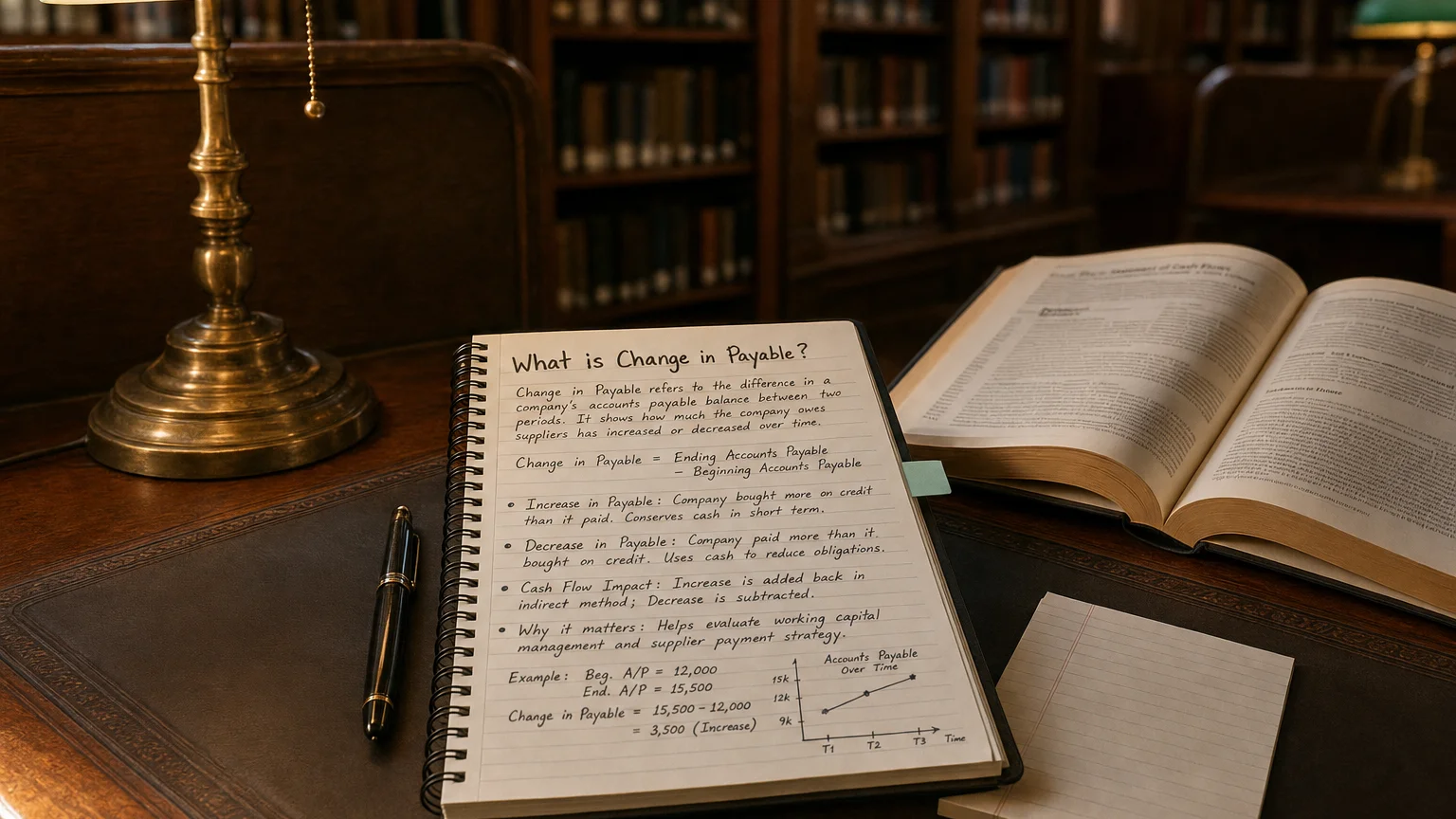

"Change in payable" is the period-over-period difference in a company's accounts payable balance. An increase means the company deferred supplier payments, adding cash to operating activities; a decrease means it paid down obligations, reducing cash from operations.

