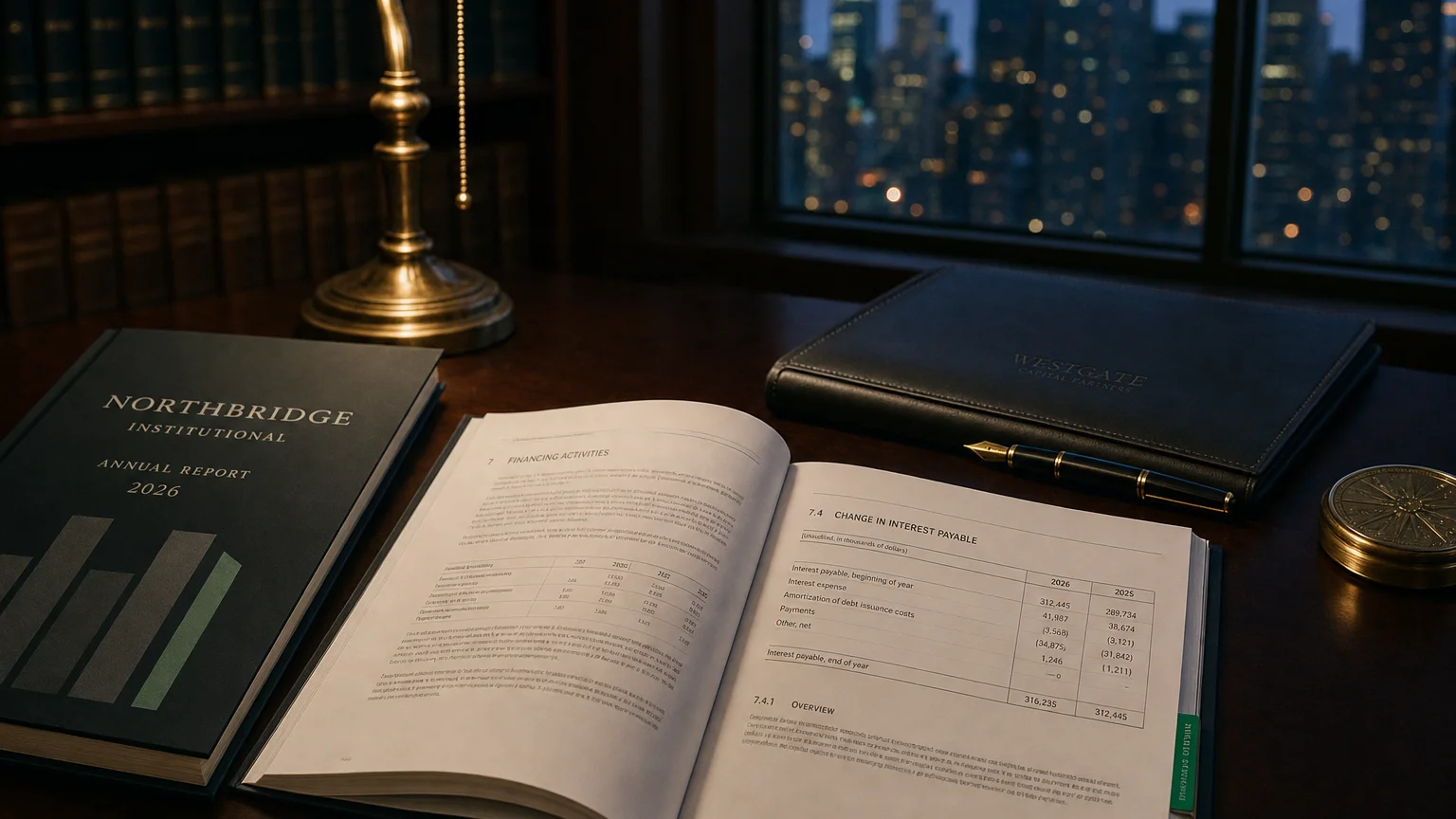

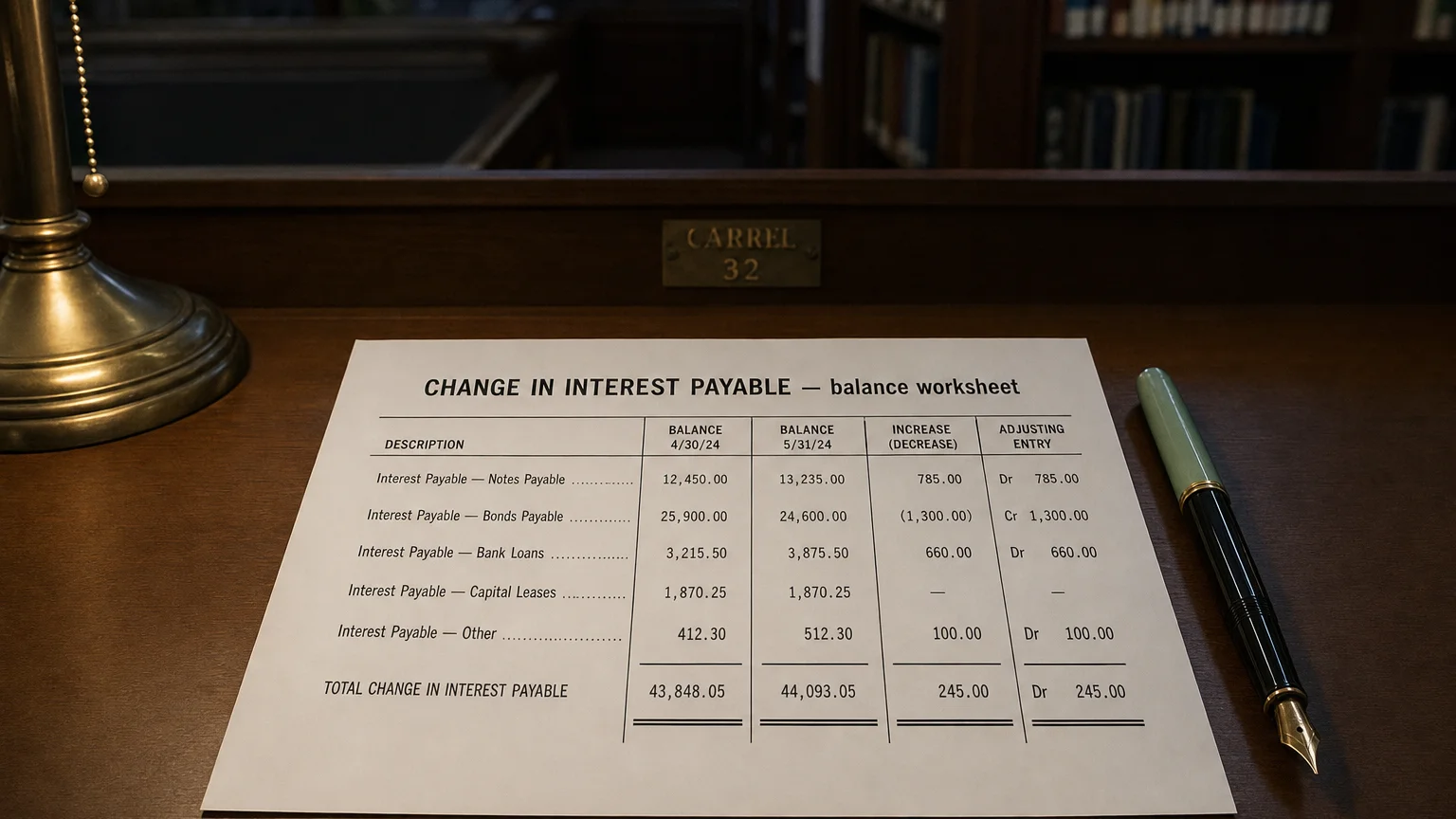

Change in interest payable is the net increase or decrease in accrued interest during the period. An increase adds to operating cash flow as debt interest accrues without an immediate cash payment; a decrease subtracts when prior accruals are settled.

In investing, you get what you don't pay for. Costs matter enormously.

Change in Interest Payable is the net increase or decrease in the accrued interest liability during the reporting period. This line appears in the operating activities section of the indirect-method cash flow statement. An increase adds to operating cash flow (interest expense recognized but cash not yet paid), while a decrease subtracts (paying off prior accrued interest).

What It Really Means

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

Interest payable is the interest you’ve racked up on debt but haven’t paid yet—usually because payments are quarterly or semi-annual.

When this balance grows, you’re recognizing interest expense now but delaying the cash payment—free short-term financing that boosts operating cash flow.

When it shrinks, you’re settling prior accruals—cash goes out the door.

A Straightforward Example

Company has bonds paying interest semi-annually on June 30 and December 31.

- Year-end December 31 → just paid, Interest Payable ≈ $0

- During year: 10M by next June

- Cash flow this year: +$10M Change in Interest Payable (add-back)

- Next June: Pay 0

- Next period cash flow: -$10M Change in Interest Payable

The timing of payment dates drives big swings.

Common Drivers

- Payment schedule timing (quarter-end vs. mid-quarter)

- New debt issued (more interest accruing)

- Debt repayment (less interest accruing)

- Interest rate changes on variable debt

- Seasonal borrowing patterns

Heavy debt companies show larger movements.

How It Fits in Cash Flow

Indirect method operating section:

- Net Income (includes interest expense)

-

- Change in Interest Payable (increase adds back)

- = Closer to actual cash from operations

It’s a working capital timing adjustment.

What a Change Tells You

- Rising → conserving cash on interest (positive for OCF)

- Falling → paying down past interest (cash drain)

- Year-end zero common (just paid)

- Link to debt levels and rates

- Smooth vs. lumpy (payment schedule)

Compare to total interest expense for payment frequency clues.

Q · 01Why does interest payable create a positive OCF adjustment?+

Q · 02How does debt repayment affect future changes in interest payable?+