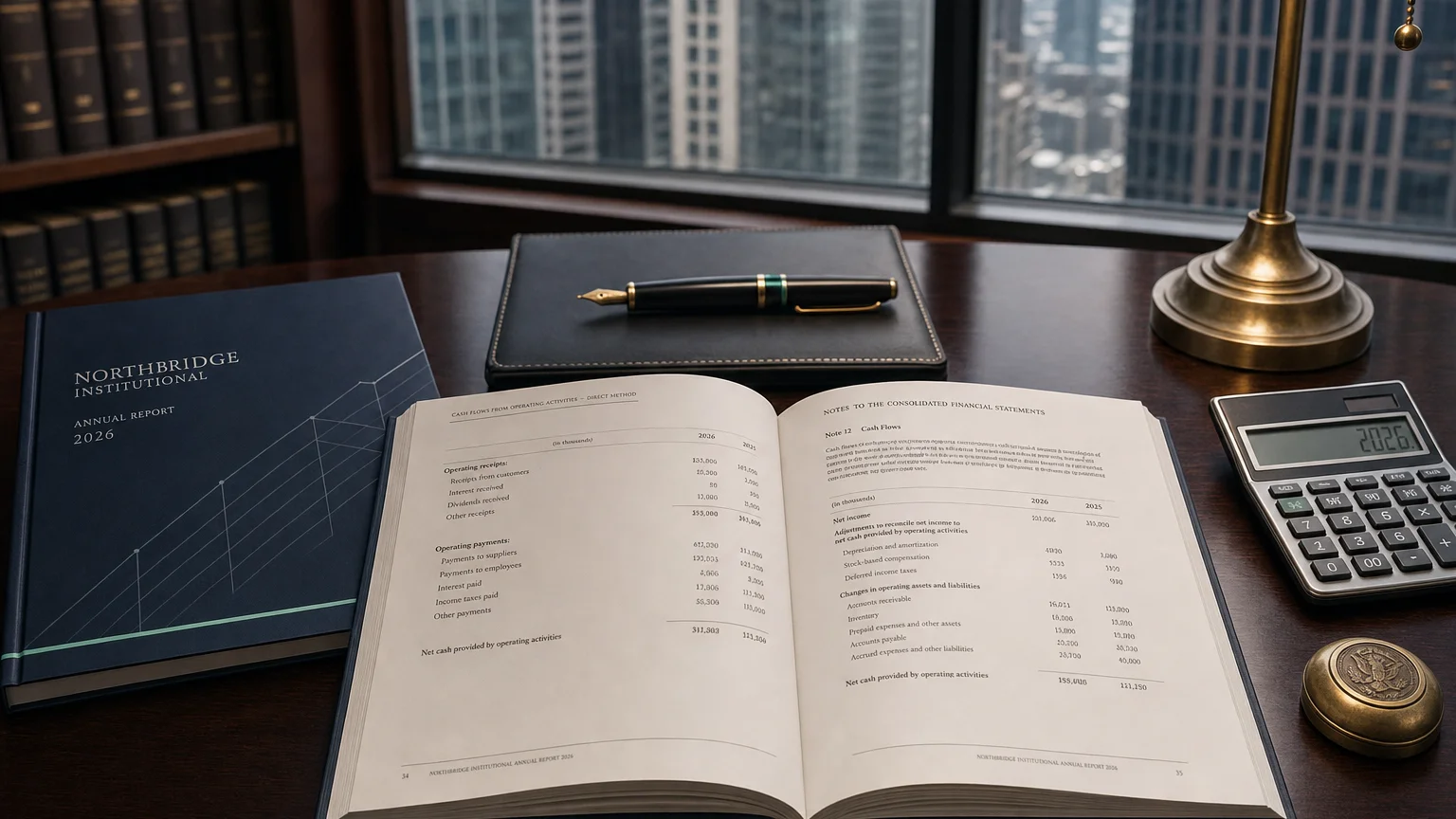

The direct method presents operating cash flow by listing gross cash inflows—primarily receipts from customers—and gross cash outflows to suppliers, employees, and tax authorities. It reaches the same net figure as the indirect method but without starting from net income.

The stock market is filled with individuals who know the price of everything but the value of nothing.

Cash Flows from (used in) Operating Activities – Direct Method presents the actual cash inflows and outflows from a company’s day-to-day business operations. Instead of starting with net income and adjusting for non-cash items (indirect method), the direct method lists major classes of gross cash receipts (e.g., from customers) and gross cash payments (e.g., to suppliers, employees) to arrive at net operating cash flow.

What the Direct Method Shows

The direct method gives a straightforward look at where operating cash actually comes from and goes to—no adjustments or add-backs needed.

It’s like reading a cash register tape for the whole business: money in from customers, money out to suppliers, employees, taxes, etc.

Net result = Cash generated (or burned) by core operations.

Typical Line Items You’ll See

“The stock market is filled with individuals who know the price of everything but the value of nothing.”

— Philip Fisher, Author, Common Stocks and Uncommon Profits Common Stocks and Uncommon Profits (1958)

Cash Receipts (Inflows)

- Receipts from customers

- Interest and dividends received

- Other operating cash receipts (refunds, settlements)

Cash Payments (Outflows)

- Payments to suppliers for goods/services

- Payments to/on behalf of employees (salaries, benefits)

- Interest paid

- Income taxes paid

- Other operating cash payments

Net = Receipts − Payments = Operating Cash Flow.

