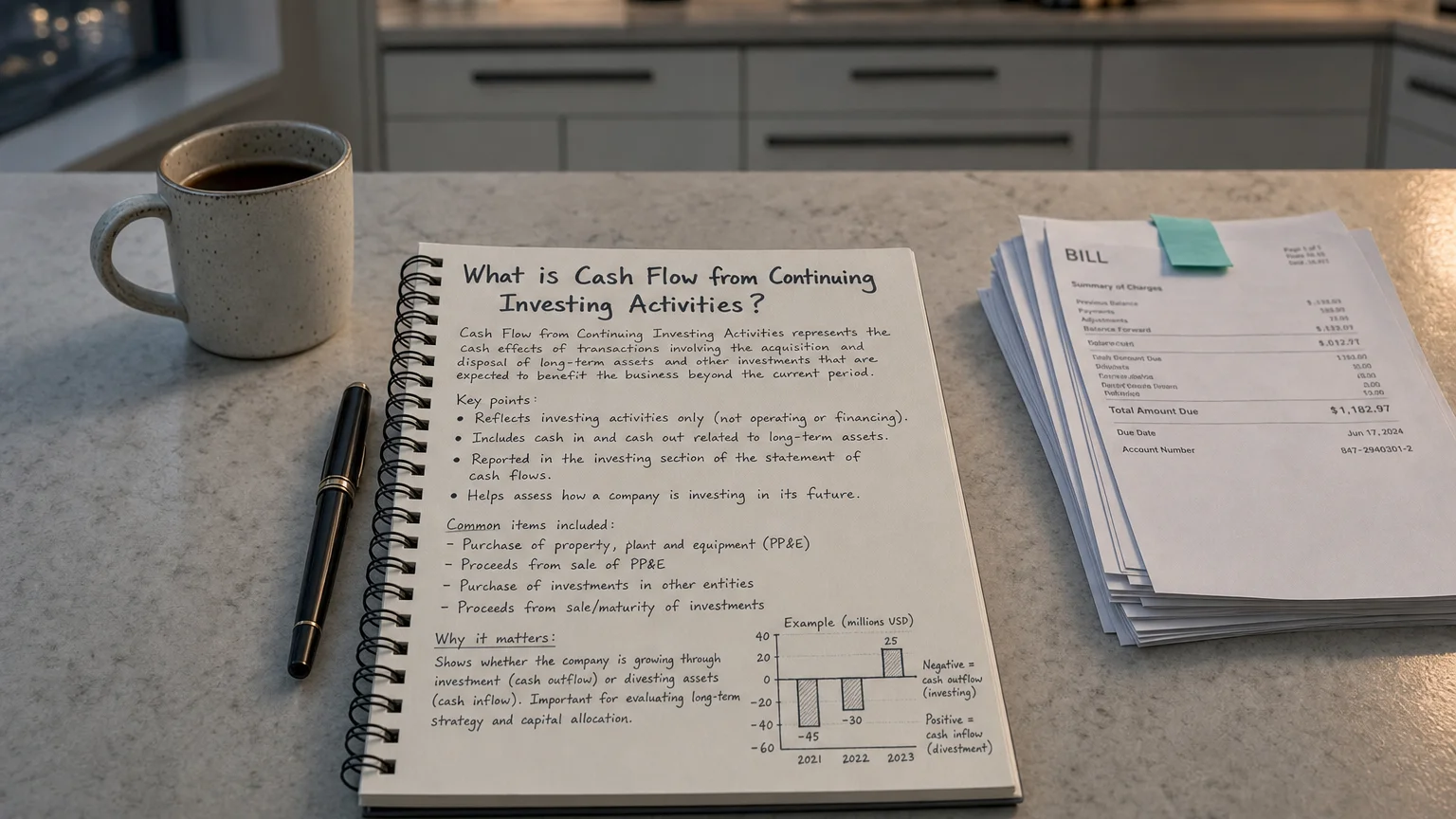

“Cash flow from continuing investing activities is the net cash a company spends or receives on long-term assets, acquisitions, and financial investments for its ongoing operations—stripped of any one-time flows from segments it has sold or closed.”

If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes.

Cash Flow from Continuing Investing Activities refers to the net cash flow generated or used by a company’s investing activities for its continuing operations. On a cash flow statement, “investing activities” include transactions like buying or selling long-term assets and other investments. When a company has discontinued operations (segments that have been sold off or shut down), accounting rules require that its cash flows be split. This line item therefore isolates the investing cash flows of the core business that will remain in operation, providing a clear view of its sustainable investment strategy.

The “Continuing” vs. “Discontinued” Distinction

The term “continuing” is crucial when a company has sold or shut down a business segment. Accounting standards require this separation to provide transparency to investors. It allows an analyst to differentiate cash flows from the core, ongoing business from the one-time cash flows associated with a segment that is no longer part of the company’s future. If a company has no discontinued operations, this line will typically just be labeled ‘Net cash from investing activities.’

