Other Cash Receipts from Operating Activities is a financial concept covered in this article. Miscellaneous Operating Cash Inflows in Direct Method

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

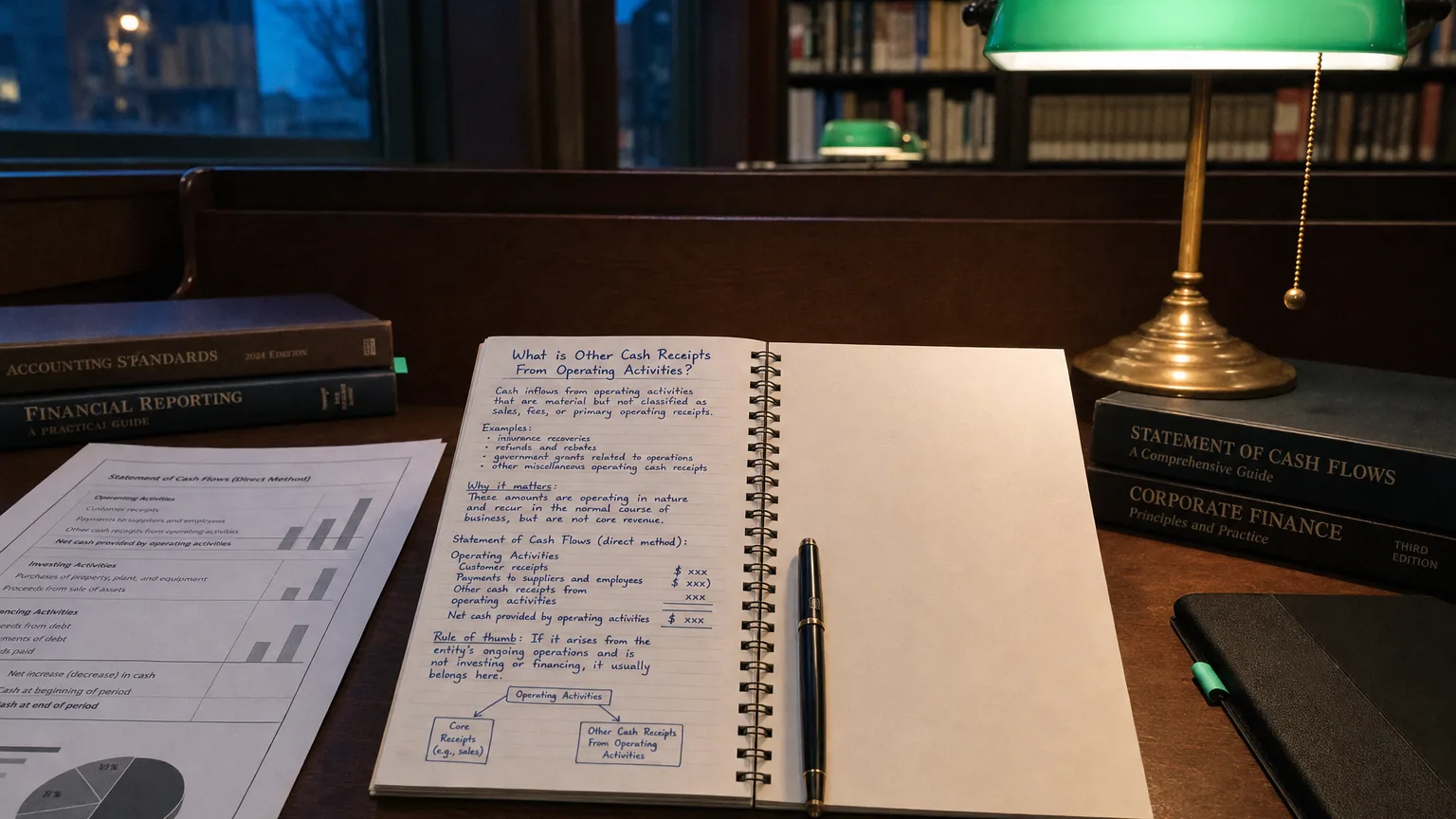

Other Cash Receipts from Operating Activities is the residual line in the direct-method cash flow statement for operating cash inflows that don’t fit into the primary categories like receipts from customers. It captures smaller or varied cash receipts tied to day-to-day business operations, ensuring all significant operating cash sources are disclosed transparently.

What It Captures

The direct method lists major operating cash receipt classes separately for clarity. Anything material that doesn’t fit those buckets ends up here.

It’s the ‘everything else’ category—ensuring no big operating cash inflow hides in a lump sum.

Indirect method doesn’t show gross receipts—everything nets into one OCF figure.

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Typical Items Included

- Royalty or license fee receipts

- Insurance recoveries for operating losses

- Government grants or subsidies (non-capital)

- Legal or dispute settlements

- Scrap or by-product sales

- Refund of overpaid expenses

- Franchise fees received

- Miscellaneous operating recoveries

Varies by industry—pharma might have royalties, manufacturers scrap sales.

A Practical Example

Tech company using direct method:

- Receipts from customers: +$1,000M

- Interest received: +$20M

- Other Cash Receipts from Operating Activities: +30M, insurance recovery 5M)

You see the full picture of operating cash sources.

Direct Method Context

In direct method operating section:

- Cash receipts from customers

- Interest received

- Other Cash Receipts from Operating Activities

- Minus payments to suppliers, employees, etc.

- = Net operating cash flow

Gross transparency—every major bucket visible.

Why It Matters

- Complete view of operating cash sources

- Highlights non-customer revenue cash

- Better insight into ancillary income

- Industry-specific cash visibility

- Comparability when peers use direct method

What to Watch For

- Size and growth (rising royalties?)

- Composition (disclosed in notes)

- Trend vs. revenue (diversification?)

- One-time items (insurance recoveries)

- Link to strategy (licensing revenue?)

Large or growing ‘other’ can hide shifting revenue mix.