Change in accrued expense is the net increase or decrease in expenses incurred but not yet paid. A rise adds to operating cash flow by delaying cash outflows; a fall subtracts as prior obligations are settled.

In investing, you get what you don't pay for. Costs matter enormously.

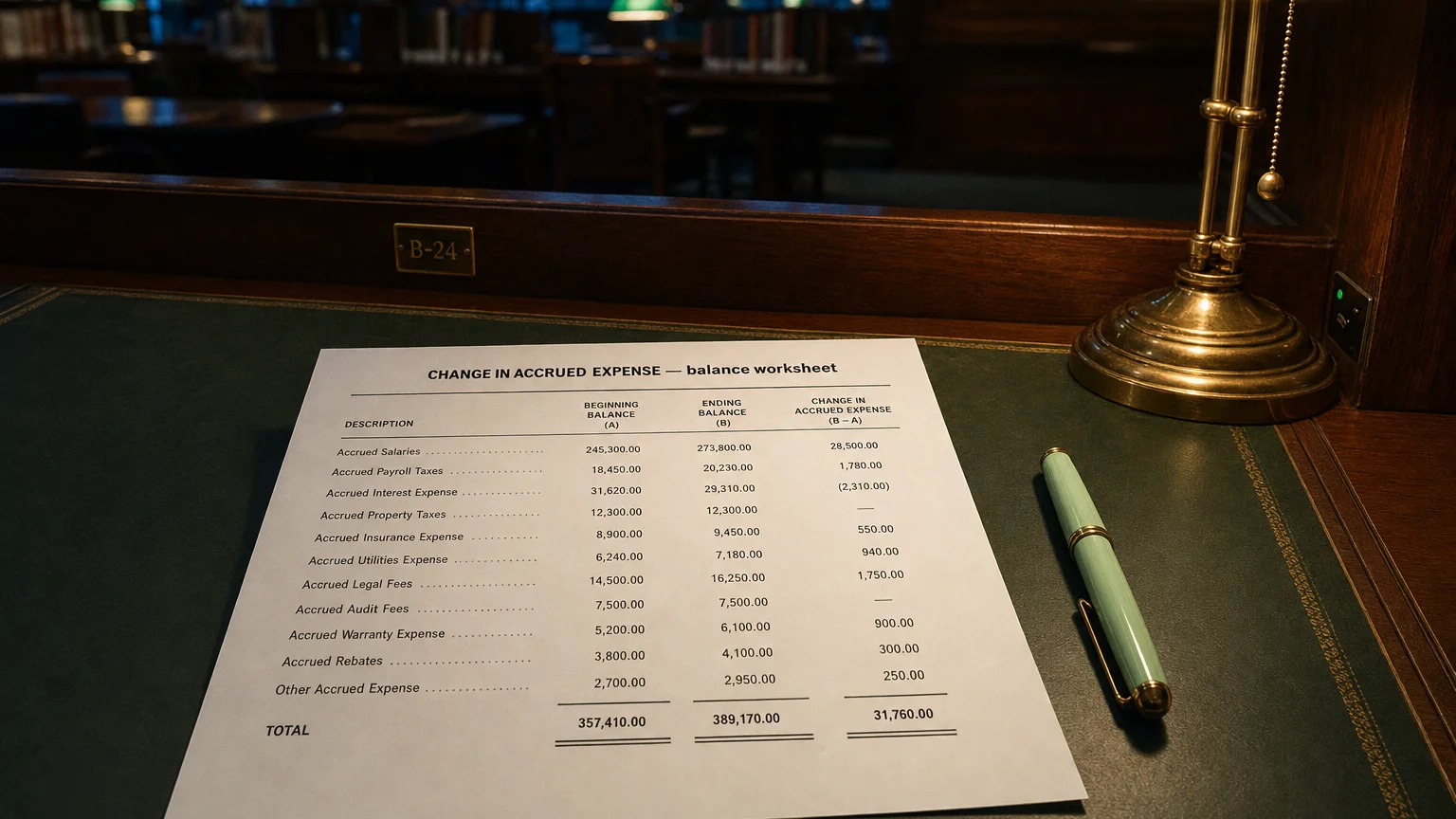

Change in Accrued Expense is the net increase or decrease in accrued liabilities (expenses incurred but not yet paid) during the reporting period. This line appears in the operating activities section of the indirect-method cash flow statement. A rise in accrued expenses adds to operating cash flow (you’ve delayed cash payment), while a fall subtracts (you’re catching up on prior accruals).

What It Really Means

Accrued expenses are bills you’ve run up but haven’t paid yet—like salaries earned this month but paid next, or interest accumulating on debt.

When these obligations grow, you’re effectively getting an interest-free loan from employees, lenders, or suppliers—cash stays in your pocket longer, boosting operating cash flow.

When they shrink, you’re paying off past accruals—cash goes out the door.

A Straightforward Example

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

Your company pays bonuses in January for the prior year’s performance.

- End of Year 1: Accrue 5M

- Cash flow Year 1: +$5M Change in Accrued Expense (add-back)

- January Year 2: Pay 5M

- Cash flow Year 2: -$5M Change in Accrued Expense

Year 1 OCF gets a boost; Year 2 takes the hit when cash actually leaves.

Common Drivers

- Year-end bonus or incentive accruals

- Interest accruing on debt

- Unpaid utilities, rent, or services

- Warranty or legal provisions

- Timing of payroll cycles

Seasonal businesses often see big swings around year-end.

How It Fits in Cash Flow

Indirect method operating section:

- Net Income

-

- Non-cash expenses (depreciation, etc.)

-

- Increase in Accrued Expenses (or − Decrease)

- = Cash from Operations

It’s a working capital adjustment—bridging accrual profit to cash reality.

What a Change Tells You

- Rising accruals → conserving cash, possibly growing obligations

- Falling accruals → paying down past bills, cash outflow

- Year-end spikes → bonus timing or earnings management?

- Consistent increases → aggressive accrual policy

- Link to revenue growth (normal) or mismatch (concern)

Sharp drop after big buildup can signal cash crunch or reversal of aggressive accruals.

Q · 01What types of expenses most commonly drive accrued expense changes?+

Q · 02Can rising accrued expenses signal financial trouble?+