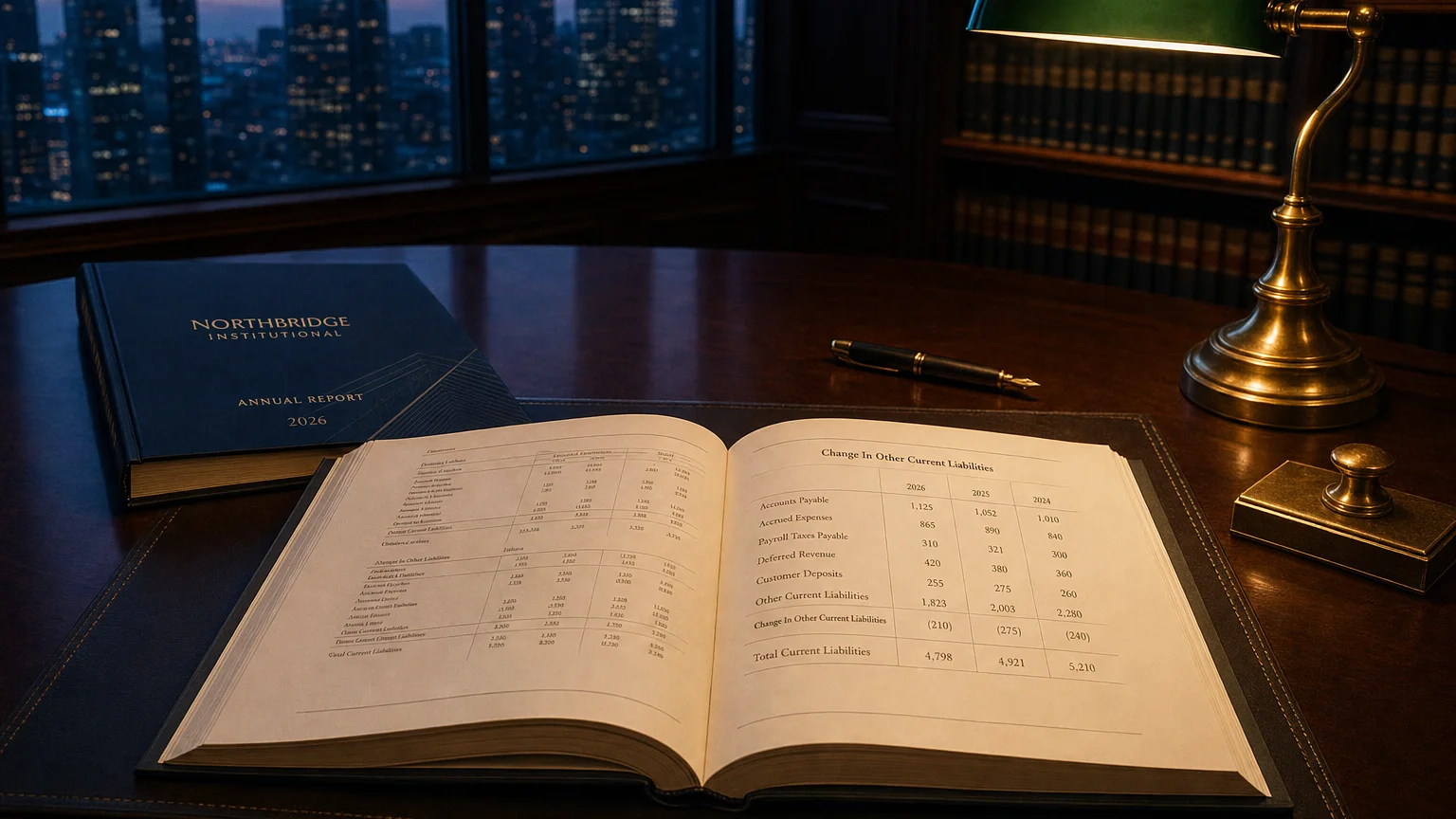

”Change in other current liabilities” is the net shift in miscellaneous short-term obligations such as accrued wages and deferred revenue. An increase signals retained cash; a decrease signals cash paid out in Operating Activities.

It does not matter how frequently something succeeds if failure is too costly to bear.

