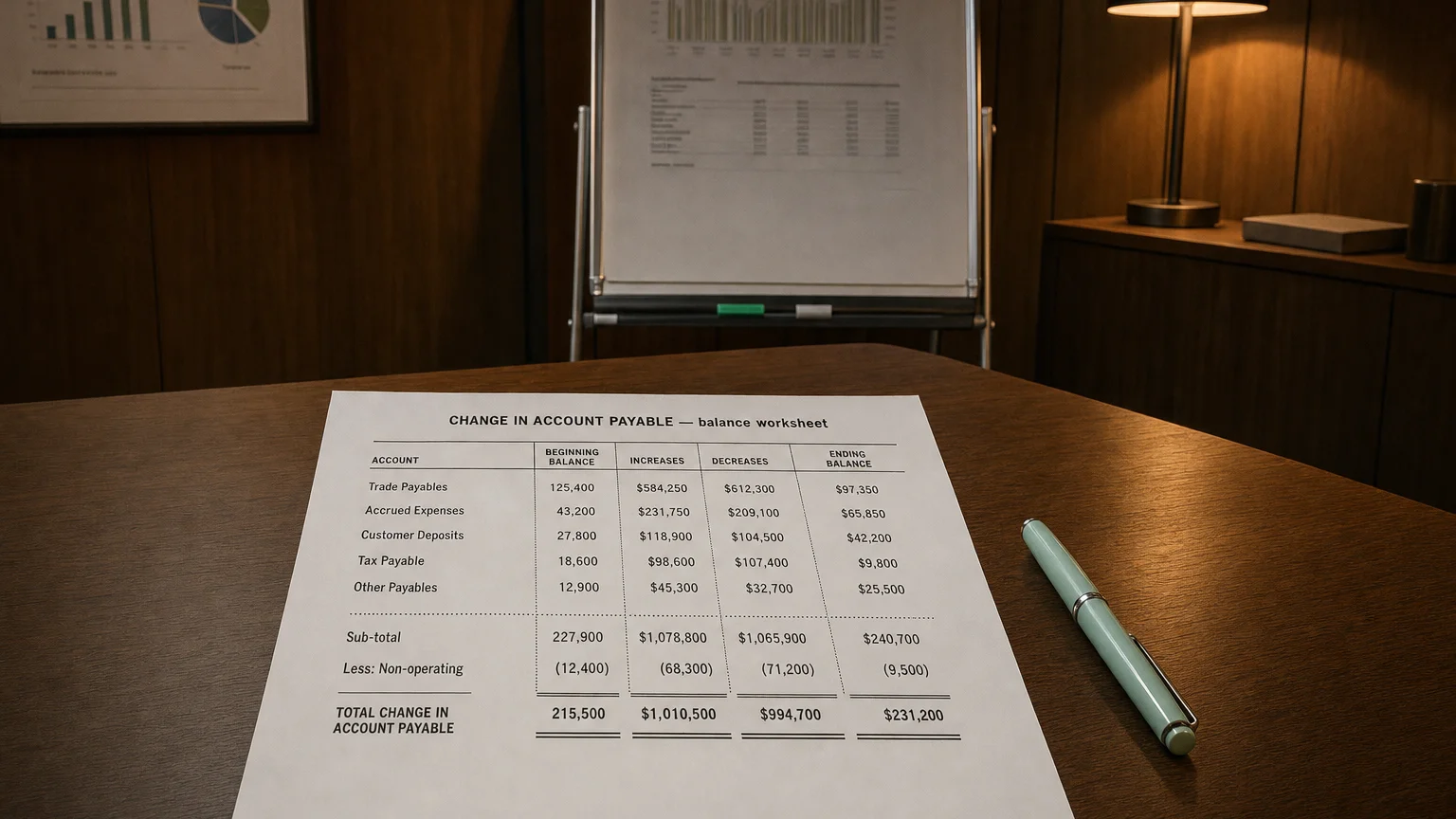

Change in accounts payable is the period-over-period difference in amounts owed to suppliers. An increase in AP adds to operating cash flow; a decrease subtracts from it.

The stock market is a device for transferring money from the impatient to the patient.

Change in accounts payable refers to the period-over-period difference in a company’s accounts payable (AP) balance—that is, how much the amount owed to suppliers has increased or decreased. Accounts payable itself is the short-term liability for goods or services a company has received on credit but has not yet paid for. The cash flow statement captures the change in this liability because it directly impacts the actual cash the company retains or uses during the period.

What Makes Up Accounts Payable?

Accounts payable arise from ordinary business expenses that are billed to the company and due at a later date. Common examples include:

- Inventory or raw materials on credit: Supplier invoices for stock or materials that the company will pay for in the near term.

- Utilities and facility expenses: Unpaid bills for electricity, water, internet, and other utilities that have been used but not yet paid.

- Billed services: Invoices from contractors or vendors for services like consulting, legal, or accounting fees that are outstanding.

- Rent, maintenance, and subscriptions: Owed payments for monthly rent, maintenance fees, and other recurring services.

The Link Between Accounts Payable and Cash Flow

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Annual Report (1999)

Changes in AP affect the cash flow statement because of timing differences between when expenses are recorded (accrual basis) and when cash is paid. The indirect method cash flow statement starts with net income and must adjust for these non-cash changes. If a company incurred expenses but hasn’t paid the bills, it saved cash relative to its reported profit. This adjustment converts the accrual-based profit to a true cash flow figure.

Increase vs. Decrease: A Source or Use of Cash?

The Core Rule

This may seem counterintuitive, but from a cash perspective, higher payables mean the company held onto its cash longer.

How It’s Calculated and Presented

The change in AP is calculated by comparing the balance at the beginning of a period to the balance at the end. It’s found in the Operating Activities section of the cash flow statement, grouped with other working capital adjustments.

Formula:

For example, if last year’s ending AP was 120,000, the change is a +$20,000 increase, which is added to operating cash flow.

What It Reveals About a Company

The change in accounts payable provides deep insight into a company’s cash management strategies and operational health.

- Working Capital Management: A rising AP balance shows the company is using supplier credit to finance its short-term operations, which can be an effective way to improve liquidity. However, an unusually large jump could be a red flag for cash shortages.

- Payment Speed and Supplier Relations: A falling AP balance means the company is paying its suppliers faster. This uses cash but can help maintain good vendor relationships or take advantage of early payment discounts. Conversely, stretching payments too long can harm a company’s credit rating and strain supplier relationships. Analysts often use metrics like Days Payable Outstanding (DPO) to gauge if a company’s payment pace is healthy.

Interpreting Real-World Examples

Example: Apple Inc. (Fiscal 2017)

Apple reported a **9.6 billion in cash by deferring payments to its suppliers, which significantly boosted its cash flow from operating activities for the year.

Example: Company XYZ

If Company XYZ starts the year with 65,000, the 15,000 in the operating section. If instead, AP had dropped to 20,000 decrease), it would be shown as -$20,000, representing a cash use.

Q · 01Why does an AP increase improve operating cash flow?+

Q · 02How do analysts use Days Payable Outstanding alongside AP changes?+