Change in dividend payable is the net increase or decrease in dividends declared by the board but not yet paid. An increase adds to operating cash flow; a decrease subtracts as prior declarations are settled.

The stock market is a device for transferring money from the impatient to the patient.

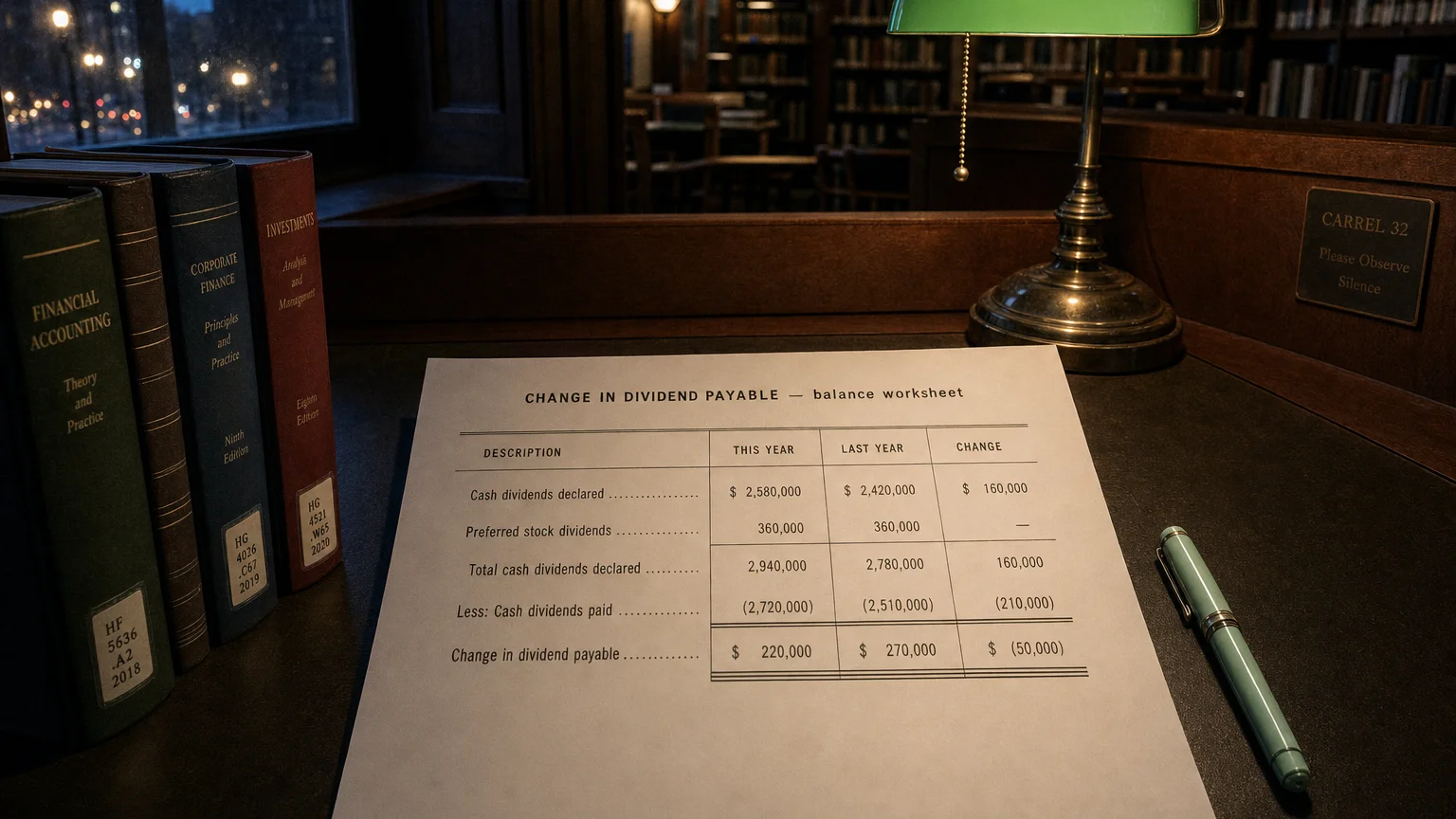

Change in Dividend Payable is the net increase or decrease in the liability for dividends that have been declared by the board but not yet paid to shareholders. This line appears in the operating activities section of the indirect-method cash flow statement. An increase adds to operating cash flow (dividends declared but cash not yet paid), while a decrease subtracts (paying out previously declared dividends).

What It Really Means

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Annual Report (1999)

Dividends become a liability the moment the board declares them—creating Dividends Payable. Cash only leaves on the payment date.

When the liability grows (more declared than paid), you’re keeping cash longer—positive for operating cash flow. When it shrinks (more paid than declared), cash goes out to settle past declarations—negative for OCF.

A Clear Example

Company pays quarterly dividends.

- Q4 declaration (December): $10M dividend for Q4, payable in January

- Year-end: Dividends Payable rises $10M

- Cash flow this year: +$10M Change in Dividend Payable (add-back)

- January next year: Pay $10M cash

- Next year cash flow: -$10M Change in Dividend Payable

This year OCF gets a timing boost; next year takes the cash hit.

Common Drivers

- Declaration vs. payment date timing (especially year-end)

- Dividend increase (higher declarations)

- Special or one-time dividends

- Preferred vs. common dividend schedules

- Arrears on cumulative preferred

Quarterly payers often show swings around fiscal year-end.

How It Fits in Cash Flow

Indirect method operating section:

- Net Income

-

- Non-cash items

-

- Increase in Dividend Payable (or − Decrease)

- = Cash from Operations

It’s a working capital adjustment for dividend timing.

What a Change Tells You

- Rising → conserving cash on dividends (OCF boost)

- Falling → paying out past declarations (cash drain)

- Year-end spike common (declaration before payment)

- Link to dividend policy changes

- Preferred arrears buildup (if cumulative)

Compare to actual cash dividends paid (financing) for full picture.

Q · 01When does a dividend declaration create a cash flow adjustment?+

Q · 02How does a year-end dividend declaration distort OCF?+