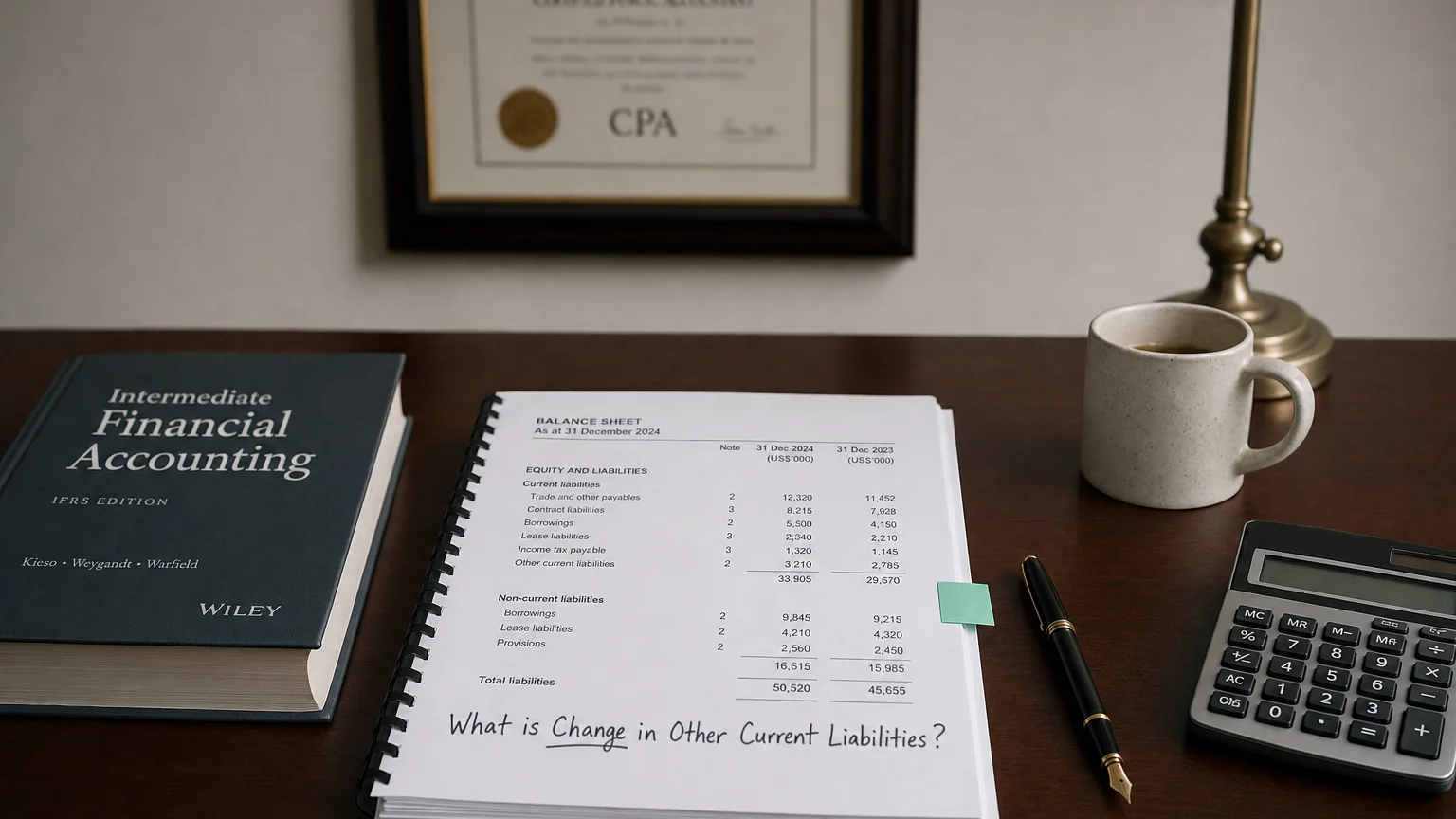

On the cash flow statement (using the indirect method), “Change in Other Current Liabilities” refers to the net increase or decrease in short-term obligations that are not listed under major categories like accounts payable or short-term debt. It functions as a catch-all line for miscellaneous liabilities due within one year that are too small or diverse to be shown separately. These are often grouped as “Other Current Liabilities” on the balance sheet.

What’s Included in Other Current Liabilities?

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

This category aggregates various short-term obligations that a company has incurred but not yet settled. Common examples include:

- Accrued expenses: Obligations for goods or services already received but not yet paid (e.g., wages payable, interest payable, taxes payable).

- Customer deposits / deferred revenue: Cash received from customers before the delivery of goods or services (e.g., unearned revenue, gift card balances, advance payments).

- Dividends or distributions payable: Dividends that have been declared by the company but not yet paid to shareholders.

- Other short-term obligations: This can include items like payroll tax liabilities, product warranty reserves, or provisions for pending legal liabilities.

Companies typically provide more detail about what constitutes their ‘other current liabilities’ in the footnotes to their financial statements.

How It Impacts Cash Flow

The impact on cash flow is straightforward and follows the standard logic for liabilities. An increase in other current liabilities during a period is treated as a source of cash (a cash inflow), while a decrease is treated as a use of cash (a cash outflow).

The Core Rule

If the company owes more in miscellaneous liabilities at the end of the year than it did at the beginning, it has effectively held onto cash. If it paid down these obligations, it used cash. In short: Increase in liabilities = + cash inflow; Decrease in liabilities = - cash outflow.

Location and Purpose on the Cash Flow Statement

You will find this line item in the Operating Activities section when a company uses the indirect method to prepare its cash flow statement. It is one of the adjustments to working capital used to reconcile net income to net cash from operations.

