Cash Flow From Continuing Operating Activities

Cash flow from continuing operating activities measures cash generated by a company's core business, isolated from discontinued or divested segments.

Overview

Cash flow from continuing operating activities measures cash generated by a company's core business, isolated from discontinued or divested segments.

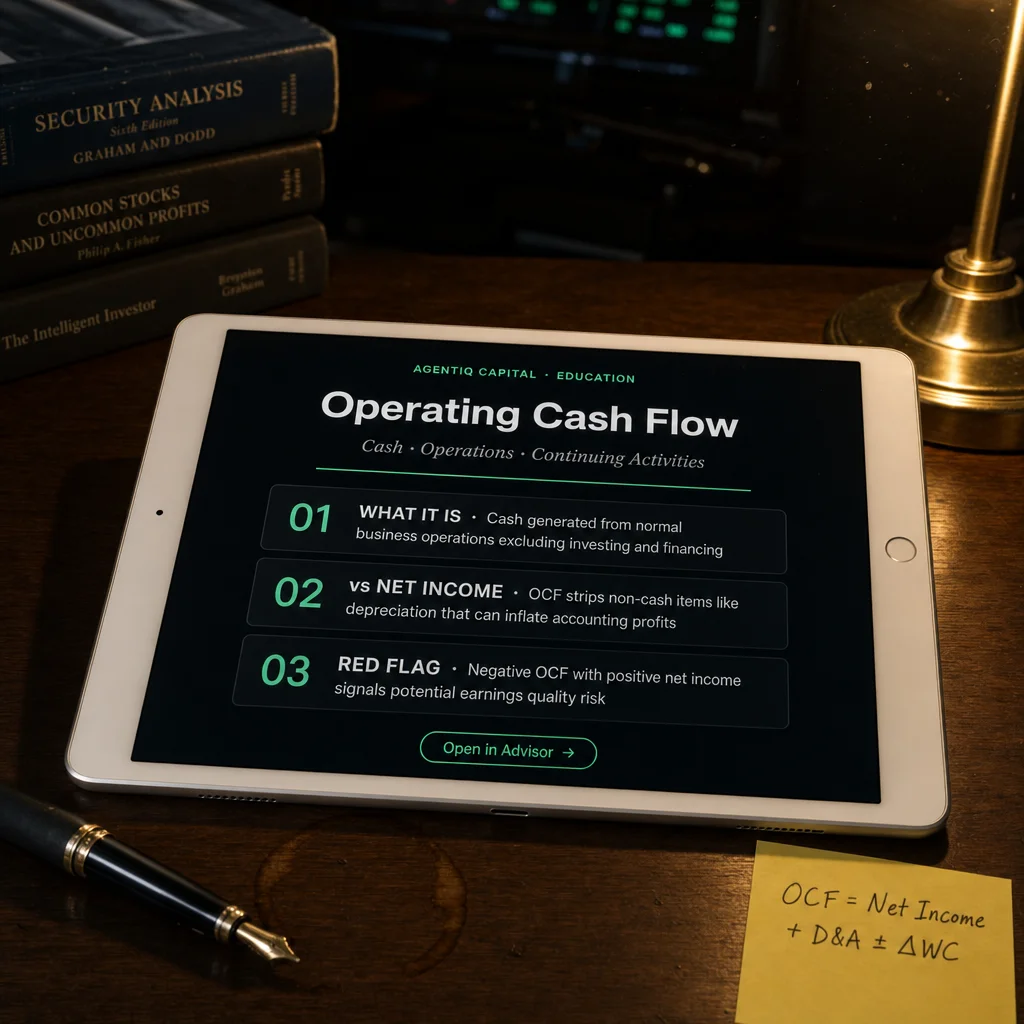

Cash flow from continuing operating activities refers to the net cash generated or consumed by a company’s operating activities that come from its continuing operations. In other words, it is the cash flow produced by the company’s core, day-to-day business functions that are expected to continue in the future, as opposed to any businesses or segments that have been sold off or shut down (discontinued operations). This figure essentially represents the portion of operating cash flow attributable to the ongoing parts of the business. By focusing on continuing operations, this measure provides a clear view of the sustainable cash-generating power of a company.

Cash Inflow or Outflow?

“Cash flow from continuing operating activities” can represent either a net cash inflow or a net cash outflow, depending on whether the continuing operations generated more cash than they used during the period. A positive number (often labeled as “net cash provided by operating activities”) indicates a net cash inflow - the ongoing operations brought in more cash than they spent. A negative number (labeled as “net cash used in operating activities”) indicates a net cash outflow, meaning the continuing operations required more cash than they generated.

