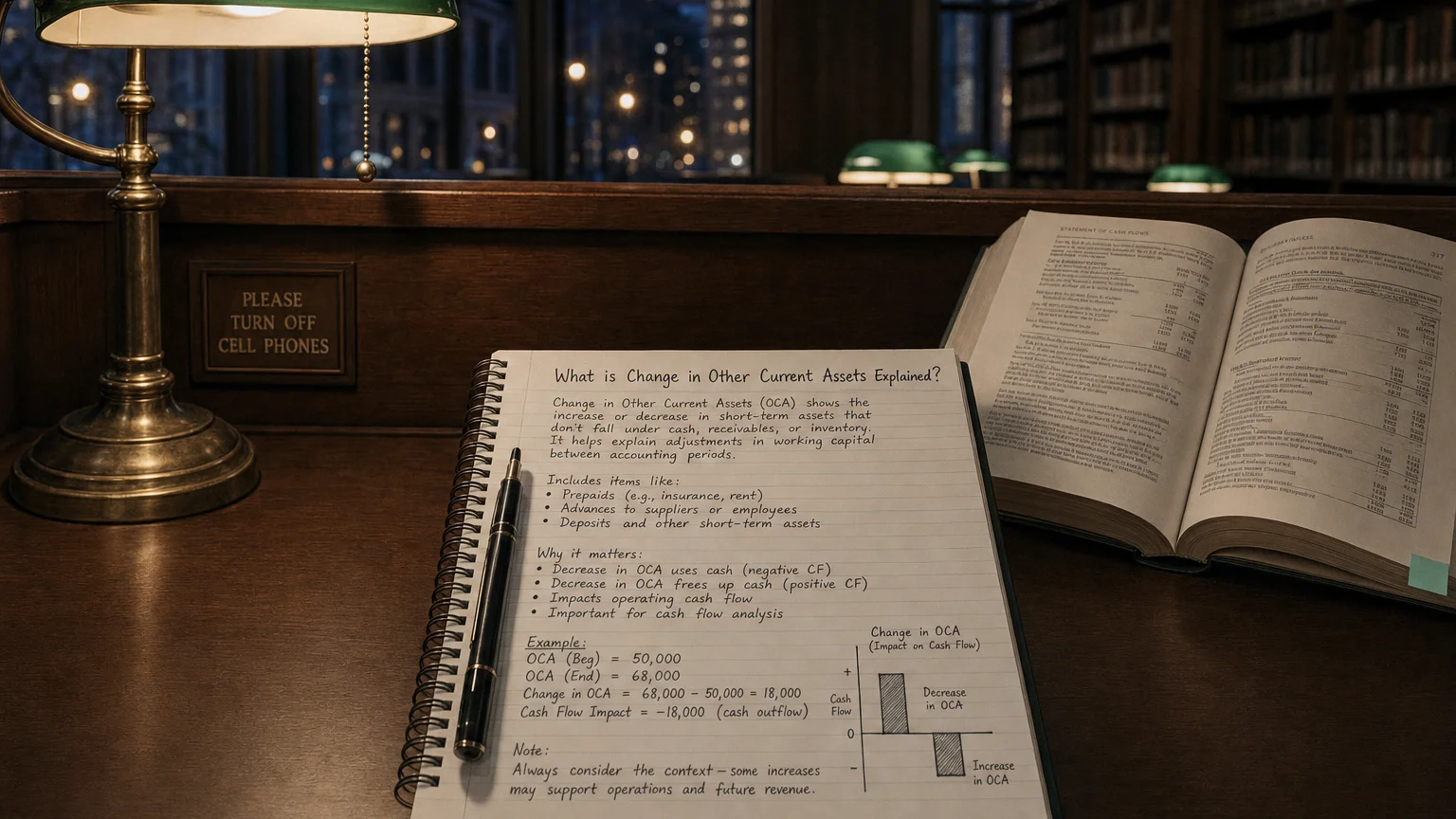

‘”Change in other current assets” captures the period-over-period shift in miscellaneous short-term assets such as prepaid expenses and other receivables. An increase is a cash outflow; a decrease is a cash inflow under Operating Activities.’

You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.

“Other current assets” is a catch-all category on a company’s balance sheet for small or unusual short-term assets that don’t fit under the main headings like cash, accounts receivable, or inventory. The “change in other current assets” on the cash flow statement reflects how the total of these miscellaneous assets moved from one period to the next. This line item is a key adjustment in the operating activities section that captures cash tied up in (or freed up from) these minor asset items.

What’s Included in Other Current Assets?

