Interest Received Direct is a financial concept covered in this article. Cash Interest Income in Direct Method Operating Activities

The stock market is filled with individuals who know the price of everything but the value of nothing.

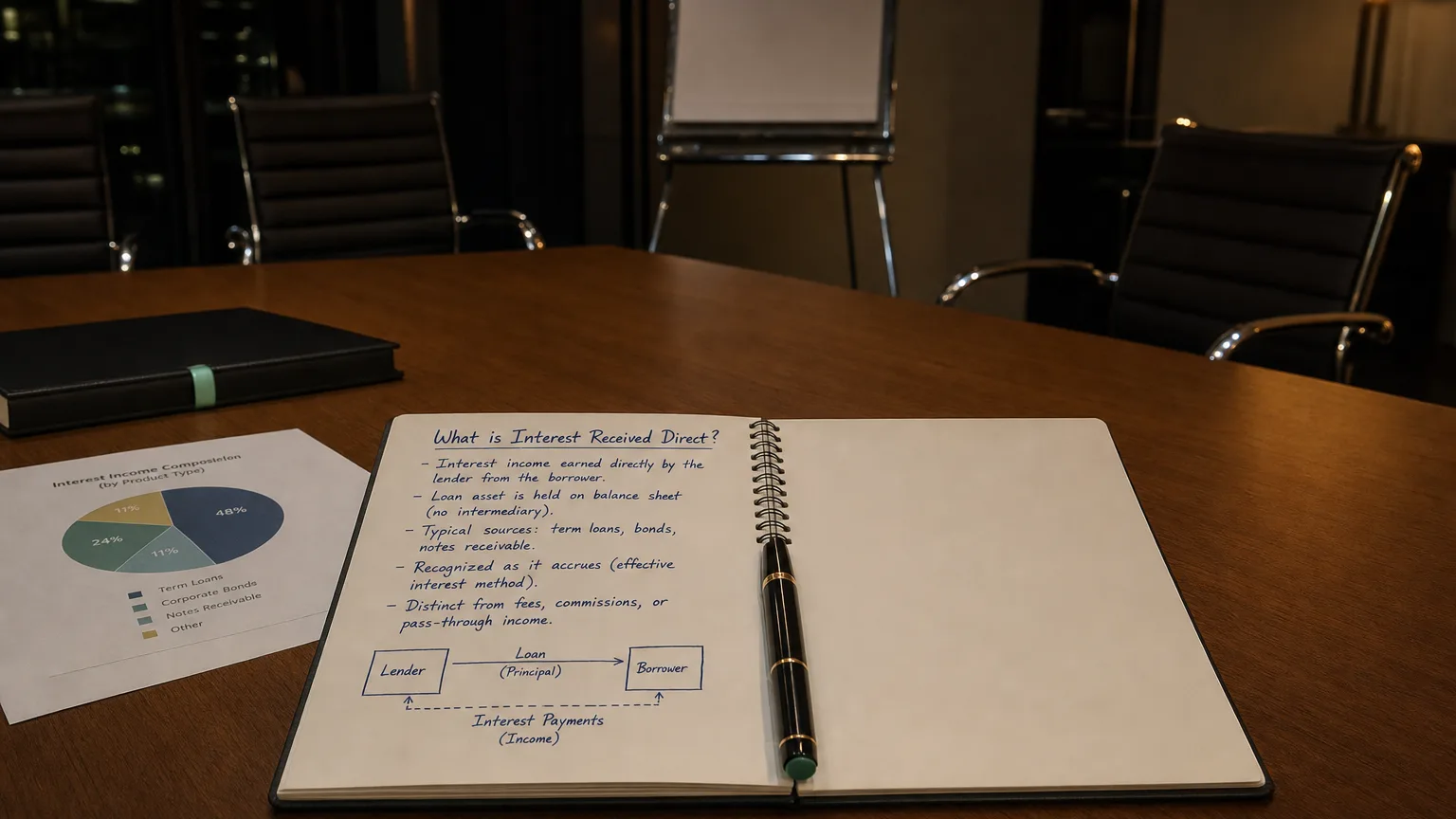

Interest Received Direct is the actual cash inflow from interest earned on loans, debt securities, bank deposits, or other interest-bearing assets, explicitly reported in the direct method presentation of operating cash flows. This classification treats interest received as a gross cash receipt from core or ongoing activities, providing transparency on cash generated from lending or investing activities that support the business.

What It Represents

Interest Received Direct shows the real cash coming in from interest—separate from accrual adjustments.

In the direct method, major cash receipt classes are listed gross, so interest gets its own line when material.

Indirect method buries interest in net income or supplemental notes—no gross visibility.

