Amortization What It Is and How It Works

Amortization allocates intangible asset costs and debt adjustments over time as a non-cash expense—essential for EBITDA, earnings quality, and M&A analysis.

Overview

Amortization allocates intangible asset costs and debt adjustments over time as a non-cash expense—essential for EBITDA, earnings quality, and M&A analysis.

Amortization in financial statements refers to the gradual allocation of the cost of certain assets over their useful lives as a non-cash expense. It primarily applies to finite-life intangible assets (e.g., patents, copyrights, acquired customer relationships) but can also refer to the amortization of premiums/discounts on debt securities or loan costs. Amortization reduces reported earnings and taxable income while matching the asset's cost to the periods it benefits. As a non-cash charge, it is added back in cash flow analysis and EBITDA calculations, making it essential for understanding earnings quality, cash generation, and the impact of acquisitions or financing decisions.

What is Amortization?

Amortization is the accounting process of spreading the cost of an asset over the periods expected to benefit from its use. It applies mainly to intangible assets with finite lives and certain financial adjustments.

For intangibles, amortization follows the matching principle: expense the cost as the asset generates revenue. For financial items (e.g., bond premiums), it adjusts effective yield.

Unlike goodwill and indefinite-life intangibles (impairment-tested only), finite-life intangibles are systematically amortized under US GAAP (ASC 350) and IFRS (IAS 38).

Amortization is non-cash, reducing earnings but preserving cash—key add-back for cash flow and valuation metrics.

Main Types of Amortization

Amortization covers two primary areas:

Key Categories

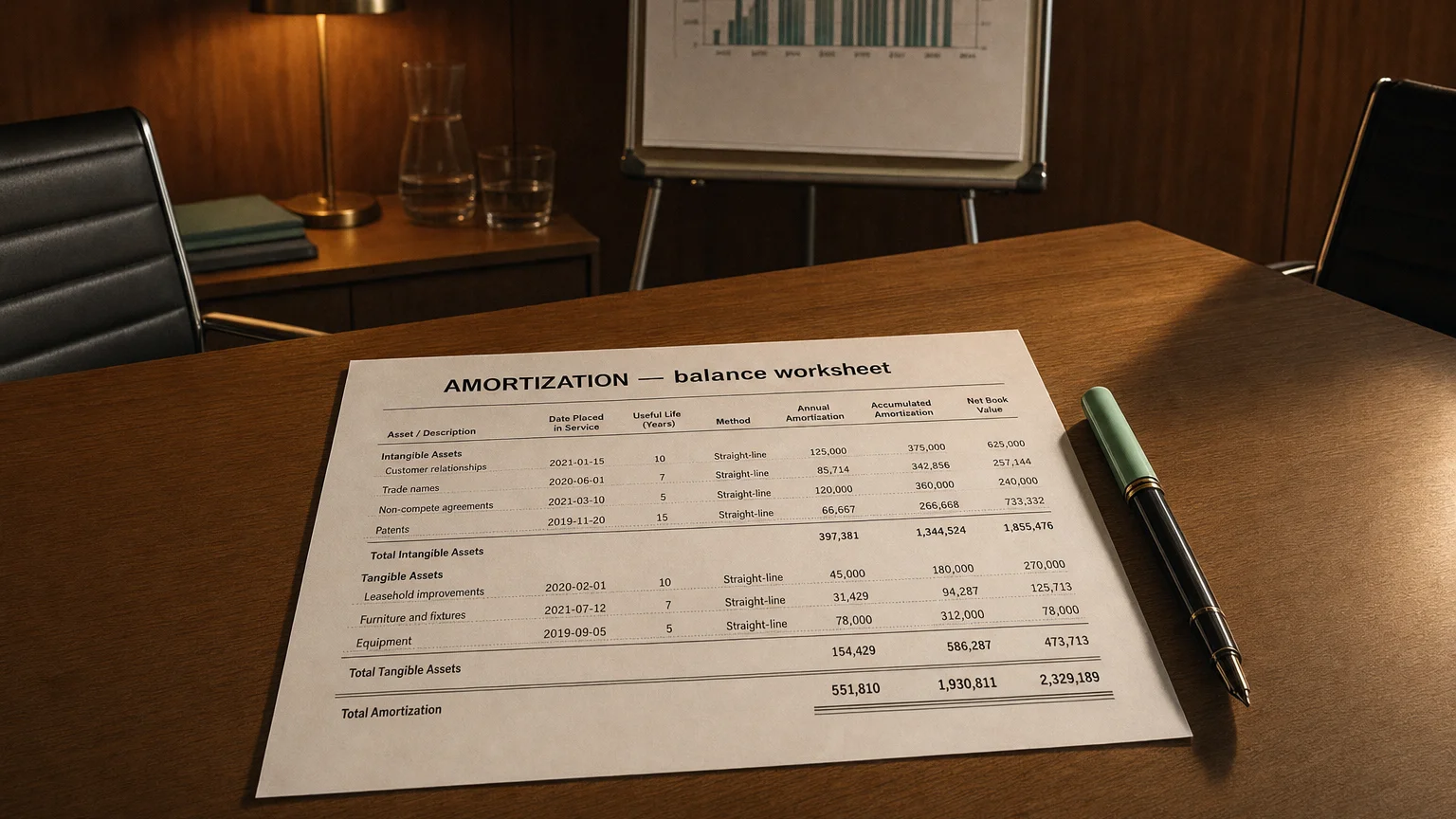

- Intangible Assets: Patents, copyrights, customer lists, software, licenses—straight-line over useful life

- Financial Instruments: Premium/discount on bonds/loans (effective interest method), debt issuance costs

Intangible amortization is operating; financial amortization may be non-operating or interest-related.