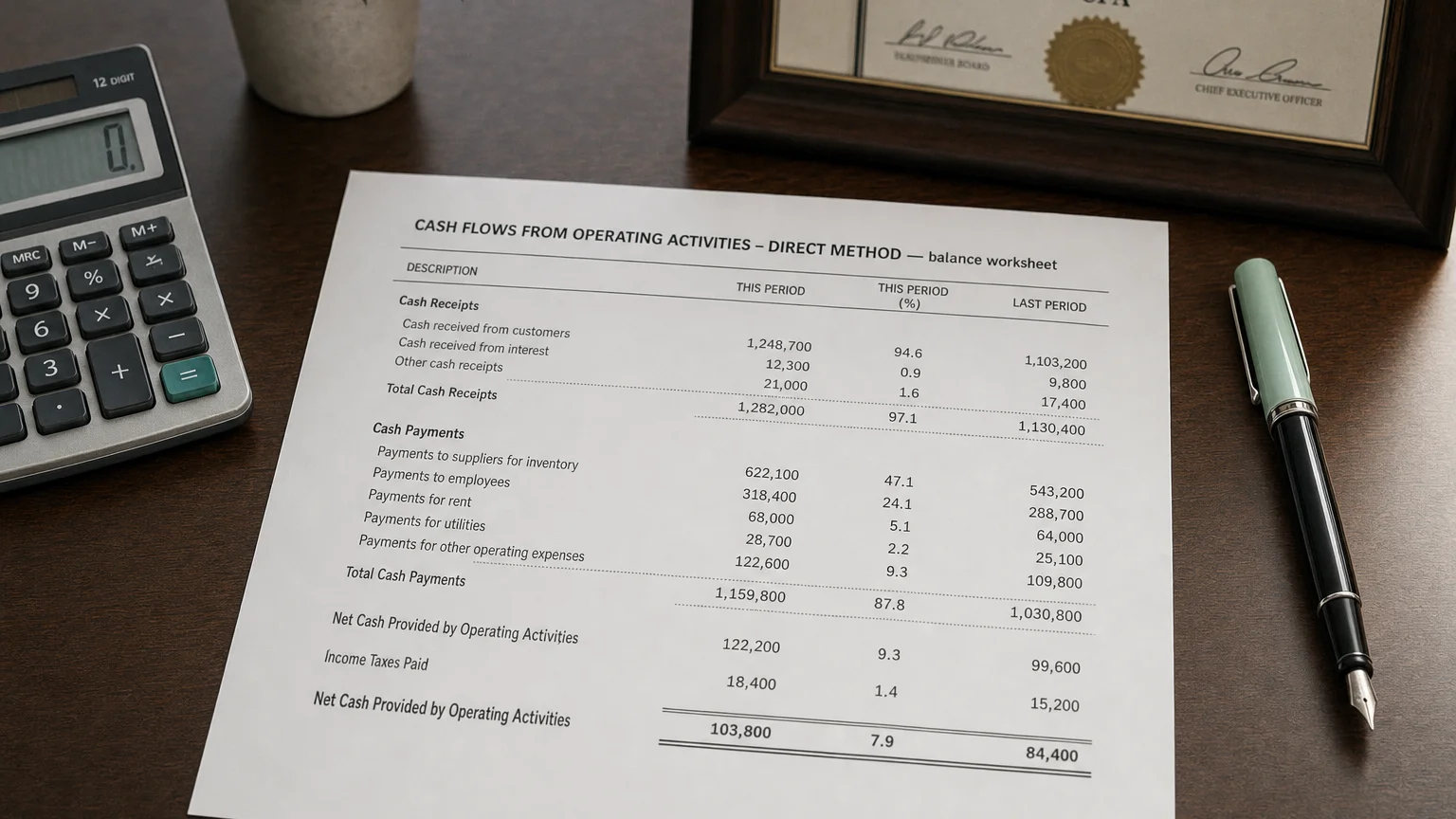

A Simple Example

Small retailer reports direct method:

- Cash received from customers: $1,200,000

- Cash paid to suppliers: -$700,000

- Cash paid to employees: -$300,000

- Income taxes paid: -$80,000

- Interest received: +$10,000

- Net Cash from Operating Activities: +$130,000

You see exactly where cash came from and went—no mystery adjustments.

Direct vs. Indirect – Why It Matters

Direct Method

- Shows actual cash movements

- Easier for non-accountants to understand

- Better insight into cash conversion cycle

Indirect Method

- Starts with net income

- Adjusts for non-cash and working capital

- More common (easier to prepare)

Both give same net operating cash flow—direct is just more transparent.

Where It Appears

Top section of cash flow statement:

- ‘Cash Flows from Operating Activities’

- Major classes of receipts and payments listed

- Net subtotal

US GAAP encourages direct but allows indirect; IFRS prefers direct but accepts indirect with reconciliation.

What It Tells You

- True cash generation from customers

- Major cash drains (suppliers, payroll)

- Collection and payment efficiency

- Operational cash cycle health

- Comparison to accrual revenue/expenses

Low receipts despite high sales = collection problems.

Q · 01How does the direct method differ from the indirect method?+

Q · 02Which accounting standards require or prefer the direct method?+

Q · 03What does low cash receipts despite high reported sales indicate?+