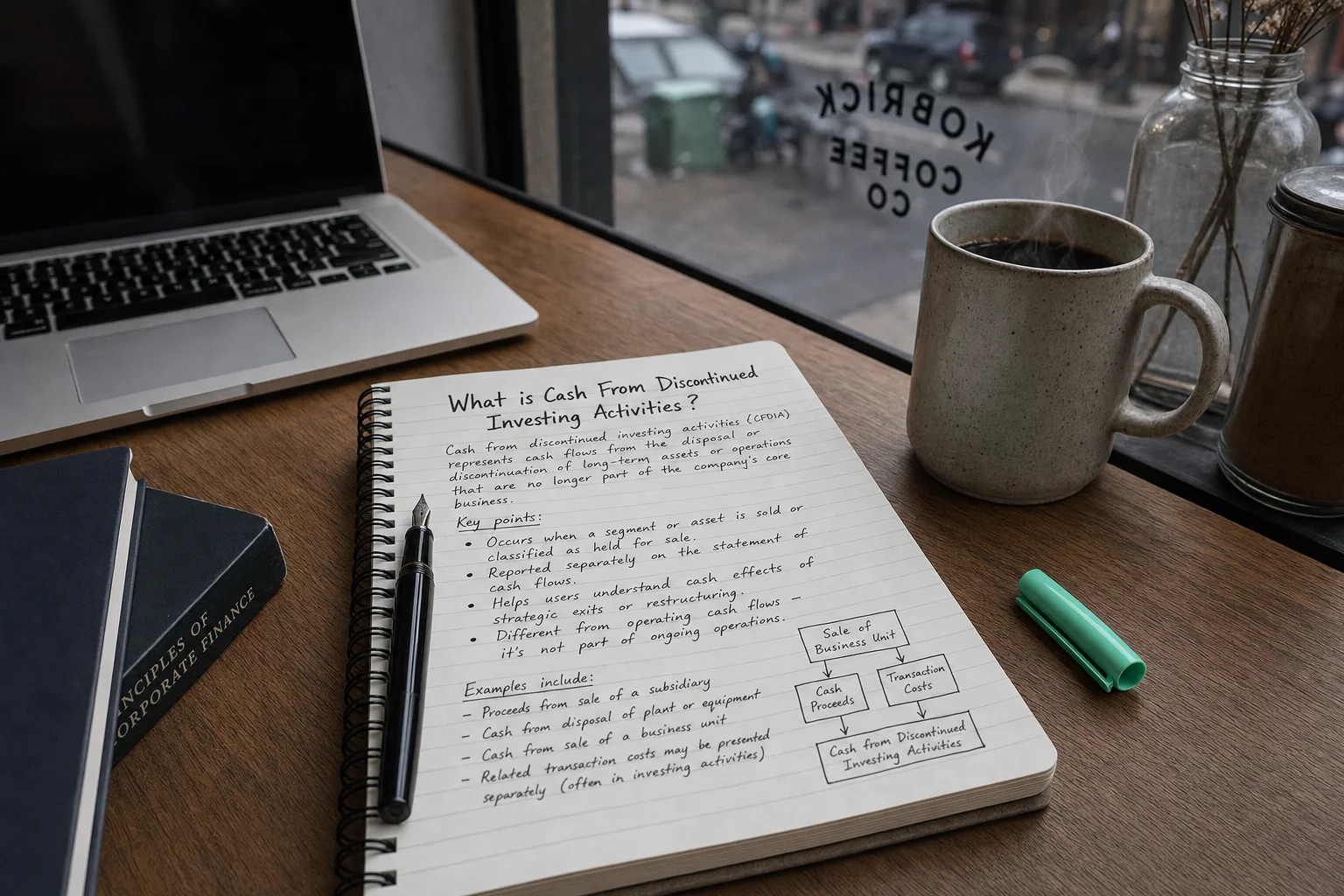

Cash from discontinued investing activities records sale proceeds, asset disposals, and pre-disposal capex tied to divested or held-for-sale units — separated so one-time windfalls don't distort core investing trends.

If we avoid the losers, the winners will take care of themselves.

Cash From Discontinued Investing Activities captures the cash inflows and outflows from investing transactions specifically related to business components that have been sold, shut down, or classified as held for sale. These are separated from continuing operations to give a clear picture of cash flows from the ongoing core business versus one-time or exiting segments.

What It Includes

This line item covers investing cash flows directly linked to the discontinued component:

- Proceeds from selling PP&E, intangibles, or other assets of the discontinued unit

- Cash spent on capital expenditures in the unit before disposal

- Proceeds from selling investments held by the discontinued operation

- Cash used to acquire assets within the discontinued segment (pre-disposal)

The biggest item is usually the cash received from the actual sale of the business or assets.

Only investing flows clearly attributable to the discontinued part are separated.

A Practical Example

“If we avoid the losers, the winners will take care of themselves.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

BigCorp decides to sell its underperforming gadget division.

- Sells the division for $250M cash (after negotiations)

- Before sale, spent $15M on new equipment for the division

- Net Cash From Discontinued Investing Activities: +250M inflow − $15M capex outflow)

Core business investing cash flow stays clean—no $250M sale inflating capex comparisons.

