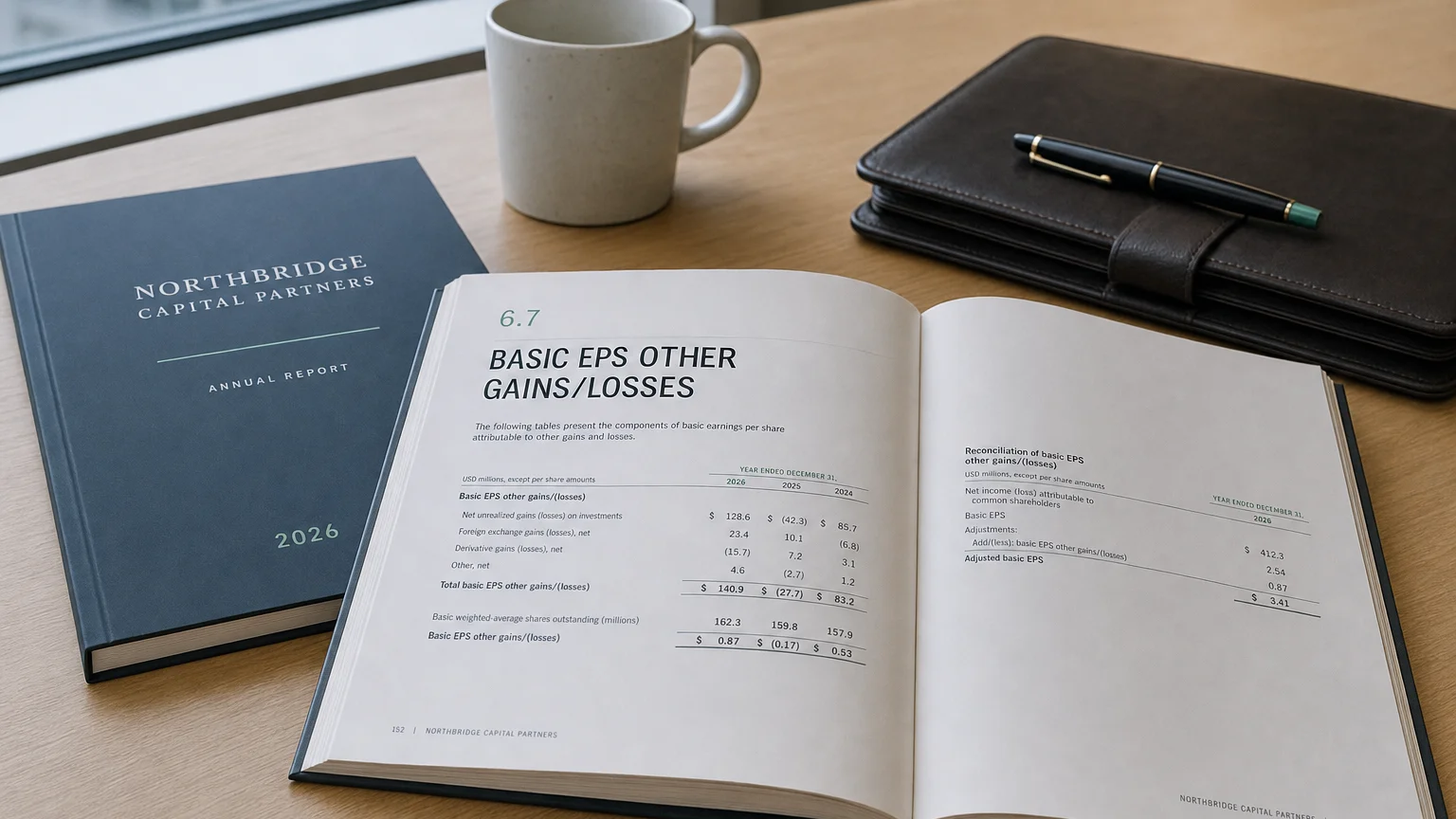

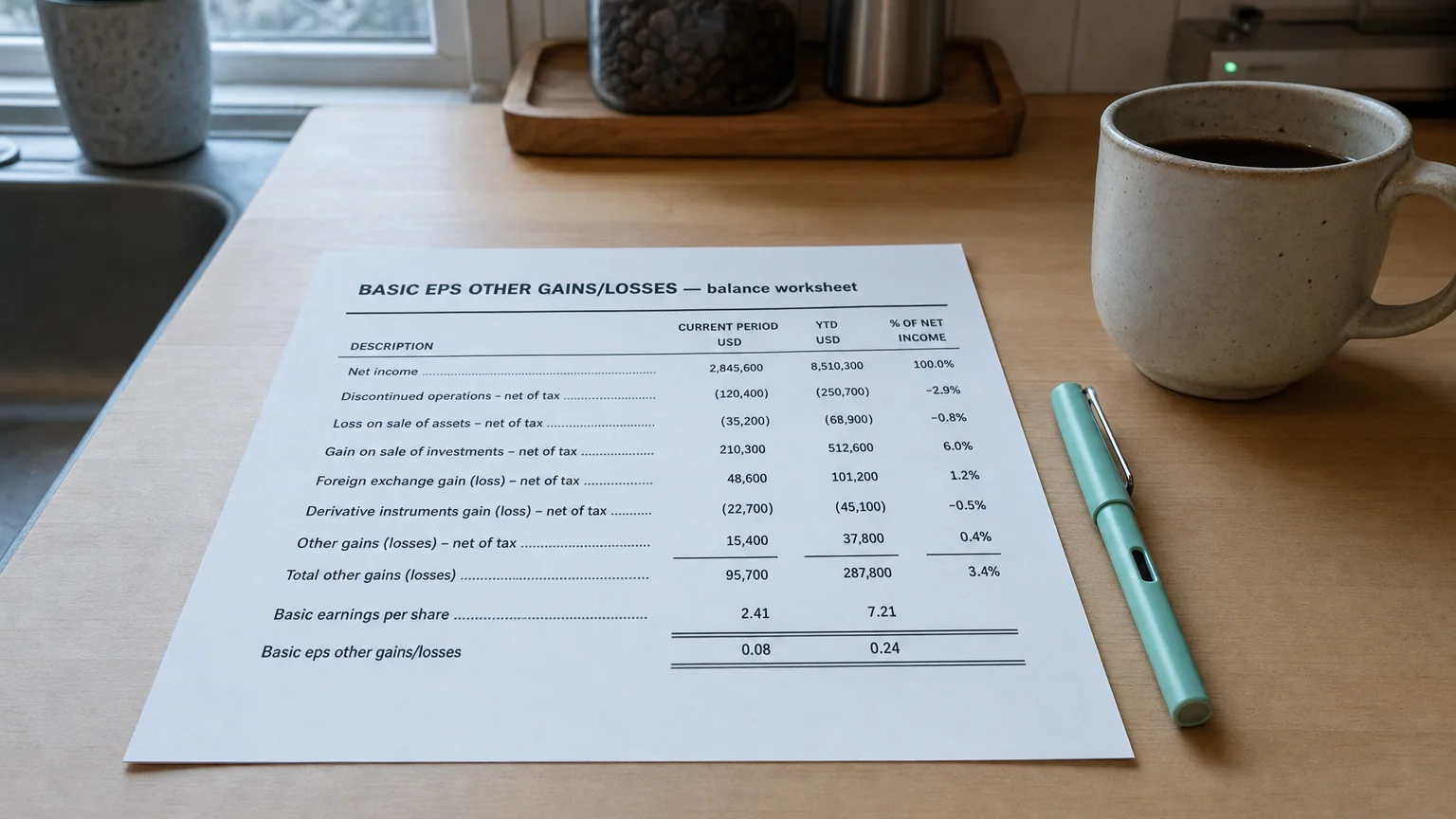

Basic EPS Other Gains/Losses is the basic EPS component from non-operating items—asset sale gains, impairments, and restructuring charges. It equals after-tax gains or losses divided by basic weighted average shares, isolating one-time effects from core earnings.

Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

Basic EPS Other Gains/Losses represents the portion of basic earnings per share (EPS) that stems from non-operating, unusual, or infrequent gains and losses. These include items such as gains or losses on asset sales, impairments, restructuring charges, litigation settlements, and other special income or expense items outside core ongoing operations. This component helps investors and analysts isolate the per-share contribution (or reduction) from one-time or peripheral events to basic EPS, providing clarity on the quality and sustainability of reported earnings without considering potential dilution.

What is Basic EPS Other Gains/Losses?

Basic EPS Other Gains/Losses is a breakdown component in detailed EPS reconciliations that captures the per-share impact of other gains and losses or unusual/special items using the basic weighted average shares outstanding. It excludes any dilution from convertible securities, options, or warrants.

This line reflects the after-tax effect of non-recurring or non-operating transactions on basic EPS, helping explain variances between core operating earnings and total reported basic EPS.

Financial databases and filings often separate EPS into components like continuing operations, discontinued operations, and this ‘other gains/losses’ category for transparency.

How It Is Calculated

The calculation is straightforward within the EPS framework:

Formula: Basic EPS Other Gains/Losses = (After-tax Other/Unusual Gains and Losses) ÷ Basic Weighted Average Shares Outstanding

The after-tax amount is derived as: Pre-tax unusual/special items × (1 − Effective Tax Rate). Basic shares are simply the actual weighted average common shares outstanding during the period.

