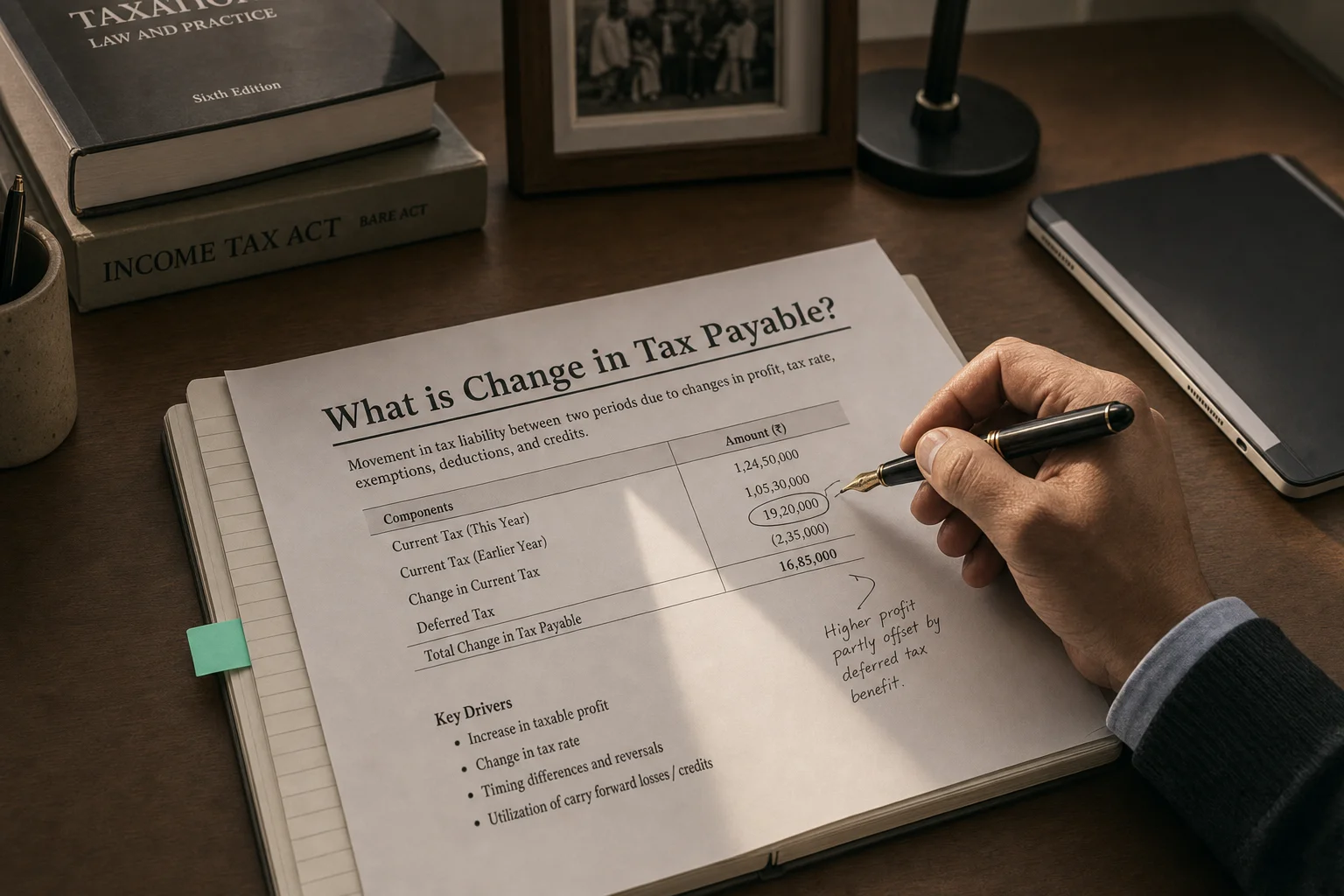

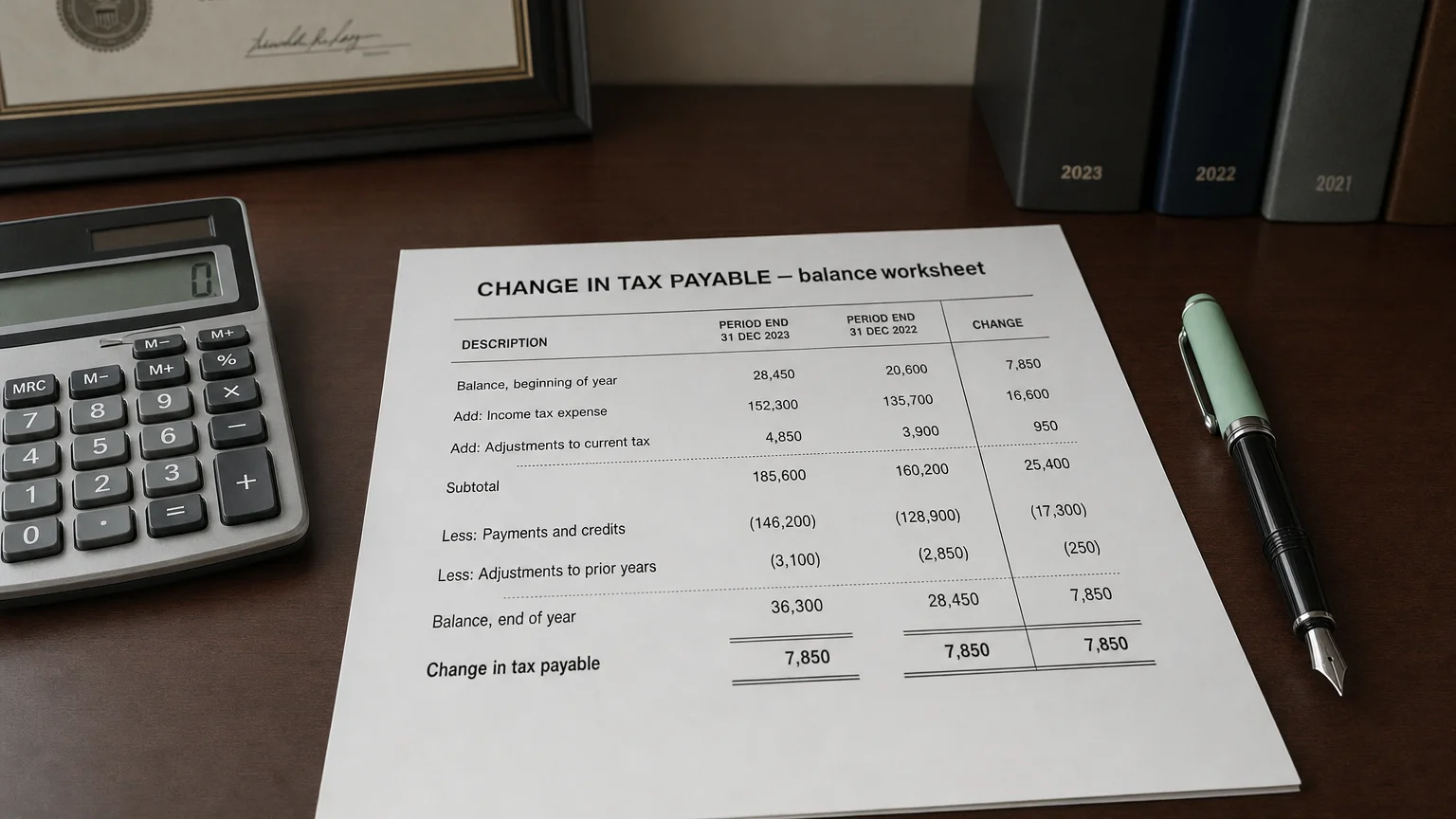

Change in tax payable is the net increase or decrease in current income tax liabilities during the period. An increase adds to operating cash flow because tax expense was recognized without a matching cash payment; a decrease subtracts when prior accruals are settled.

If we avoid the losers, the winners will take care of themselves.

Change in Tax Payable is the net increase or decrease in the company’s current tax liability (primarily income taxes payable) during the reporting period. This line appears in the operating activities section of the indirect-method cash flow statement. An increase adds to operating cash flow (tax expense recognized but cash not yet paid), while a decrease subtracts (paying off prior tax accruals).

What It Really Means

“If we avoid the losers, the winners will take care of themselves.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Tax payable is the current income tax the company owes to governments based on taxable profit. Companies often pay estimated taxes quarterly, but the final liability is settled later.

When tax payable grows, you’ve booked more tax expense than you’ve paid in cash—keeping money longer, boosting operating cash flow. When it shrinks, you’re catching up on past taxes—cash goes out.

A Clear Example

Company estimates and pays 10M owed.

- Tax Payable rises by $2M

- Cash flow this year: +$2M Change in Tax Payable (add-back)

- Next year: Pay the $2M balance

- Next year cash flow: -$2M Change in Tax Payable

This year OCF gets a timing benefit; next year takes the cash hit.

Common Drivers

- Estimated payments vs. final liability

- Tax rate changes mid-year

- Loss carryforwards or credits applied

- Installment payment schedules

- Audit adjustments or prior year true-ups

Profitable growing companies often show increases.

How It Fits in Cash Flow

Indirect method operating section:

- Net Income (after tax expense)

-

- Increase in Tax Payable (or − Decrease)

- = Closer to cash from operations

It’s a working capital adjustment bridging accrual tax to cash tax.

What a Change Tells You

- Rising → conserving cash on taxes (OCF boost)

- Falling → paying down past taxes (cash outflow)

- Link to effective tax rate and profitability

- Timing of estimated payments

- Potential future cash tax burden

Compare to current tax expense for payment pattern.

Q · 01Why does an increase in tax payable boost operating cash flow?+

Q · 02How do tax rate changes affect the change in tax payable line?+