Cash from discontinued operating activities is the net cash from revenue, expenses, and working capital changes in units classified as discontinued or held for sale — isolated so core OCF reflects only sustainable, ongoing operations.

The intelligent investor is a realist who sells to optimists and buys from pessimists.

Cash From Discontinued Operating Activities is the net cash provided by (or used in) the day-to-day operations of business components that have been sold, shut down, or classified as held for sale. This line isolates the ongoing cash generation or drain from these exiting segments, allowing a clean view of cash flow from the company’s continuing core operations.

What It Captures

This line shows the cash impact from running the discontinued business until disposal—basically its operating cash flow while still owned.

- Cash from sales/revenue of the discontinued unit

- Cash paid for expenses (suppliers, salaries, etc.)

- Working capital changes (receivables, inventory, payables)

- Taxes and interest specifically attributable

Sale proceeds themselves go to investing; shutdown costs may split.

Prior periods re-presented as discontinued for comparability.

A Practical Example

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

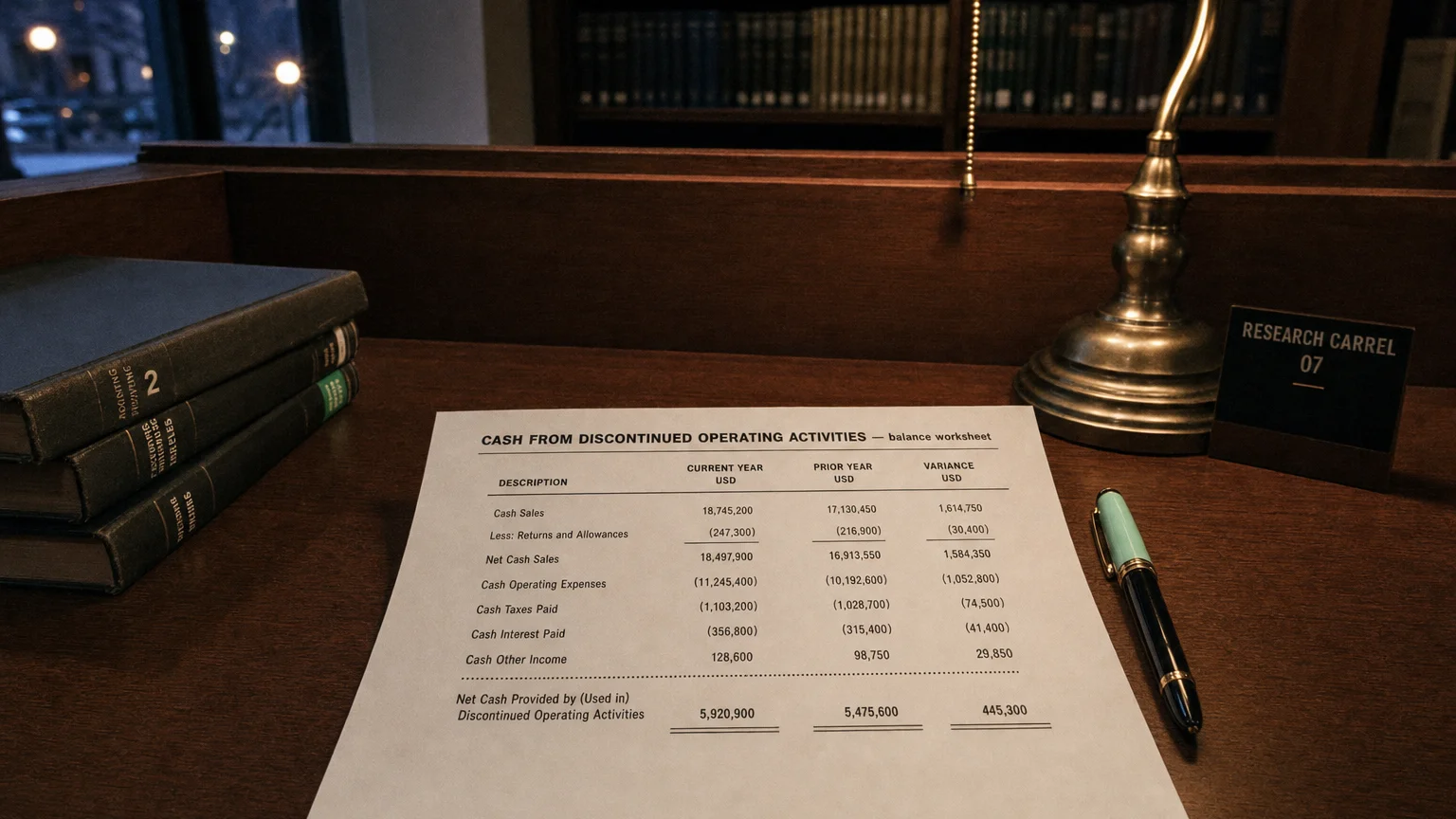

Conglomerate sells its consumer gadgets division mid-year.

- First half: Gadgets generated 40M expenses → +$20M operating cash

- Working capital release (sold inventory): +$10M

- Cash From Discontinued Operating Activities: +$30M

This $30M is separated—core business OCF isn’t inflated by a unit being exited.

How It’s Presented

In the cash flow statement:

- Separate line or section for discontinued operations

- ‘Cash provided by (used in) discontinued operating activities’

- Or single net discontinued cash flow with breakdown in notes

- Subtotal for continuing operations above

Total operating cash flow = continuing + discontinued.

Why Separate Reporting Matters

- True picture of sustainable operating cash generation

- Avoid ongoing losses from discontinued unit dragging core OCF

- Better valuation (multiples on continuing operations)

- Comparability across periods

- Focus management attention on core performance

Common Scenarios

- Profitable unit sold → positive discontinued OCF

- Loss-making division divested → negative drag removed from core

- Working capital release on shutdown (inventory liquidation)

- Ongoing operations until closing date

What to Look For

- Positive = cash cow being sold (future loss?)

- Negative = cash drain finally stopped

- Working capital effects (release or build?)

- Contribution to total OCF

- Trend in continuing OCF post-disposal

Exclude discontinued OCF for assessing core cash generation quality.

Q · 01Does discontinued operating cash include sale proceeds?+

Q · 02Why strip discontinued operating cash from valuation?+

Q · 03Can discontinued operating cash be positive or negative?+