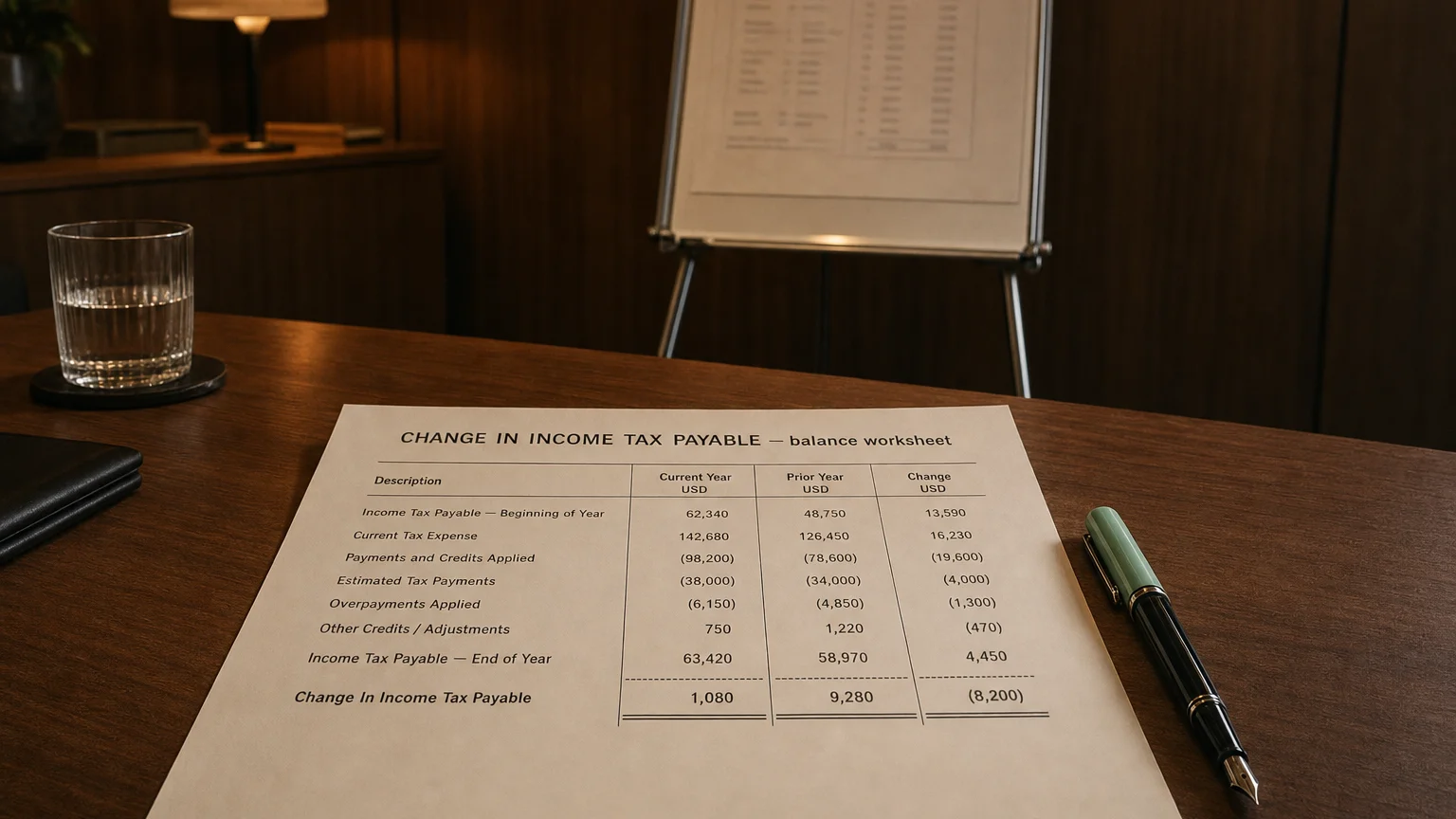

Change in income tax payable is the net increase or decrease in current tax obligations during the period. An increase adds to operating cash flow because more tax was accrued than paid; a decrease subtracts as prior liabilities are settled.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

Change in Income Tax Payable is the net increase or decrease in the company’s current income tax liability during the reporting period. This line appears in the operating activities section of the indirect-method cash flow statement. An increase adds to operating cash flow (tax expense recognized but cash payment delayed), while a decrease subtracts (settling prior tax liabilities with cash).

What It Really Means

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (1934)

Income tax payable is the current tax the company owes based on taxable profit for the year. Companies often make estimated payments throughout the year, but the final amount is settled later.

When the liability grows, you’ve recorded more tax expense than you’ve paid in cash—keeping money longer and boosting operating cash flow. When it falls, you’re paying more cash than the current expense—reducing OCF.

A Clear Example

Company estimates quarterly taxes and pays 25M total owed.

- Income Tax Payable rises by $5M

- Cash flow this year: +$5M Change in Income Tax Payable (add-back)

- Next year: Pay the $5M balance

- Next year cash flow: -$5M Change in Income Tax Payable

This year gets a cash timing benefit; next year feels the outflow.

Common Drivers

- Estimated payments vs. final tax liability

- Profit growth (higher taxes accruing)

- Tax credits or deductions applied late

- Prior year adjustments or audits

- Installment schedule timing

Fast-growing profitable firms often show increases.

How It Fits in Cash Flow

Indirect method operating section:

- Net Income (after tax expense)

-

- Increase in Income Tax Payable (or − Decrease)

- = Closer to actual cash from operations

It’s a working capital adjustment for tax payment timing.

What a Change Tells You

- Rising → cash conservation on taxes (OCF positive)

- Falling → settling past taxes (cash outflow)

- Link to profitability and effective tax rate

- Conservative vs. aggressive estimated payments

- Future cash tax implications

Compare to current tax expense for insight into payment aggressiveness.

Q · 01Why do profitable companies often show rising income tax payable?+

Q · 02How do tax credits affect the change in income tax payable?+