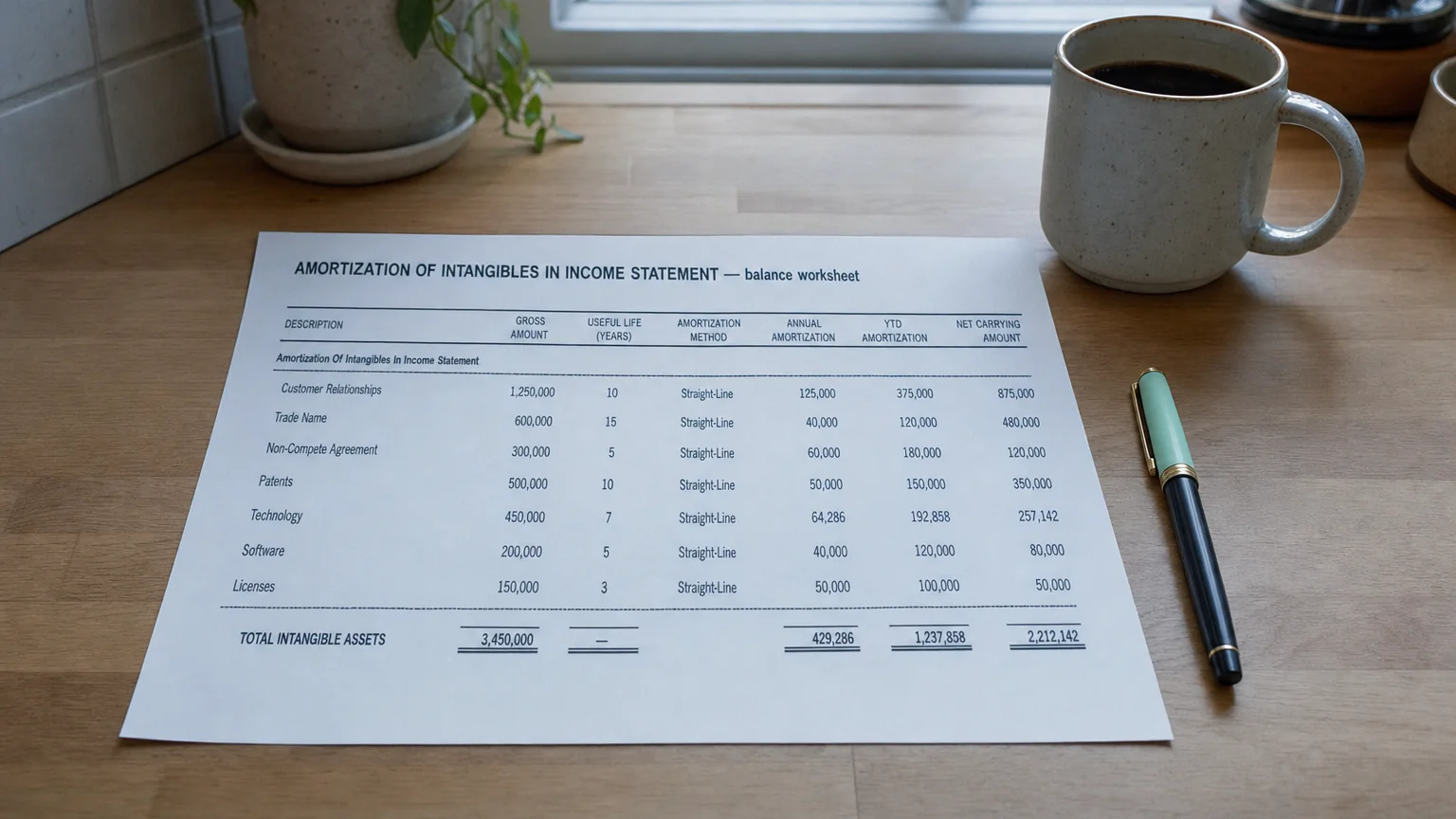

How Amortization of Intangibles Is Calculated

The amortization expense for an intangible asset is typically calculated in a systematic way over the asset’s useful life. In general, companies follow these steps to determine amortization:

-

Determine the asset’s cost: Use the historical cost paid to acquire the intangible (e.g. purchase price of a patent or license).

-

Estimate the useful life: Decide over how many years the asset will provide economic benefit. This is the asset’s finite life (e.g. a patent valid for 20 years may have a useful life of 20 years, or less if obsolescence is expected earlier).

-

Consider residual value (if any): Many intangibles are assumed to have little or no salvage value at the end of their life (unlike some tangible assets).

-

Calculate periodic expense: Apply a suitable amortization method – typically straight-line unless a different usage pattern is more appropriate. The straight-line formula is:

Amortization Expense per period = (Cost – Residual Value) ÷ Useful Life.