Typical Items Included

- Gains/losses on sale of assets or investments

- Asset impairments (including goodwill)

- Restructuring and merger costs

- Litigation or settlement charges/gains

- Debt extinguishment gains/losses

- Certain foreign exchange or hedging results (if non-operating)

Tip: Classification can vary by company or data provider—review footnotes for precise definitions.

“Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 2014 (2014)

Examples

Example 1: Gain on Investment Sale

Company records a pre-tax $120M gain on security sale. Tax rate: 25%. Basic shares: 80M.

After-tax gain: 90M. Basic EPS Other Gains/Losses = 1.125. This increases total basic EPS by $1.125 per share.

Example 2: Restructuring Charge

Company incurs $100M pre-tax restructuring costs. Tax benefit: 25%. Basic shares: 60M.

After-tax loss: 75M loss. Basic EPS Other Gains/Losses = −1.25. This reduces total basic EPS by $1.25 per share.

Significant values here can cause large swings in reported basic EPS, underscoring the need for adjusted or normalized metrics.

Importance in Financial Analysis

This component is key for:

- Identifying volatility from non-core events

- Deriving normalized basic EPS by excluding these items

- Understanding differences between headline and core earnings

Frequent or large amounts may suggest ongoing restructuring, asset turnover, or operational challenges rather than true one-time events.

Warning: Companies sometimes classify recurring costs as ‘other losses’ to boost core EPS—always scrutinize trends and disclosures.

When aggregated with other components (e.g., basic continuing operations), it reconciles to total basic EPS.

Q · 01What does Basic EPS Other Gains/Losses measure?+

Q · 02How is Basic EPS Other Gains/Losses calculated?+

Q · 03Why do analysts adjust for Basic EPS Other Gains/Losses?+

Q · 04Can Basic EPS Other Gains/Losses be positive or negative?+

Q · 05How does Basic EPS Other Gains/Losses relate to total Basic EPS?+