In the short run, the market is a voting machine. In the long run, it is a weighing machine.

In the context of a cash flow statement, “change in payables” usually refers to the change in a company’s Accounts Payable (AP) balance over an accounting period. Accounts payable represents the short-term obligations a company owes to its suppliers for goods or services that have been received but not yet paid for. The change in payables is simply the difference in the AP account balance from one period to the next, capturing how much more or less the company owes its suppliers.

Why Changes in Payables Affect Cash Flow

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

Changes in accounts payable affect cash flow because of the timing difference between accrual accounting (which records expenses when incurred) and cash accounting (which records when cash actually moves). An increase in accounts payable means some expenses on the income statement were not paid in cash during the period. In effect, the company held onto that cash, so its actual cash balance is higher than net income alone would suggest. Conversely, a decrease means the company used cash to pay off prior obligations. These adjustments are essential for reconciling accrual-based net income to actual cash flow.

Increase vs. Decrease: Cash Inflow or Outflow?

The Core Rule

Put simply, an increase in payables provides cash by deferring payments, whereas a decrease uses cash to settle prior obligations.

Where to Find It on the Cash Flow Statement

On a Statement of Cash Flows prepared using the indirect method, the change in accounts payable appears in the Operating Activities section. This section starts with net income and then adjusts for non-cash items and changes in working capital accounts—like receivables, inventory, and payables—to arrive at net cash from operations.

Note on the Direct Method

This explicit ‘Change in AP’ line appears when using the indirect method. In the less common direct method, the effect of accounts payable is embedded within a line item like ‘cash paid to suppliers’ rather than shown as a separate adjustment.

Calculation and Common Examples

The change is calculated as the difference in the accounts payable balance between the beginning and end of the accounting period.

Formula:

For instance, if Accounts Payable was 120,000 this year, the change is a +$20,000 increase. This would be added to net income as a cash source. Accounts payable generally consists of day-to-day bills and invoices, such as:

- Inventory or Raw Materials Purchases on Credit: Goods bought from suppliers without immediate payment.

- Utilities and Bills Pending Payment: Expenses like electricity, water, or internet that have been incurred but not yet paid.

- Office Supplies and Equipment on Credit: Unpaid invoices for supplies or maintenance services.

- Services Received from Third Parties: Billed amounts for consulting, legal, or subcontracting services that are awaiting payment.

Why It’s Important for Analysis

The ‘change in payables’ line provides crucial insight into a company’s operational cash management and short-term liquidity.

- Liquidity Management: An increase in payables boosts cash in the short run. Effectively using supplier credit is a common cash management strategy, allowing a business to finance some of its operations through its creditors.

- Timing of Disbursements: The change indicates whether the company is delaying or accelerating payments. A large increase might mean the company is stretching out payments, which conserves cash but could strain supplier relationships. A large decrease shows the company is paying bills faster, which uses cash but may earn early payment discounts.

- Operational Efficiency and Sustainability: Analysts look at this change to assess the quality of cash flow. If cash flow improved mainly because payables shot up, the boost might be temporary. Those bills must eventually be paid. This helps differentiate cash generation from core operations versus generation from simply shifting payment timing.

Example Presentation

Simplified Cash Flow Statement (Indirect Method)

Cash Flows from Operating Activities

Net Income: 10,000 Increase in Accounts Receivable: -15,000 Increase in Accounts Payable: +35,000

In this example, accounts payable increased by $5,000. This is added back to net income because it represents cash that was conserved by deferring payments to suppliers.

Q · 01Does an increase in accounts payable improve or hurt cash flow?+

Q · 02What does a declining accounts payable balance indicate to analysts?+

Q · 03Where does change in payable appear on the cash flow statement?+