“Change in payables and accrued expense is the net period-over-period shift in accounts payable plus accrued liabilities. An increase signals delayed cash outflows and adds to operating cash flow; a decrease means the company settled obligations, reducing it.”

You can't take the same actions as everyone else and expect to outperform.

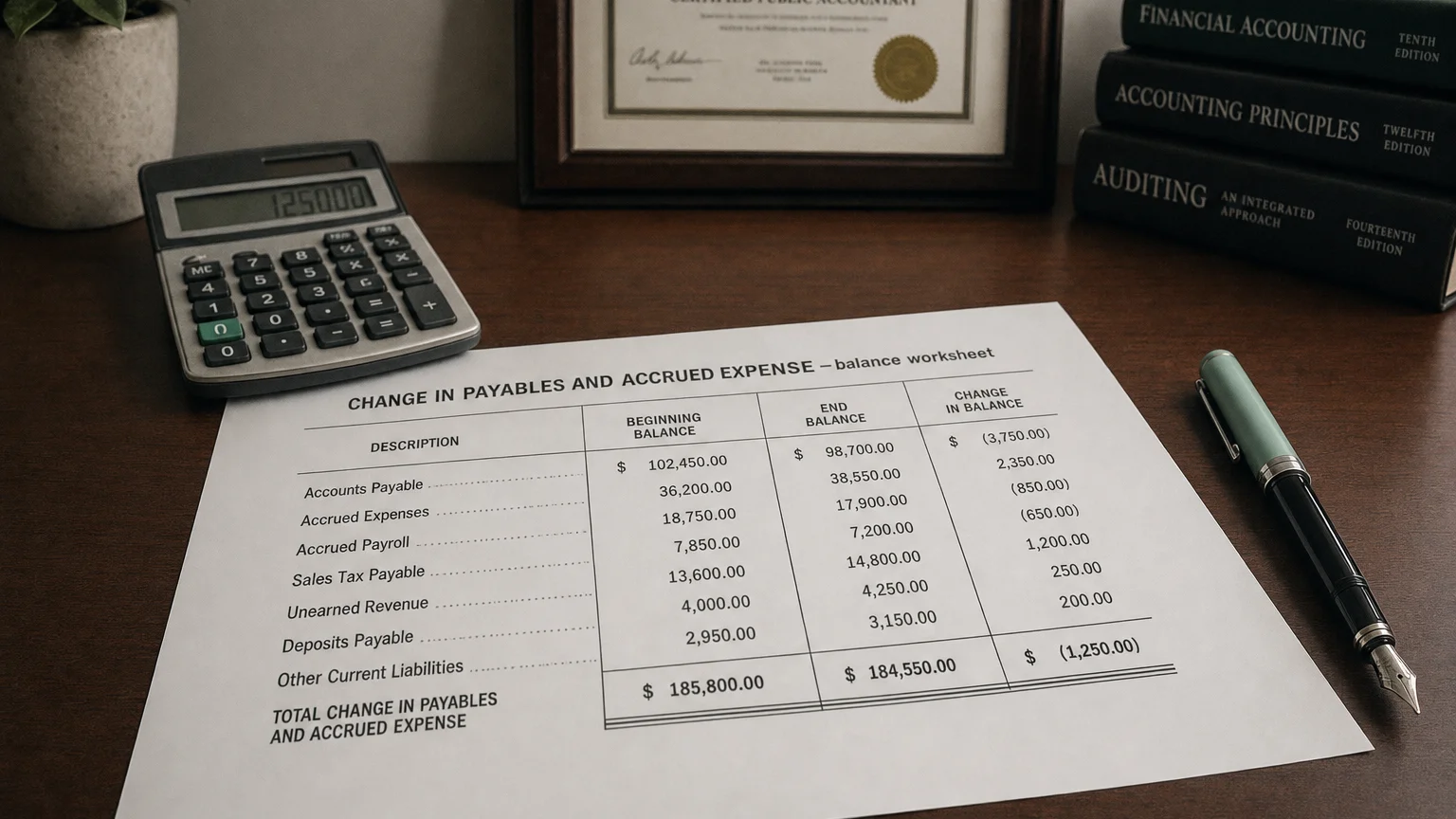

“Change in payables and accrued expenses” on the cash flow statement represents the net change in a company’s short-term obligations from one period to the next. It combines Accounts Payable (amounts billed by suppliers) and Accrued Expenses (costs incurred but not yet paid, like wages or utilities). This single line measures how much a company’s total unpaid operational liabilities have increased or decreased, providing insight into its cash management.

Understanding the Components

“You can’t take the same actions as everyone else and expect to outperform.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘Dare to Be Great’ (2006)

This line item aggregates two types of short-term liabilities:

- Accounts Payable (AP): These are formal bills or invoices a company has received from its suppliers for goods or services but has not yet paid.

- Accrued Expenses (Accrued Liabilities): These are expenses that the company has incurred during a period but for which it has not yet received a bill or made a payment. The expense is recognized, but the cash is still on hand.

Common examples of accrued expenses include:

- Wages/Salaries: Payroll for work done by employees this period that will be paid in the next period.

- Utilities and Rent: Electricity, water, or rent used during the period but billed after the period ends.

- Interest Expense: Interest that has built up on debt between payment dates.

- Taxes: Income, property, or sales taxes owed for the period but not yet paid to the government.

- Commissions or Bonuses: Sales commissions earned or bonuses declared that have not yet been disbursed.

How It Affects Cash Flow

Changes in these liabilities directly affect cash flow because of timing differences. When payables or accruals increase, it means the company has recognized expenses on its income statement but has not yet paid cash for them. This delay in payment retains cash in the business.

The Simple Rule

Presentation on the Cash Flow Statement

This adjustment appears in the Operating Activities section when using the indirect method. It is a critical part of reconciling accrual-based net income to actual cash from operations.

Sample Cash Flow Presentation

A simplified statement might look like this:

Net Income: 10,000 Changes in working capital: Change in Accounts Receivable: -15,000 Change in Accounts Payable & Accrued Expenses: +35,000

Here, the $5,000 increase in payables was added back, boosting the final cash flow figure.

Calculation and Real-World Examples

The calculation is simply the difference between the ending and beginning balances of the combined accounts payable and accrued expenses.

Formula:

Example: LGI Homes

Homebuilder LGI Homes disclosed a +€15 million change in payables and accrued expenses in 2024. This means its combined obligations increased, acting as a €15 million cash source for the year. Conversely, its Q1 2025 report showed a change of -€9M, meaning the balance fell and €9 million in cash was used to pay down these liabilities.

Why This Metric Matters for Analysis

This line item offers valuable insights into a company’s working capital management and liquidity. It reveals whether a business is strategically delaying payments to suppliers to conserve cash or, conversely, using cash to pay down its bills promptly. A consistently rising payables balance might indicate strong negotiating power with suppliers or, in a negative light, potential cash flow problems. A falling balance shows cash is being used to settle liabilities, which could be a sign of healthy operations or pressure from suppliers for faster payment. Understanding this line is crucial for assessing a company’s short-term cash needs and operational health.

Q · 01“How does an increase in payables and accrued expenses boost cash flow?”+

Q · 02“What does a falling payables balance signal to analysts?”+