“You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

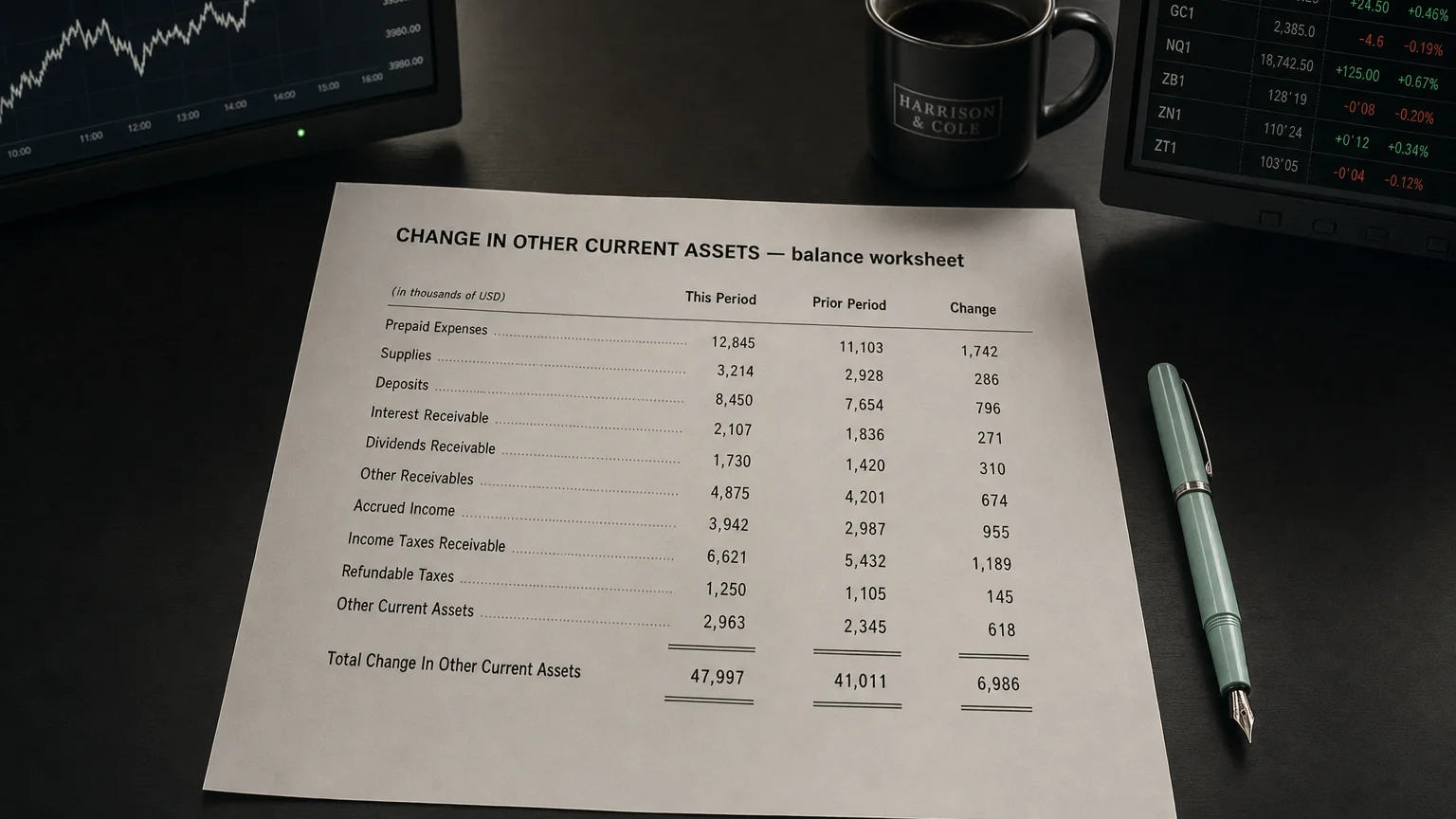

This category aggregates various short-term assets that are expected to be converted to cash within a year but are not significant enough to be listed individually. Common examples include:

- Prepaid Expenses: Payments made in advance for goods or services to be received in the future, such as prepaid rent, insurance, or subscriptions.

- Deferred Tax Assets: The potential future reduction in income taxes, arising from temporary differences between tax accounting and financial accounting.

- Other Receivables: Amounts due to the company outside of its primary trade receivables, such as interest receivable, tax refunds, or rent receivable.

- Advances and Deposits: Small cash advances to employees or suppliers, or security deposits paid to vendors.

The Impact on Cash Flow

The impact on cash flow follows the standard logic for assets. An increase in an asset represents a use of cash, while a decrease represents a source of cash. This is because acquiring an asset (even a prepaid one) requires a cash payment.

The Core Rule

Where It Appears and Why It Matters

On the statement of cash flows (using the indirect method), “Change in other current assets” appears under Operating Activities. It’s one of the working capital adjustments used to reconcile net income to net cash from operations. A typical presentation looks like this:

- Net Income

- Plus: Depreciation & Amortization

- Change in Accounts Receivable

- Change in Inventories

- Change in Other Current Assets

- Change in Accounts Payable

- …

This line is reported separately to capture timing differences between accrual accounting and cash transactions that don’t fit into the main categories. While often small, a large change can signal unusual activity, such as a major prepayment. Significant shifts are typically explained in the financial statement footnotes.

Calculation and a Real-World Example

The change is calculated as the difference between the beginning and ending balances of the ‘Other Current Assets’ account. To reflect the cash impact correctly on the statement, the formula is often presented as:

Formula:

Calculation Example

If a company had 1,333 this year, the balance decreased. The cash flow adjustment would be 1,333 = **+133 cash inflow.

Real-World Example: Laugh Radio Inc.

In its cash flow statement, Laugh Radio Inc. reported **Change in other current assets: (10,000 during the period, consuming that amount of cash.

Q · 01“What items are included in other current assets?”+

Q · 02“Why does an increase in other current assets reduce operating cash flow?”+

Q · 03“How is the cash flow impact of other current assets calculated?”+