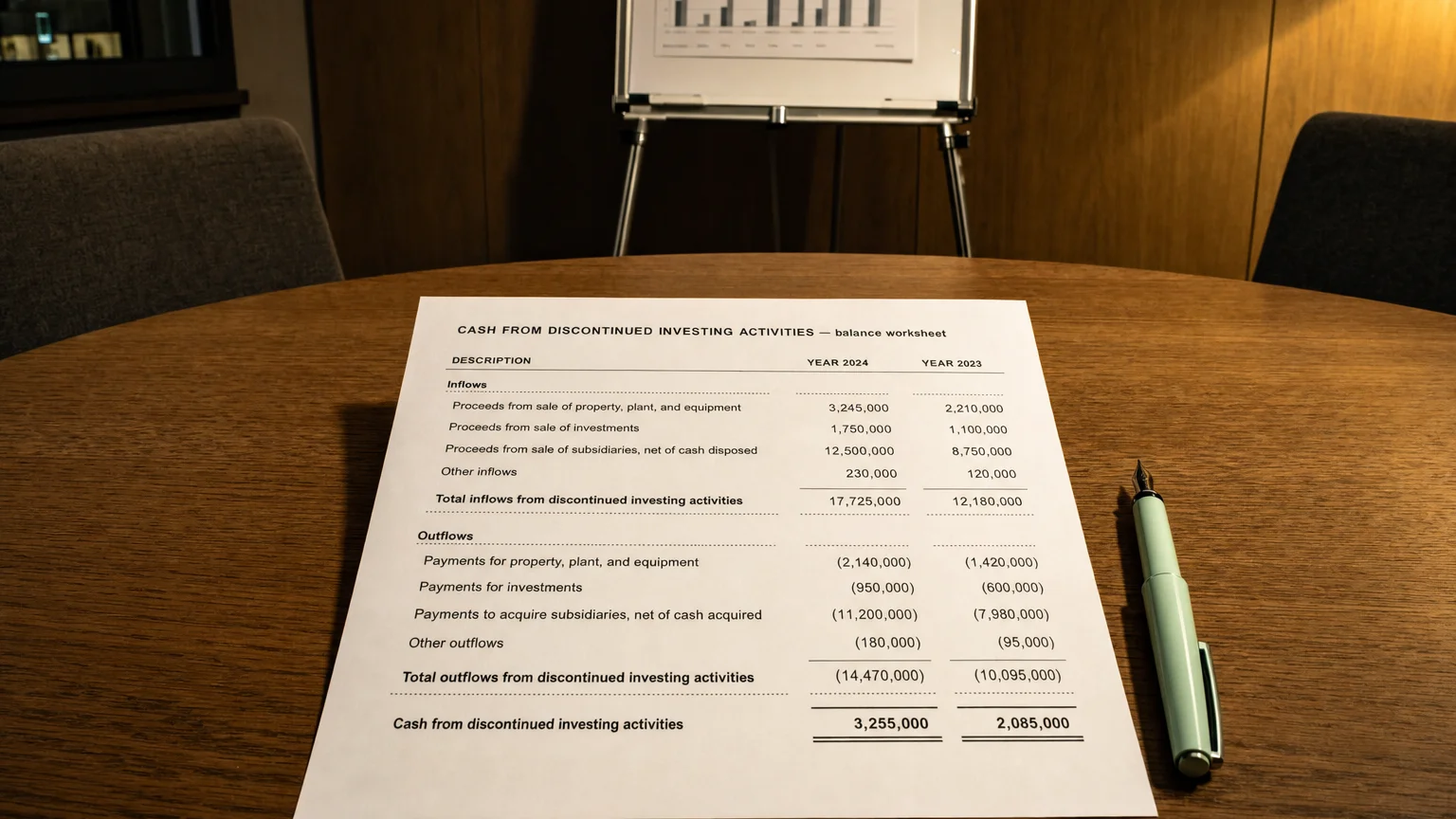

How It’s Presented

In the cash flow statement:

- Separate line or section for discontinued operations

- ‘Cash provided by (used in) discontinued investing activities’

- Or combined net discontinued cash flow with breakdown in notes

- Prior years re-presented for comparability

Total investing cash flow = continuing + discontinued.

Why Separate Reporting Matters

- True picture of ongoing capital expenditure

- Avoid one-time sale proceeds masking core investing needs

- Better comparability year-to-year

- Cleaner free cash flow from continuing operations

- Highlights divestiture impact

Common Scenarios

- Large inflow from selling business unit assets

- Pre-sale capex in unit being divested

- Proceeds from disposing subsidiary investments

- Cash spent on final improvements before sale

- Recovery of prior investments in discontinued segment

What to Look For

- Major inflows = sale proceeds (one-time boost)

- Outflows = last-minute capex (why spend on exiting unit?)

- Net impact on total cash

- Comparison to continuing investing (core capex trend)

- Recurring discontinued items (chronic portfolio trimming?)

Don’t mistake large discontinued investing inflow for sustainable investing cash generation.

Q · 01What is the largest item in discontinued investing activities?+

Q · 02How does discontinued investing affect free cash flow?+

Q · 03Are prior periods restated for discontinued investing?+