Accrued Interest Receivable Balance Sheet Asset Guide

Accrued Interest Receivable is interest earned on loans, bonds, or deposits but not yet collected. Learn how to accrue and record it on the balance sheet.

Overview

Accrued Interest Receivable is interest earned on loans, bonds, or deposits but not yet collected. Learn how to accrue and record it on the balance sheet.

Accrued Interest Receivable is the amount of interest income that a company has earned on its interest-bearing assets (such as loans, notes receivable, bonds, or deposits) as of the balance sheet date, but has not yet received in cash or been billed to the debtor. It reflects the time-based accrual of interest revenue under the matching principle, ensuring income is recognized in the period it is earned.

What It Represents

Accrued Interest Receivable captures interest that has accumulated since the last payment date but hasn't been collected yet.

It's the flip side of 'Interest Payable'—here the company is the lender or investor earning the interest.

Accrual ensures interest income matches the period the funds were lent/invested.

Typical Sources

- Interest on customer loans or notes receivable

- Interest on held-to-maturity or other debt securities

- Interest on bank deposits or money market accounts

- Interest on employee or related party loans

- Interest on finance leases receivable

Common in banks, finance companies, and any firm with significant lending or investing activity.

"It does not matter how frequently something succeeds if failure is too costly to bear."

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

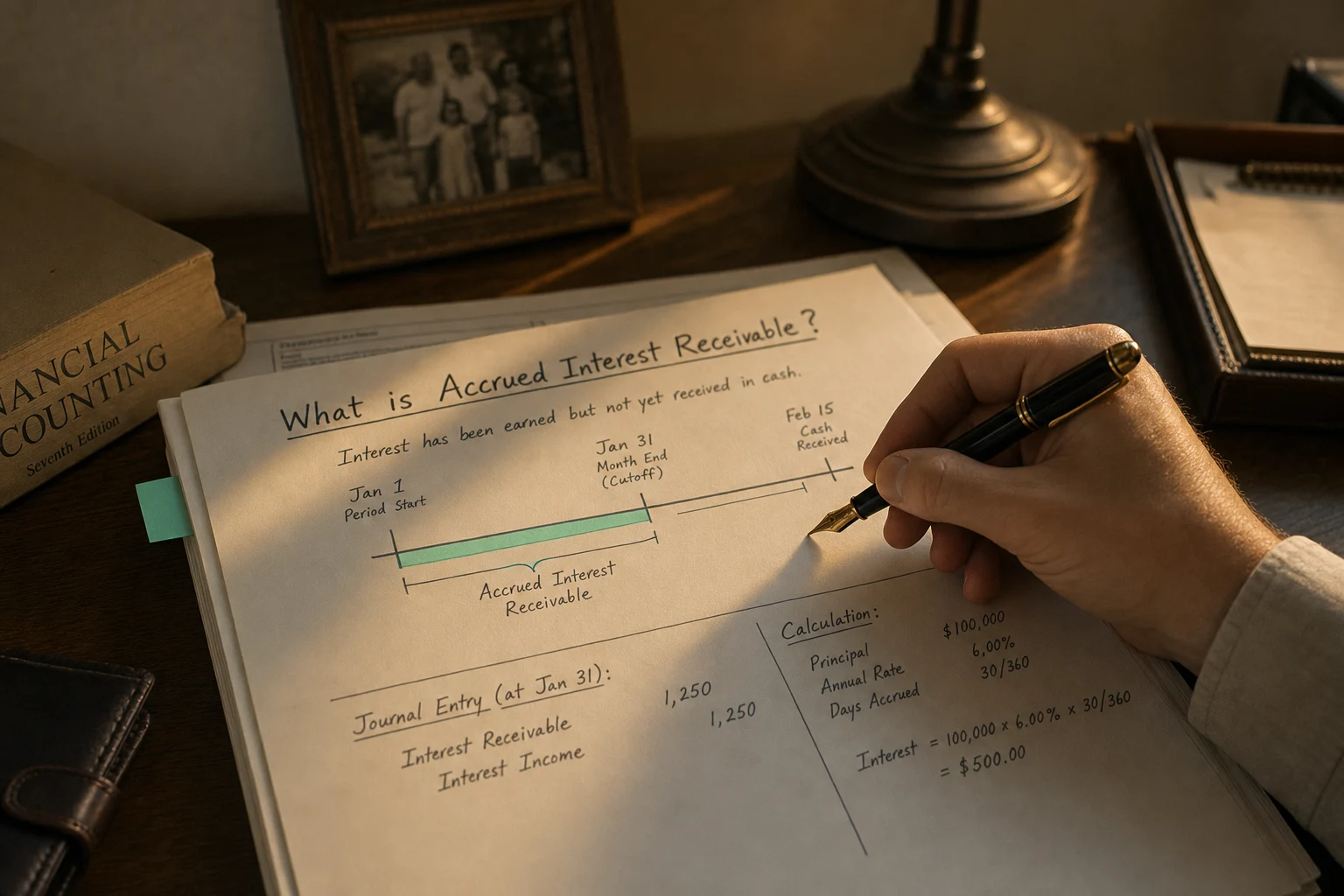

A Simple Example

Company holds a $1 million bond paying 6% interest semi-annually (payments June 30 and December 31).

- Balance sheet date September 30

- 3 months interest earned: 1M × 6% × 3/12)

- Record 15,000 Interest Income

- December 31: Receive 15k accrual + accrue new $15k

Books always show the interest earned to date.

Accounting Treatment

- Periodic accrual: Debit Accrued Interest Receivable, Credit Interest Income

- On receipt: Debit Cash, Credit Accrued Interest Receivable

- Effective interest method for discounted/premium instruments

- Classify current/non-current by expected receipt timing

Almost always current due to frequent interest payment cycles.

Balance Sheet Presentation

Under current assets as:

- 'Accrued Interest Receivable'

- 'Interest Receivable'

- 'Accrued Interest'

- Often grouped in 'Other Receivables' or 'Prepaid and Other Current Assets'

Impairment assessed if collection doubtful.

Analytical Implications

- Size reflects scale of lending/investing activity

- Growth signals increasing interest-earning assets

- Timing indicator (resets at payment dates)

- Contribution to interest income

- Liquidity bridge (cash coming soon)

Persistently high balances may indicate delayed collections or long payment cycles.