Common Sources

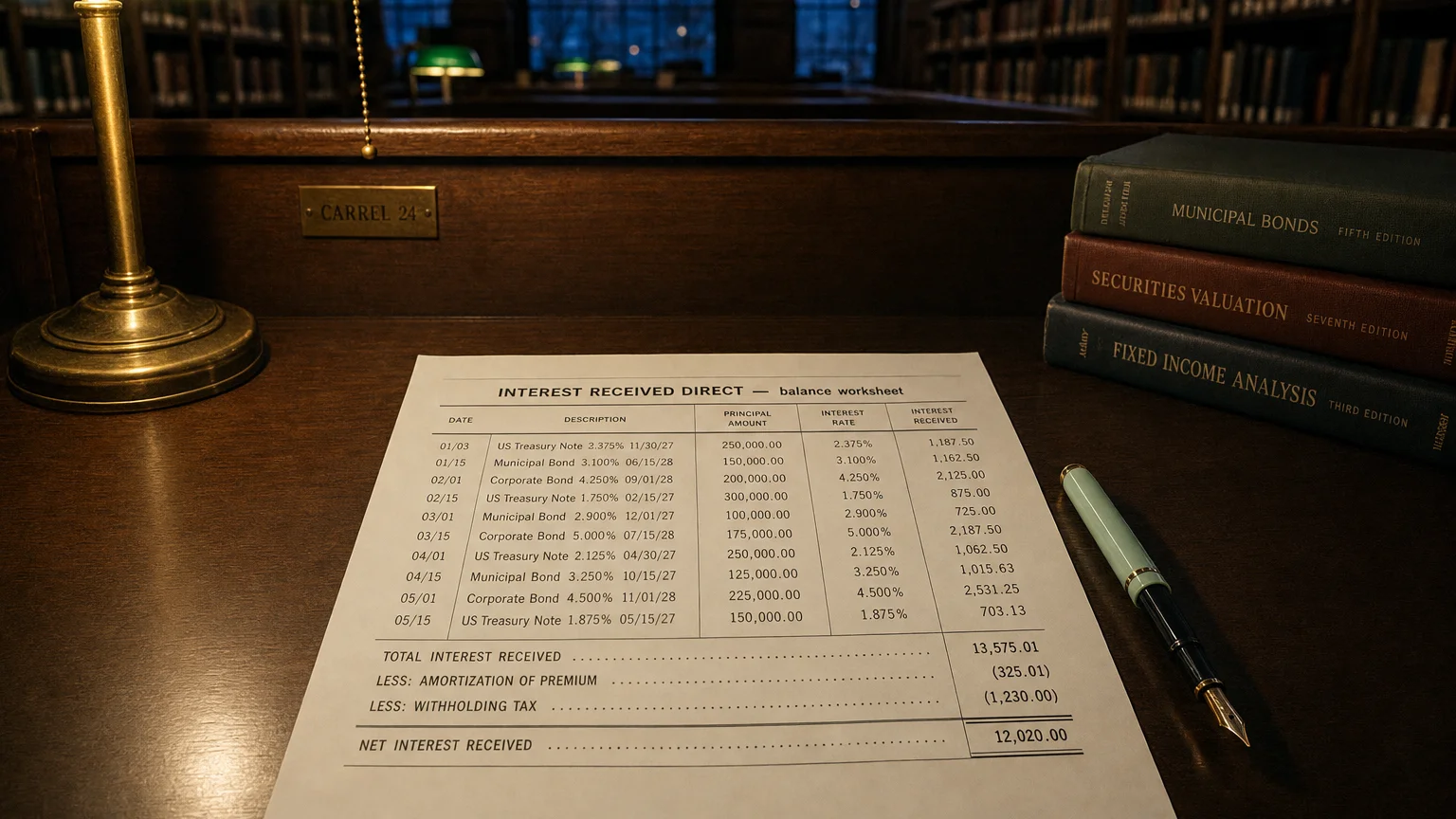

- Interest on customer loans or notes receivable

- Interest from held bonds or debt securities

- Bank deposit or money market interest

- Finance lease interest income

- Intercompany loan interest

Banks show huge numbers—interest is core revenue. Non-financial firms less, but still meaningful if lending/investing heavily.

“The stock market is filled with individuals who know the price of everything but the value of nothing.”

— Philip Fisher, Author, Common Stocks and Uncommon Profits Common Stocks and Uncommon Profits (1958)

A Practical Example

Company has $200M in customer financing loans at 6% average.

- Annual interest accrual: $12M

- Cash actually collected: $11.5M (some accrued)

- Direct method: ‘Interest Received Direct’ +$11.5M

- Clear view of cash timing vs. accrual income

Shows true cash generation from lending.

Direct Method Context

In direct method operating section:

- Cash receipts from customers

- Interest Received Direct

- Other operating receipts

- Minus payments to suppliers, employees, interest paid, taxes

- = Net operating cash flow

Gross transparency—see interest cash separate.

Why It Matters

- Actual cash from interest-earning assets

- Timing differences vs. accrual income

- Contribution to operating cash

- Better insight for financial or lending-heavy firms

- Comparability challenge (most use indirect)

What to Watch For

- Growth vs. interest-bearing assets (collection efficiency?)

- Size relative to interest income (accrual timing)

- Link to loan portfolio growth

- Seasonality or lumpiness

- Comparison to interest paid

Lower cash vs. accrual interest may signal growing receivables or delays.

Q · 01What is Interest Received Direct?+