Healthy, mature companies typically report a net inflow (positive operating cash flow), which signifies that the core business is generating cash. However, it’s not unusual for startups or expanding companies to have net operating cash outflows in the short term if they are investing in growth (spending more on inventory, marketing, etc. than the cash coming in). The key is that this figure shows the net result of all cash receipts and payments from continuing business operations.

Where It Appears on the Cash Flow Statement

"In the short run, the market is a voting machine. In the long run, it is a weighing machine."

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

On the cash flow statement, cash flow from operating activities is presented in the first section (before investing and financing activities). When a company has no discontinued operations, this section is typically titled “Cash flows from operating activities” and by default represents the continuing operations. If the company does have discontinued operations to report, the statement will often split the operating cash flows into continuing and discontinued components for clarity.

In such cases, you might see a subsection or line items for “Net cash provided by operating activities - continuing operations” and a separate line for “Net cash provided by (or used in) operating activities - discontinued operations.” The continuing operations portion appears under the Operating Activities section, usually at the top of the cash flow statement, and the discontinued operations’ cash flow may be shown below or separately. This presentation helps readers see the cash flow from the core ongoing business distinctly.

Relationship to Operating Cash Flow (OCF)

“Cash flow from continuing operating activities” is essentially the same concept as Operating Cash Flow (OCF) or “Net cash from operating activities,” but narrowed to only continuing parts of the business. Thus, if a company has no discontinued segments, its “cash flow from operating activities” equals the cash flow from continuing operations. The term “continuing” is explicitly added only when needed to distinguish from discontinued operations.

In cases where discontinued operations exist, total OCF would include both continuing and discontinued operations. The cash flow statement may then segregate the two: the continuing OCF shows the cash from the ongoing business, and the discontinued OCF shows cash from the portion of the business that is being phased out. Together, they sum up to the company’s total net cash from operating activities. In summary, cash flow from continuing operating activities is the sustainable, recurring operating cash flow that investors and analysts focus on when evaluating the company’s core performance.