Using straight-line amortization, the same amount is expensed each period over the asset’s life. For example, if a company purchased a patent for $28,000 with a 14-year useful life, it would record an amortization expense of $2,000 per year for 14 years (assuming no residual value). This gradual write-off continues until the asset’s carrying value is reduced to zero by the end of its useful life. (If the asset’s benefits are consumed in a non-linear pattern and that pattern can be reliably determined, GAAP allows using an alternative method that reflects the actual consumption of benefits; otherwise, straight-line is used by default.)

Impact on Operating Income and Profitability

On the income statement, amortization of intangibles is recorded as an expense, which means it directly reduces operating income and, ultimately, net income for the period. Companies typically include this expense within the operating expense section – often grouped under Selling, General & Administrative (SG&A) expenses or sometimes in cost of goods sold, depending on the nature of the intangible asset. For instance, amortization of a patent used in manufacturing might be included in production costs (COGS), whereas amortization of a customer list or trademark would likely be part of SG&A. Regardless of classification, it subtracts from operating profit (EBIT), reflecting the periodic cost of using the intangible asset.

Importantly, amortization expense reduces a company’s net income on the income statement, but does not involve an outflow of cash in the current period. The cash outlay typically occurred up front (when acquiring or developing the intangible asset); the amortization entry is an accounting allocation of that past cost. Thus, amortization is a non-cash expense – it lowers reported profit without affecting the company’s cash balance. (It can, however, provide a tax benefit: for tax-reporting purposes, amortization is usually deductible, which reduces taxable income and creates a “tax shield” that lowers actual taxes paid.)

Because it’s non-cash, amortization is added back to net income on the cash flow statement (under operating activities) to reconcile net income to cash flow. In practice, companies often aggregate depreciation and amortization in both their financial statements and analysis. For example, EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a common profitability metric that adds back amortization (and depreciation) to operating earnings specifically because these expenses don’t use cash in the current period. In summary, while amortization reduces accounting earnings (operating income and net profit), it does not directly reduce cash flow. Investors and analysts may therefore look at earnings before amortization to assess operating performance or cash-generating ability, but GAAP net income will include the amortization charge as a real expense.

GAAP Reporting and Presentation

Under U.S. GAAP, intangible assets with finite useful lives are required to be amortized over that estimated life. The amortization method should reflect the pattern in which the asset’s economic benefits are consumed, but if no reliable pattern is determinable, the straight-line method is used by default. Indefinite-lived intangible assets (those with no foreseeable limit to their benefit, such as certain trademarks or acquired franchise rights that can be renewed indefinitely) are not amortized; instead, they must be tested periodically (at least annually) for impairment to see if their value has decreased. Goodwill, a unique intangible arising from business acquisitions, is not amortized under GAAP for publicly traded companies; rather, goodwill is subject to annual impairment tests (private companies have an option to amortize goodwill over a specified period, but this is a GAAP alternative for ease of reporting).

Presentation in financial statements: The amortization expense is usually presented on the income statement within operating expenses. Many firms report it as part of a combined line item “Depreciation and Amortization” (D&A), or include it in SG&A, with additional details provided in the notes. For transparency, companies often disclose the total amortization of intangible assets either on a separate line or in the footnotes, especially if the amount is significant. On the balance sheet, the cumulative amount of amortization taken is reflected through accumulated amortization – a contra-asset account that offsets the gross intangible assets. Thus, intangibles are shown at their net book value (original cost minus accumulated amortization) on the balance sheet. Over time, as amortization expense is recorded each period, the carrying value of the intangible asset declines correspondingly, indicating the asset’s consumed value.

In summary, “Amortization of Intangibles” on the income statement represents the periodic non-cash charge expensing the cost of intangible assets. This expense exists to properly match the cost of intangibles to the revenues they help generate, following GAAP’s accrual principles. It is calculated in a systematic way (often straight-line over the asset’s life) and reported as an operating expense that reduces operating income and net profit. However, because it is a non-cash charge, it does not impact current-period cash flows (aside from its effect of reducing taxable income), and it is added back in cash flow analyses. Properly accounting for amortization of intangibles ensures that a company’s financial statements reflect a realistic allocation of intangible asset costs over time, which helps investors understand the true operating costs and profitability of the business.

Sources:

-

AccountingTools – “Amortization of Intangible Assets” (definition and presentation)

-

Wall Street Prep – “Intangible Assets Amortization” (GAAP treatment and matching principle)

-

TaxRobot – “Definition of Amortization of Intangible Assets” (expense impact on income and cash flow)

-

Patriot Software – “Accounting for Intangible Assets” (amortization calculation example)

-

FASB ASC 350-30-35 (via Deloitte) – (amortization requirements for finite vs. indefinite-lived intangibles)

Q · 01How is intangible amortization calculated?+

Q · 02Where does intangible amortization appear on the income statement?+

Q · 03Why is intangible amortization added back in EBITDA?+