is a financial concept covered in this article. Long-Term Promissory Notes Owed to the Company

It does not matter how frequently something succeeds if failure is too costly to bear.

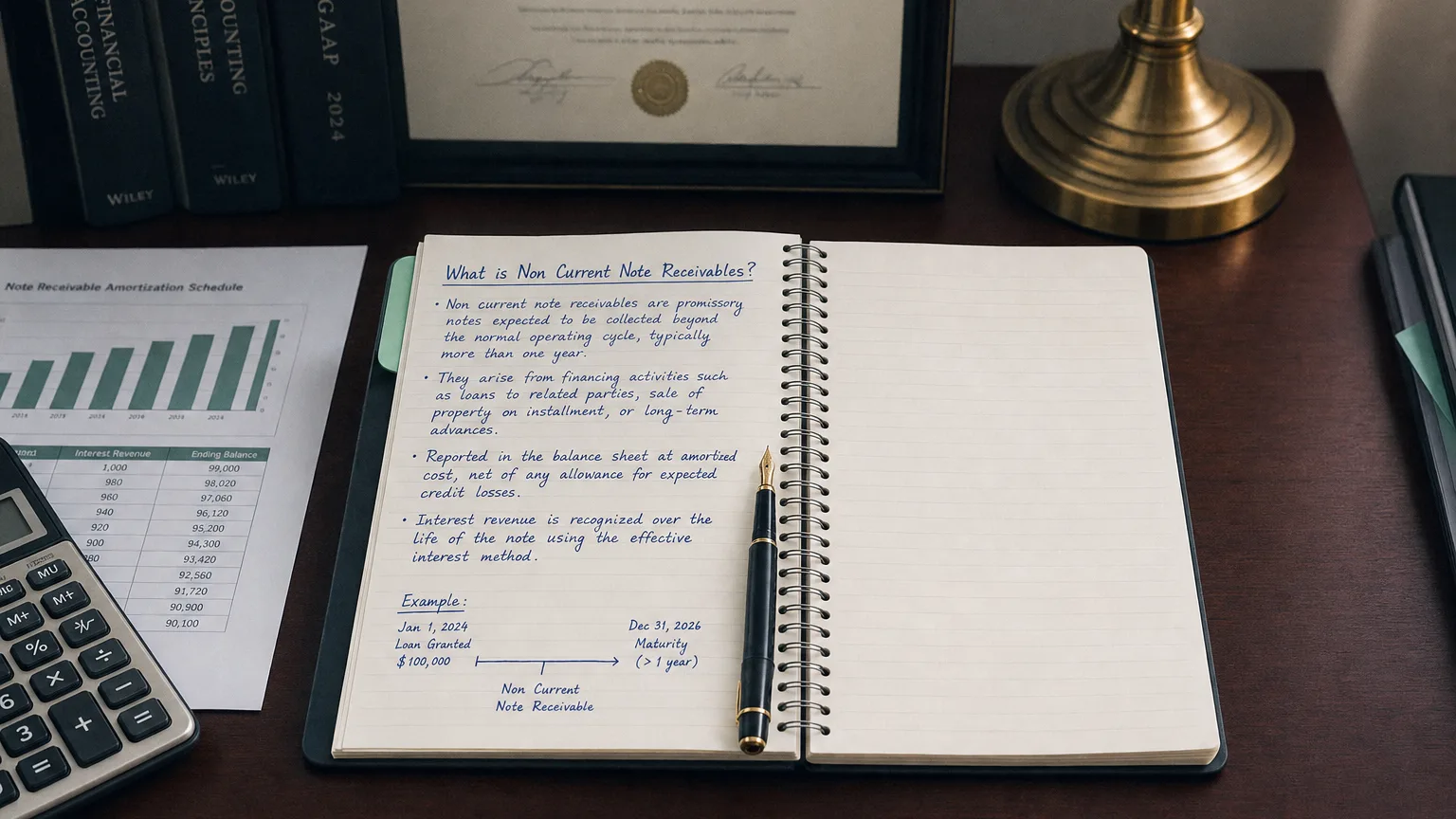

Non Current Note Receivables are formal promises (promissory notes) from customers, employees, or other parties to pay a specific amount, usually with interest, where the due date is more than 12 months (or one operating cycle) from the balance sheet date. They represent long-term lending or financing provided by the company, often from sales on credit terms or separate loan arrangements.

What They Are

Non Current Note Receivables are written promises to pay that extend beyond one year. The ‘note’ part means there’s a formal document spelling out principal, interest rate, repayment schedule, and maturity date.

They’re different from regular accounts receivable (open invoice, short-term, no interest) because notes usually carry interest and have longer terms.

The non-current label simply means the bulk of payment is due after one year.

Typical Situations Where They Appear

- Selling expensive equipment on installment plans (e.g., machinery maker finances buyer over 5 years)

- Real estate or property sales with seller financing

- Employee relocation or retention loans repayable over several years

- Loans to related parties or affiliates with long terms

- Restructuring short-term receivables into longer notes

You’ll see bigger balances in capital goods, real estate, or companies offering customer financing as a sales tool.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

How They’re Recorded

- Initial recognition at fair value (cash advanced or sales price)

- If interest below market → discount and amortize (effective interest method)

- Interest income recognized over term

- Classify current/non-current based on payment schedule

- Allowance for doubtful notes if collection risk

Example: Sell 20k down and 80k non-current note receivable (minus any discount).

Balance Sheet Presentation

Under non-current assets as:

- ‘Non Current Note Receivables’

- ‘Long-Term Notes Receivable’

- ‘Notes Receivable - Non Current’

- Net of allowance and discount

Current portion (due within year) shown separately in current assets.

Comparison with Other Receivables

Non Current Note Receivables

- Formal note, interest-bearing, long-term

Accounts Receivable

- Trade invoices, short-term, usually no interest

Loans Receivable

- Broader category, may include notes

What to Look For

- Customer financing strategy (competitive edge?)

- Interest income contribution

- Credit risk (allowance size)

- Liquidity impact (long collection cycle)

- Related party notes (disclosure scrutiny)

Large balances can tie up capital and increase default risk.