Calculated Under the Indirect Method

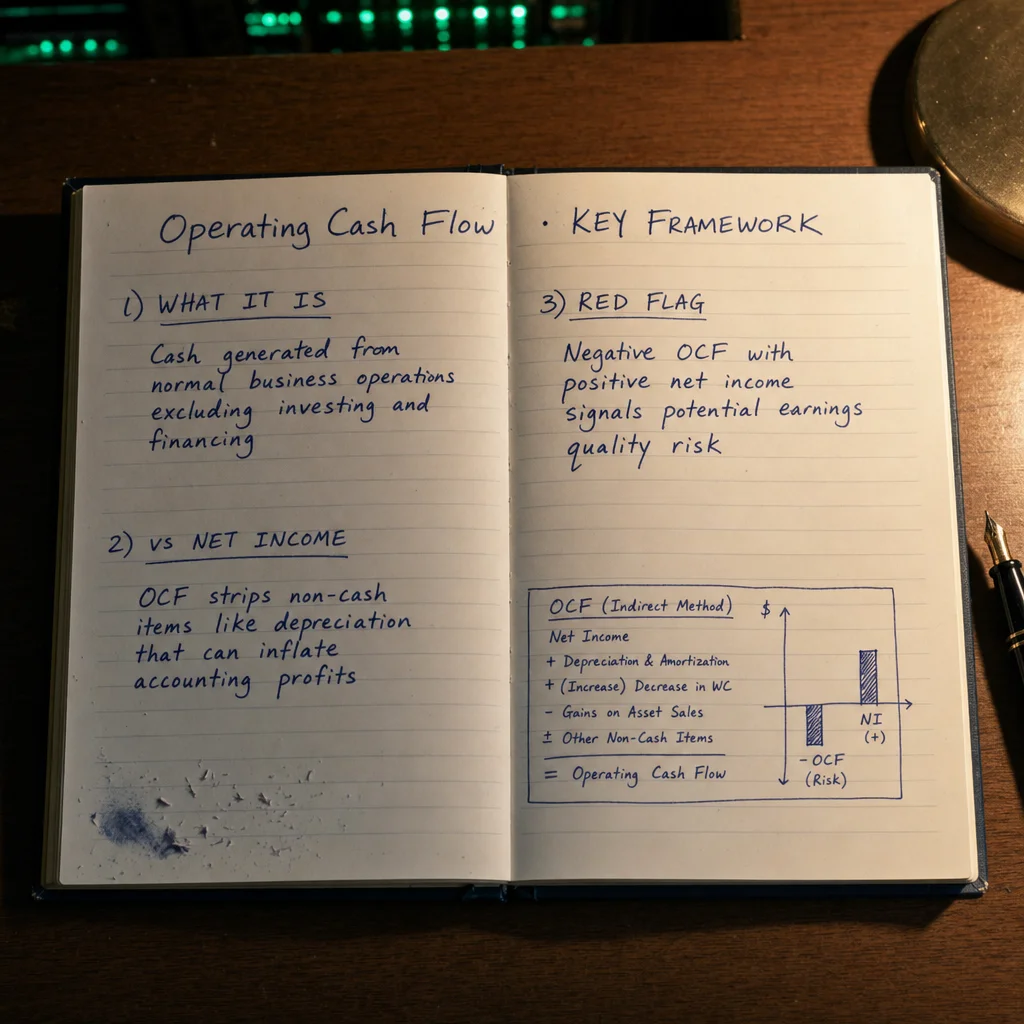

Most companies use the indirect method to calculate cash flow from operating activities. When focusing on continuing operations, the calculation starts with net income from continuing operations and makes several adjustments to reconcile it to a cash basis.

- Start with Net Income from Continuing Operations: This is the profit from the company’s ongoing activities, excluding any income or loss from discontinued segments. This step ensures that only the ongoing business’s profit is considered.

- Add Back Non-Cash Expenses: Expenses that reduced net income but didn’t involve a cash outflow are added back. The most common are depreciation and amortization, but also include impairments or stock-based compensation.

- Adjust for Non-Operating Gains/Losses: Gains or losses from investing or financing activities (like a gain on the sale of equipment) that were included in net income are removed to avoid double-counting, as their cash effects belong in other sections.

- Adjust for Changes in Working Capital: This step reflects the actual cash receipts and payments by accounting for changes in current assets and liabilities like accounts receivable, inventories, and accounts payable.

Direct vs. Indirect Method

Companies that use the direct method (less common) would calculate this figure by directly summing all cash inflows from customers and subtracting all cash outflows for operating expenses related to continuing operations. Regardless of the method used, the final number for cash flow from continuing operating activities should be the same.

Continuing vs. Discontinued Operations Cash Flows

It’s crucial to distinguish cash flows from continuing operations versus discontinued operations. Discontinued operations refer to parts of the business that have been sold, shut down, or are held for sale. Accounting rules require that their income and cash flows be shown separately so investors can see what cash is coming from the ongoing business versus a part that will not contribute in the future.

The key difference is that continuing operations’ cash flow reflects the ongoing business’s cash-generating ability, whereas discontinued operations’ cash flow is temporary and will vanish once the disposal is complete. By separating the two, analysts can evaluate the performance of the core business on its own. If a firm’s total OCF was boosted by a large positive cash influx from a discontinued unit, separating them makes this clear and prevents one-time events from masking the true trends in the ongoing operations.

Why It’s Important for Analyzing Ongoing Business Health

Cash flow from continuing operating activities is a critical indicator of a company’s financial health and the quality of its earnings. It shows how much actual cash the company’s core business is generating. Investors and analysts pay close attention to this metric for several key reasons:

- Sustainability of Cash Generation: It tells you how well the ongoing segments are producing cash. A consistently positive and growing figure is a strong sign that the company’s core business model is sound and can fund itself.

- Quality of Earnings: It helps assess if reported profits are translating into real cash. If net income from continuing operations is high but its cash flow is low or negative, it could be a red flag for accounting issues.

- Financial Flexibility and Ongoing Funding: This cash is the primary source for investments, debt repayment, and dividends. Strong internal cash generation reduces reliance on external financing.

- Focus on Future Performance: By isolating continuing operations, analysts can make better forward-looking assessments. Discontinued operations are not part of the future, so including them would distort projections. This metric is vital for valuation models.

Real-World Example Presentation

Example - Novartis AG (Q3 2024)

In its interim financial report, Novartis highlighted that net cash flows from operating activities from continuing operations amounted to approximately $6.3 billion for the quarter, whereas the net cash flows from operating activities from discontinued operations were about $0.07 billion ($74 million). This presentation makes it clear that almost all of Novartis’s operating cash that quarter came from its ongoing businesses.

Example - Ryder System, Inc. (Q1 2010)

Ryder’s consolidated cash flow statement started with net earnings, subtracted the loss from discontinued operations, and then made adjustments. It reported “Net cash provided by operating activities from continuing operations” of $271.5 million. By showing this figure distinctly, Ryder enabled investors to see that its core truck leasing and logistics operations generated a positive cash flow independent of segments it was exiting.

Example - Federated Department Stores (Macy’s Inc.)

In an earlier financial statement, Federated (now Macy’s) showed “Net cash provided by continuing operating activities” of $630 million, contrasted with a net cash inflow of $731 million from discontinued operations. In that case, the discontinued unit provided a significant one-time cash boost. The statement’s layout allowed investors to deduce that the larger total operating cash flow was bolstered by a non-recurring source, and the business would primarily rely on the $630 million going forward.