Notes Receivable is a financial concept covered in this article. Formal Promissory Notes Owed to the Company

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

Notes Receivable are formal written promises (promissory notes) from customers or other parties to pay a definite sum of money, usually with interest, on a specific date or on demand. They arise from sales of goods/services on extended credit, loans to employees or affiliates, or financing arrangements, and are distinguished from ordinary accounts receivable by their formal documentation and often longer terms.

What Makes a Note Receivable

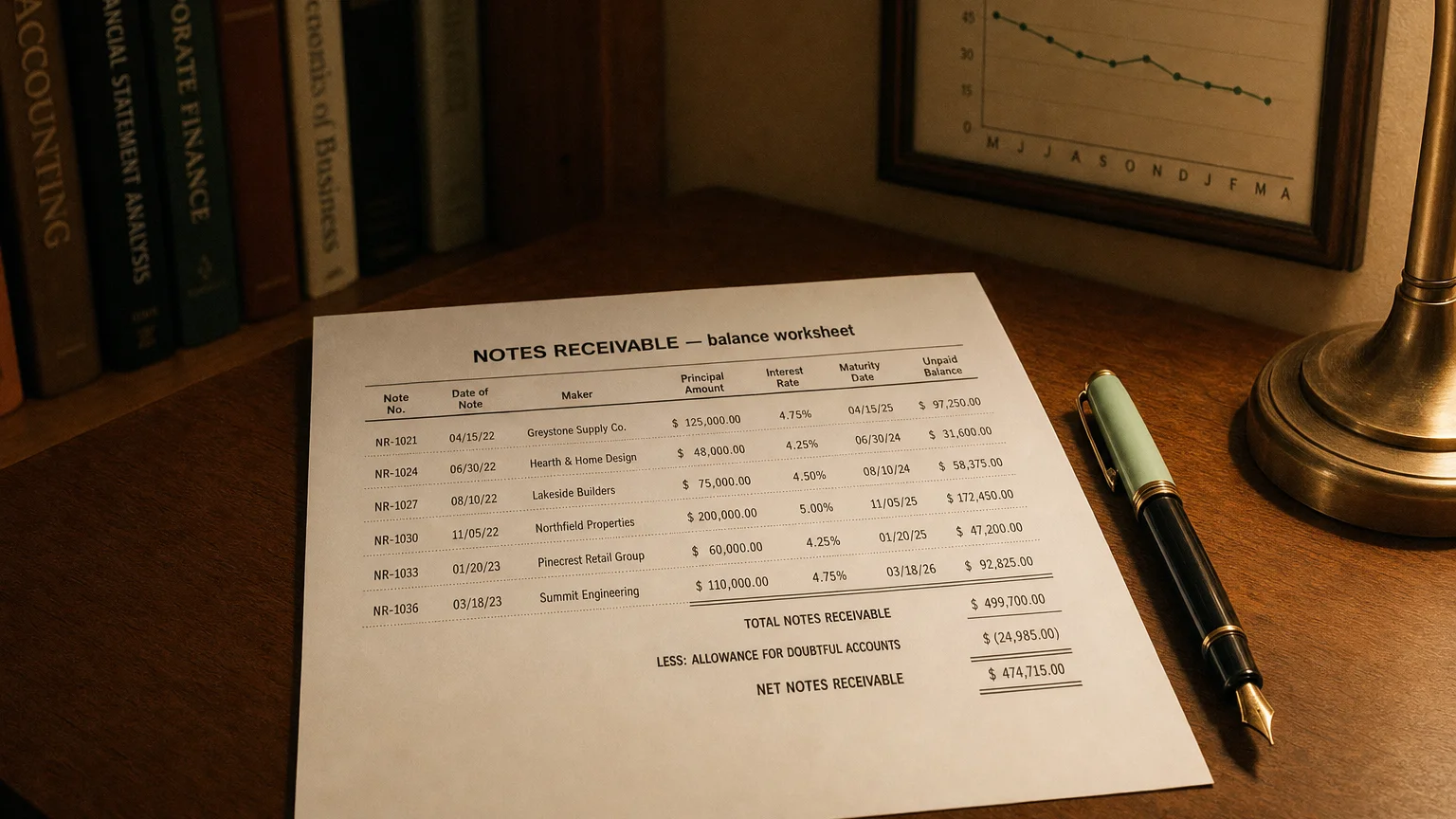

Notes Receivable are documented IOUs with specific terms: principal amount, interest rate, maturity date, and repayment schedule.

They provide stronger legal standing than open accounts receivable and are common when credit terms exceed normal trade periods.

Zero-interest or below-market notes require discounting to present value.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (1934)

Typical Situations

- Selling high-value goods with installment payments (machinery, vehicles)

- Converting slow-paying accounts receivable into formal notes

- Loans to employees (relocation, retention bonuses)

- Financing sales to customers with poor credit

- Intercompany or related party lending

- Seller-financed real estate transactions

Capital equipment manufacturers and auto dealers frequently use notes for customer financing.

Accounting Treatment

- Initial recording at fair value (face + imputed interest if needed)

- Interest income accrued over term (effective interest method)

- Classify current/non-current based on maturity schedule

- Allowance for credit losses applied

- Discount/premium amortized to interest income

Example: 100k principal, accrue interest annually.

Current portion (due within year) reclassified from non-current.

Balance Sheet Presentation

Under current or non-current assets as:

- ‘Notes Receivable’

- ‘Notes Receivable - Current/Non Current’

- Net of allowance and unamortized discount

- Often grouped in broader ‘Receivables’

Footnotes disclose terms, interest rates, maturity dates, and collateral.

Comparison with Accounts Receivable

Notes Receivable

- Formal written promise

- Usually interest-bearing

- Longer terms, structured repayment

Accounts Receivable

- Open invoice

- Short-term, non-interest

- Normal trade credit

Analytical Implications

- Customer financing strategy (boost sales but tie up capital)

- Interest income contribution

- Credit and collection risk (longer terms = higher uncertainty)

- Liquidity impact (slower cash conversion)

- Related party notes (governance scrutiny)

Significant growth may indicate aggressive sales tactics or weaker customers.

Q · 01What is Notes Receivable?+