Focusing on the Future

By isolating the continuing activities, the cash flow statement helps users focus on the sustainable, recurring investment patterns of the business. Discontinued investing activities, such as the cash proceeds from selling a division, are separated out because they are non-recurring events.

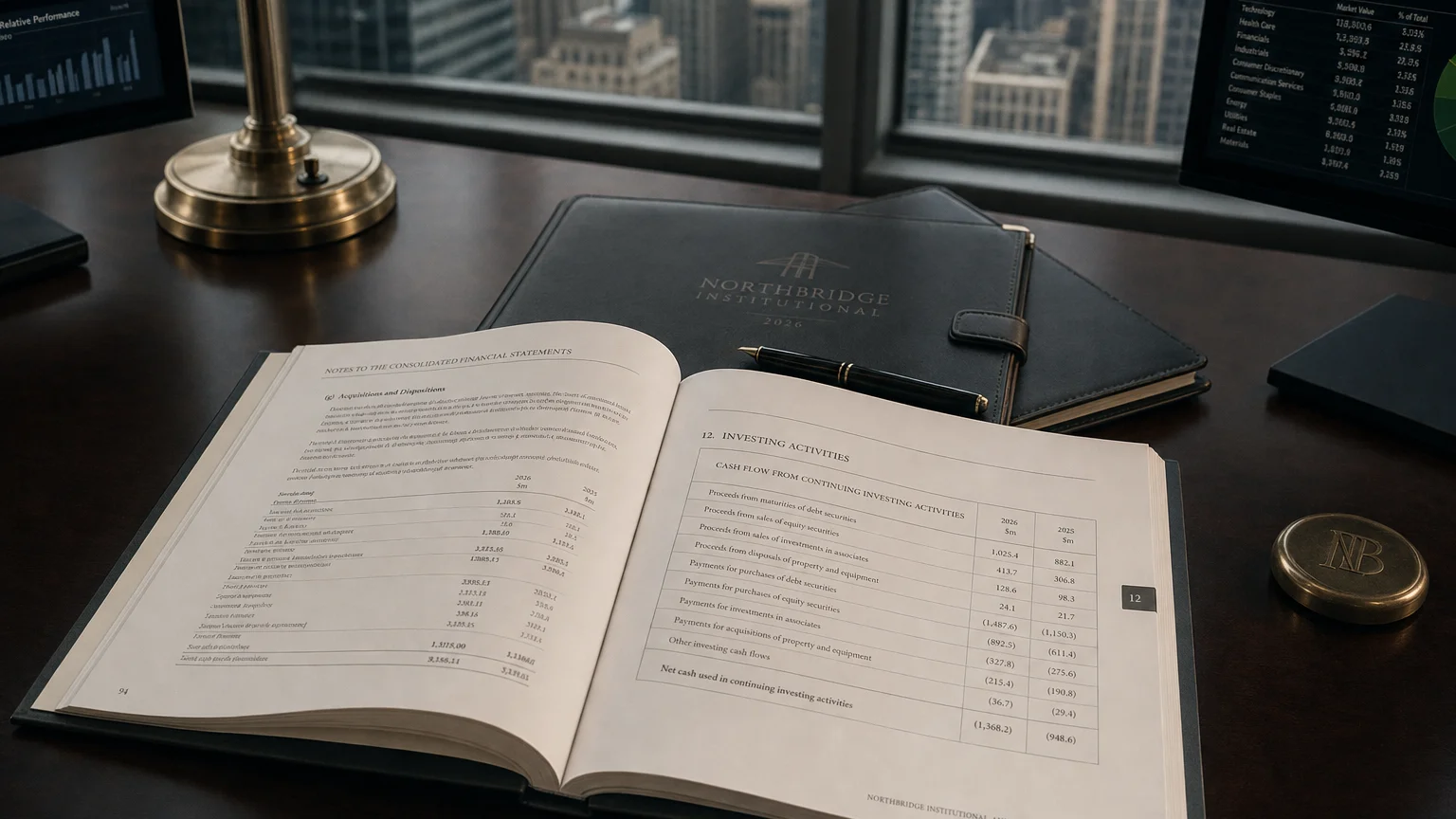

Common Transactions Included

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

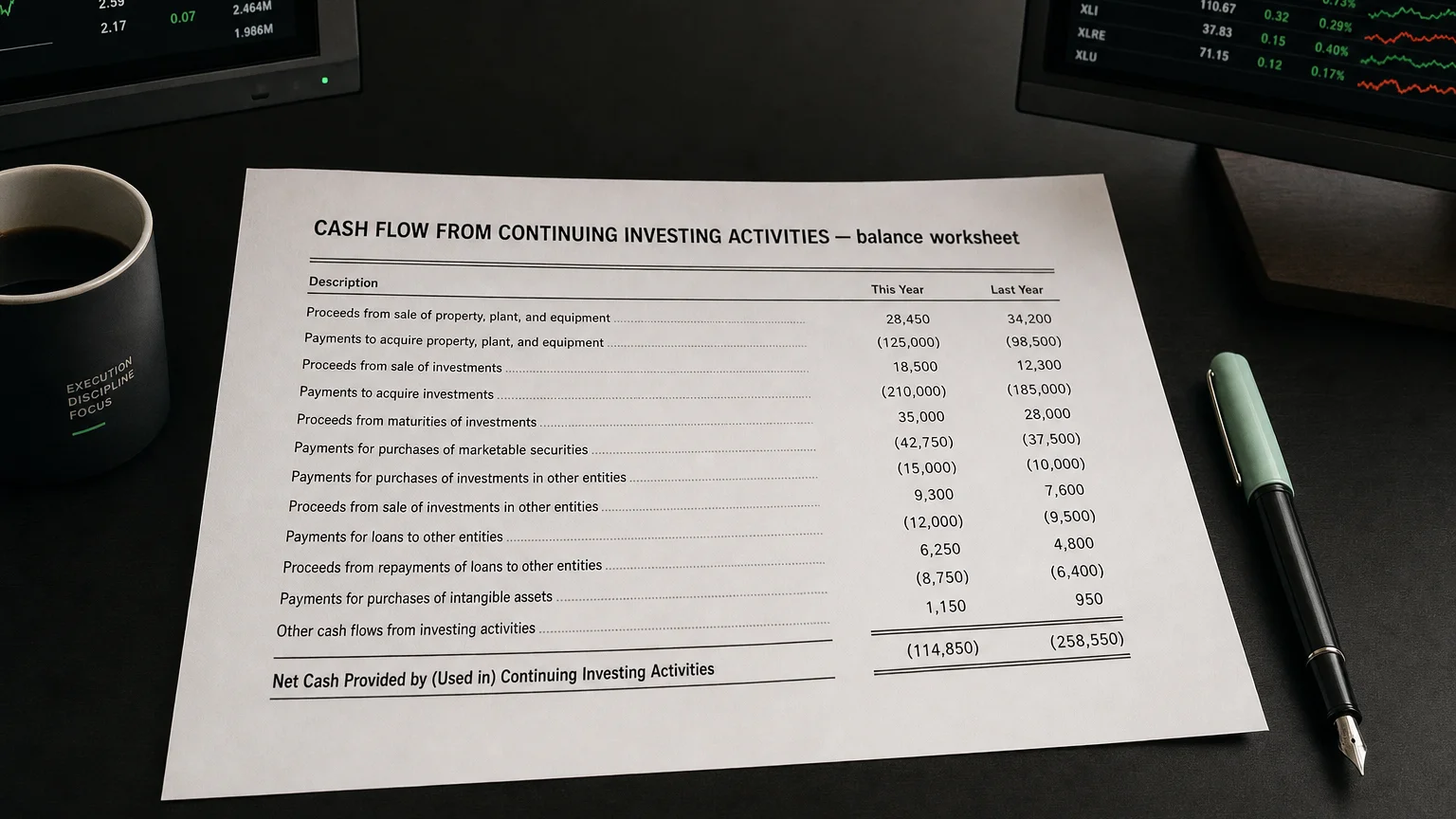

This line item is the net sum of various investing cash inflows and outflows related to continuing operations.

Key Investing Activities

- Capital Expenditures (CapEx): A cash outflow for purchasing property, plant, and equipment (PP&E) or other long-term assets for the ongoing business.

- Proceeds from Asset Sales: A cash inflow from selling long-term assets that the continuing business no longer needs.

- Business Acquisitions: A cash outflow to acquire another company that will become part of the continuing operations.

- Purchases or Sales of Investments: Cash outflows to buy financial securities and cash inflows from selling them or when they mature.

- Loans Made or Collected: Cash outflows when the company lends money and inflows when the principal is collected.

Interpreting Positive vs. Negative Cash Flow

A net cash outflow is very common and often a positive sign for a healthy, growing company. It indicates that the company is investing more in its future—through CapEx, acquisitions, or other investments—than it is generating from asset sales. While this reduces cash in the short term, it is often necessary to support future growth.

A net cash inflow means the company generated more cash from selling assets than it spent on new investments. This could happen if a company is restructuring, downsizing, or simply has a period of lower capital spending. While it boosts cash, a consistently positive figure might raise concerns about under-investment in the business’s long-term health.

Real-World Examples

Centrica plc - Separating the Flows

In 2020, Centrica reported a ‘Net cash outflow from continuing investing activities’ of £263 million, primarily from capital expenditures. Separately, it reported a ‘Net cash flow from discontinued investing activities’ of (£22) million. This breakdown allowed investors to see that the vast majority of its investing cash flow related to its core ongoing business, not the segments it had exited.

Macy’s, Inc. - The Impact of a Sale

In one quarter, Macy’s net cash used in continuing investing activities was only a 66 million cash inflow from selling its After Hours Formalwear discontinued business unit. The separation makes it clear that the low net figure was due to a one-time sale, not a lack of new investment.

Q · 01“Why is a negative investing cash flow often a positive signal?”+

Q · 02“What types of transactions are excluded from this line item?”+

Q · 03“What does a consistently positive investing cash flow indicate?”+