"The intelligent investor is a realist who sells to optimists and buys from pessimists."

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

Calculation Methods

For intangibles:

Formula: Annual Amortization = Cost ÷ Useful Life (Residual value usually zero)

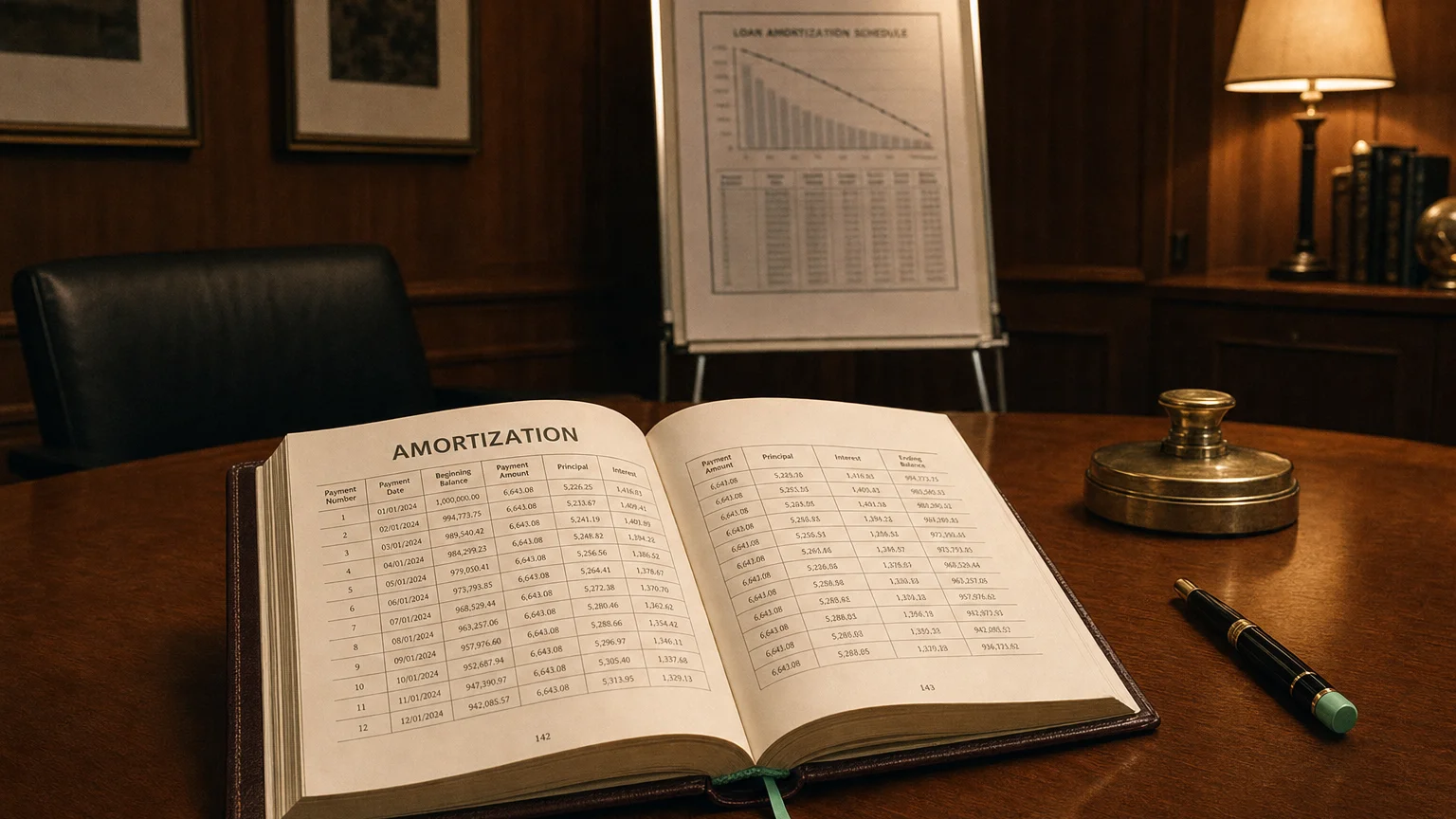

For debt securities/loans: Effective interest method preferred (constant yield).

Useful life = shorter of legal or economic life; reviewed periodically.

Examples

Example 1: Intangible Asset

Acquired patent cost $15M, 10-year life.

Annual Amortization = 1.5M. Expensed in operating expenses.

Example 2: Bond Premium

Bond bought at premium (100 face).

Premium amortized reduces effective interest income over life.

Example 3: Debt Issuance Costs

200K issuance costs.

Amortized over loan term as additional interest expense.

Large amortization often follows acquisitions (identified intangibles).

Presentation in Financial Statements

Amortization appears as:

Common Locations

- Within operating expenses (intangibles)

- In interest expense or non-operating (financial)

- Aggregated in D&A line

Reduces operating income (intangibles) or pretax income (financial).

Importance in Financial Analysis

Amortization matters for:

- EBITDA (add back non-cash)

- Assessing acquisition impact on earnings

- Evaluating intangible-heavy business models

- Understanding effective interest costs

High amortization signals M&A activity or IP reliance; monitor lives for comparability.

Warning: Short lives accelerate expense, pressuring earnings—compare policies across peers.