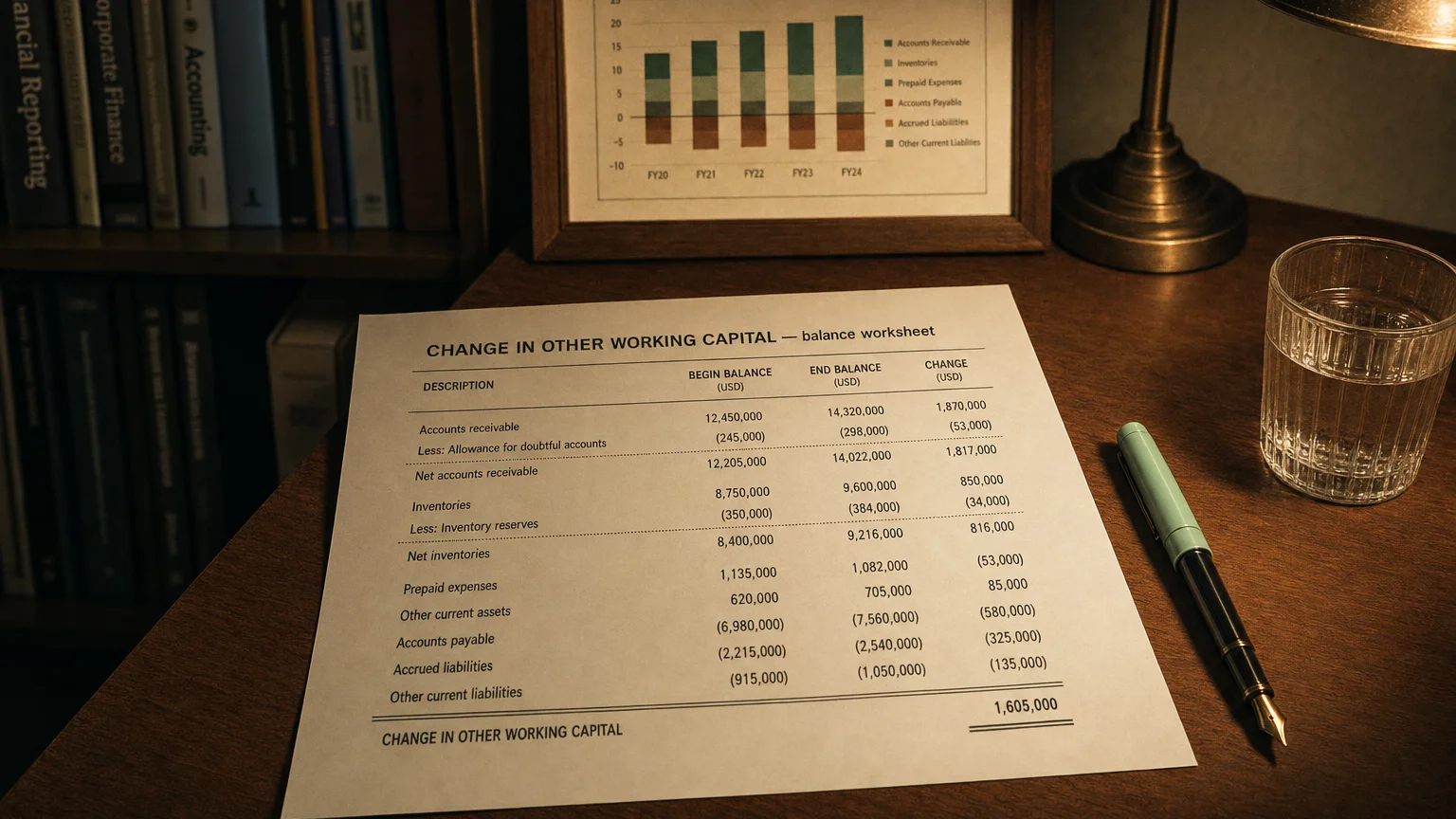

”Change in other working capital” is the net cash impact of miscellaneous current assets and liabilities — prepaid expenses, accrued taxes, deferred revenue — not listed separately. A positive figure provides cash; a negative figure consumes it.

The stock market is filled with individuals who know the price of everything but the value of nothing.

“Change in Other Working Capital” refers to the net change in miscellaneous current operating assets and liabilities not explicitly broken out elsewhere on the cash flow statement. After accounting for major items like accounts receivable, inventory, and accounts payable, the remaining current items (like prepaid expenses, other receivables, accrued taxes, and deferred revenue) are grouped together into this single line item. It captures all the small or miscellaneous adjustments needed to reconcile net income to cash flow.

What’s Included vs. Excluded

“The stock market is filled with individuals who know the price of everything but the value of nothing.”

— Philip Fisher, Author, Common Stocks and Uncommon Profits Common Stocks and Uncommon Profits (1958)

The primary working capital accounts are typically shown as their own line items on the cash flow statement. These include:

- Change in Accounts Receivable

- Change in Inventory

- Change in Accounts Payable

“Change in Other Working Capital” then captures the net effect of all other operating current assets and liabilities. Common items bundled into this category include prepaid expenses, deferred revenue, accrued expenses (like taxes, interest, or wages payable), and customer deposits.

Cash Impact and Calculation

The cash impact follows the standard rules of working capital. An increase in an ‘other’ current asset or a decrease in an ‘other’ current liability represents a use of cash (a negative adjustment). Conversely, a decrease in an ‘other’ current asset or an increase in an ‘other’ current liability is a source of cash (a positive adjustment).

Formula:

Simple Rule

If other assets rise or other liabilities fall, the change is negative (cash used). If other assets fall or other liabilities rise, the change is positive (cash provided).

Location and Purpose on the Cash Flow Statement

This line item appears in the Operating Activities section of the cash flow statement (when using the indirect method). It is one of the key adjustments that reconciles a company’s net income to its net cash from operations.

Companies aggregate these accounts primarily for simplicity and clarity. Grouping them prevents the cash flow statement from becoming cluttered with numerous small, variable line items. As UncleStock notes, this line is “one of the major ways that net income and operating cash flow can differ”. While often minor, analysts watch for large swings in this line, as they could indicate unusual one-time effects like a large tax prepayment or a change in customer deposit activity.

Real-World Examples

Arcadis (2024)

The company’s consolidated cash flow statement shows “Change in Other working capital” as +€20 million. This positive number signifies a net source of cash, meaning the company’s other miscellaneous current assets decreased and/or its other current liabilities increased during the period.

Lam Research (2007)

For a nine-month period, Lam Research reported a “Change in other working capital accounts” of **-60.5 million**. This negative figure represents a cash outflow. The company's MD&A explained that this was partly due to an increase in “other current assets” (like supply prepayments and tax receivables) of 34.9 million, which was a use of cash.

Q · 01“What items are typically bundled into other working capital?”+

Q · 02“How does other working capital differ from the main working capital lines?”+

Q · 03“What does a large negative swing in other working capital signal?”+