Interest Received CFO is a financial concept covered in this article. Cash Interest Income Classified as Operating Activities

The intelligent investor is a realist who sells to optimists and buys from pessimists.

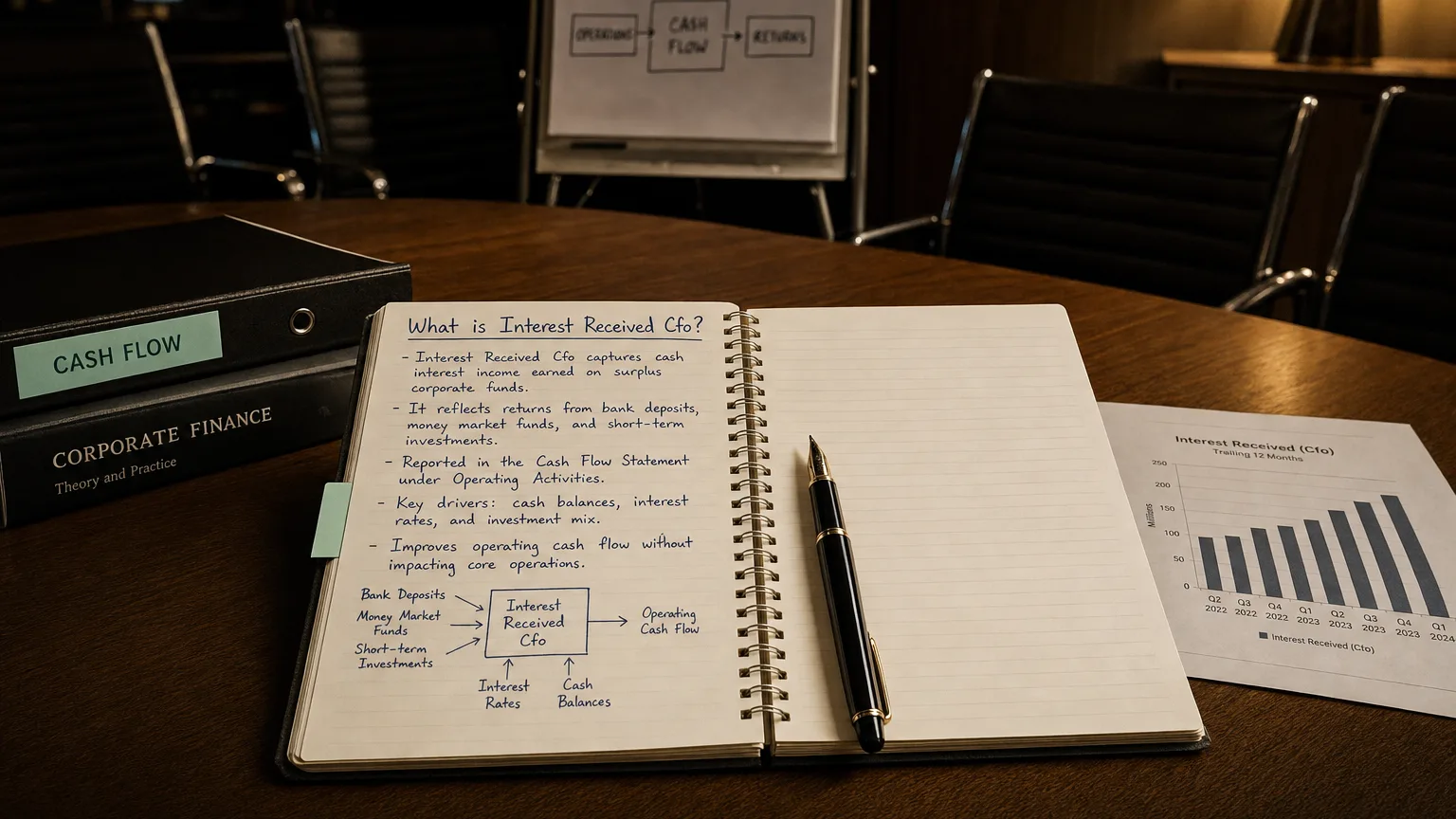

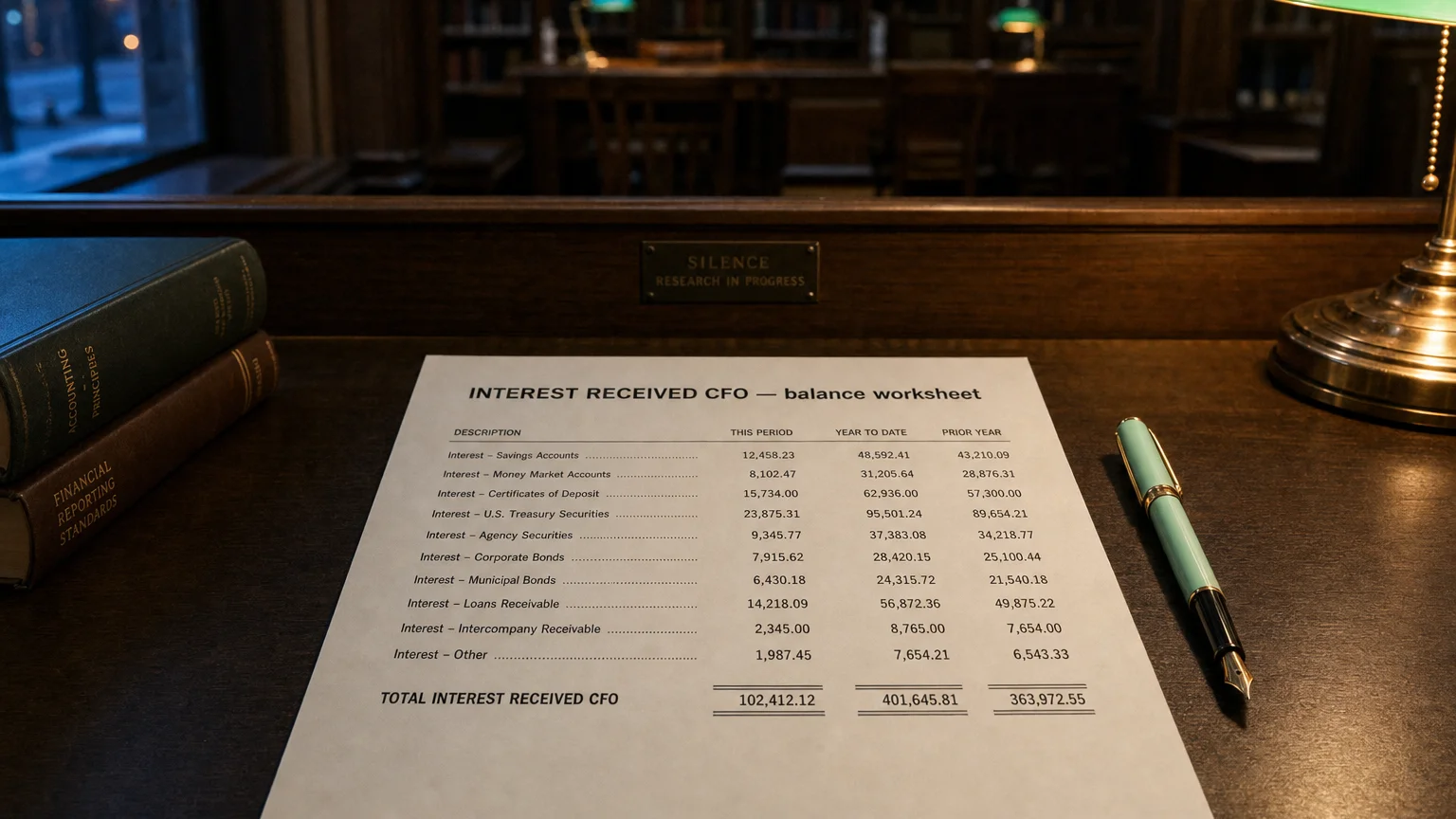

Interest Received CFO (Interest Received – Cash Flow Operating) is the actual cash inflow from interest earned on loans, debt securities, deposits, or other interest-bearing assets that a company classifies in the operating activities section of the cash flow statement. This treatment views interest income as part of core business operations, common under IFRS and for many US non-financial companies.

Why Classify Interest Received in Operating

Under IFRS, interest received must go to operating activities—it’s seen as part of running the business, especially for non-financial firms where lending/investing supports core operations.

Many US companies choose operating too, because it keeps Operating Cash Flow stronger and more reflective of total cash generation from activities.

Contrast: Some US firms put it in investing, viewing interest as return on invested capital.

Financial institutions (banks) almost always operating—interest is their product.

A Clear Example

Company holds $100M in corporate bonds earning 5% interest.

- Annual interest cash: $5 million

- IFRS or Operating choice: +$5M in Operating Activities → OCF higher

- Investing choice: +$5M in Investing Activities → OCF excludes interest

The operating classification makes core cash flow look $5M better.

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

Where It Shows Up

In the cash flow statement operating section:

- ‘Interest Received’

- ‘Cash Received for Interest’

- Direct method: explicit line

- Indirect method: added back or in supplemental

Supplemental note discloses total interest received (policy agnostic).

Who Uses Operating Classification

- All IFRS reporters (mandatory)

- Many US industrials, retailers, tech firms

- Companies emphasizing OCF as key metric

- Firms with interest from operating assets (e.g., finance leases)

Banks/insurers: operating (core business). Non-financial: mixed but leaning operating.

Pros and Cons

Advantages (Operating)

- Higher OCF

- Reflects total cash from operations including financing income

- Consistent with IFRS

Advantages (Investing)

- Purer operating cash (core only)

- Aligns interest with investment returns

What to Watch For

- Policy choice (US GAAP) and consistency

- Size relative to operating income

- Comparison across companies (different classifications)

- Supplemental total interest received

- Link to interest-bearing assets growth

Operating classification can inflate OCF when comparing to investing-classification peers.

Q · 01What is Interest Received Cfo?+