Companies group these liabilities to keep the financial statements from becoming cluttered. Major liabilities like accounts payable and short-term debt get their own lines. Everything else is bundled into this ‘other’ category for simplicity. In a typical cash flow reconciliation, you might see:

- Net Income

- Add back: Depreciation

- Change in accounts receivable (-)

- Change in inventory (-)

- Change in accounts payable (+)

- Change in other current liabilities (+)

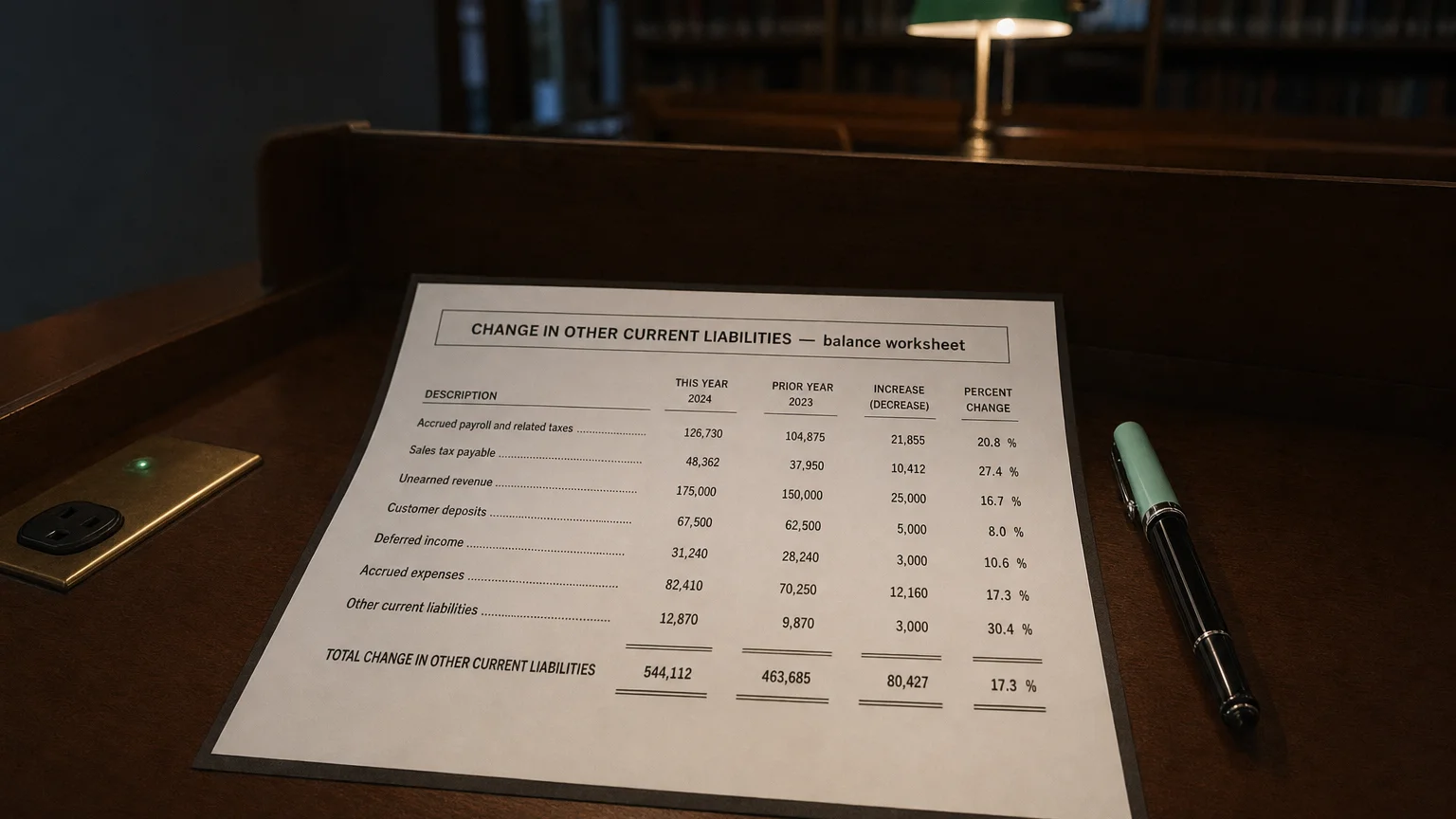

Calculation and Example

The calculation is a simple period-over-period comparison. You take the ending balance of ‘Other Current Liabilities’ from the current period’s balance sheet and subtract the beginning balance from the prior period’s balance sheet.

Formula:

Example Scenario

Suppose a company’s ‘Other Current Liabilities’ balance on December 31, 2024, was 100,000. The change is an increase of 20,000 cash inflow** from ‘Change in Other Current Liabilities’.

Q · 01“What falls under other current liabilities on the balance sheet?”+

Q · 02“Why does an increase in other current liabilities add to operating cash flow?”+

Q · 03“How do analysts use this line item to assess cash flow quality?”+