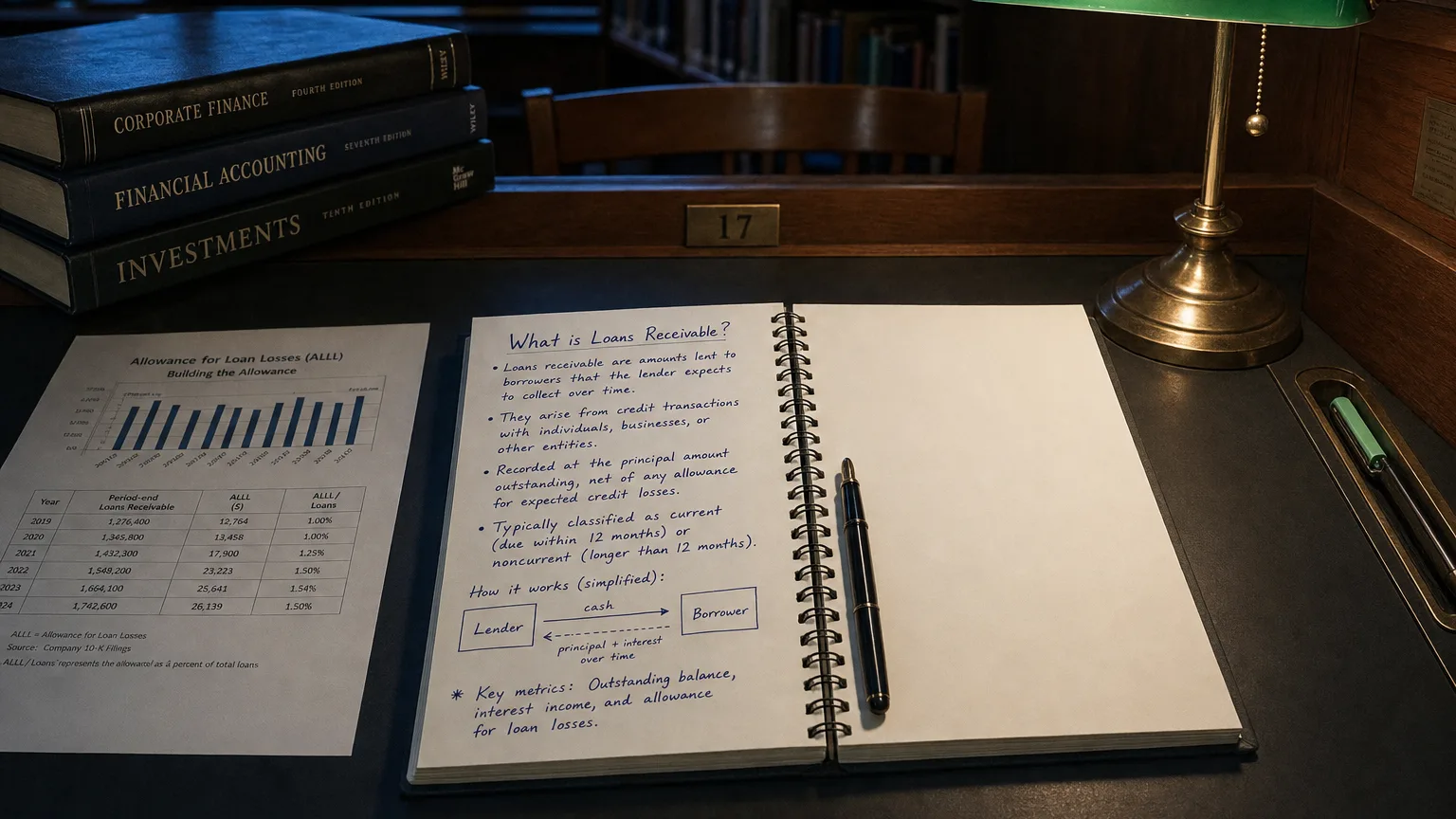

Loans Receivable is a financial concept covered in this article. Amounts Lent to Borrowers Expected to Be Repaid with Interest

It does not matter how frequently something succeeds if failure is too costly to bear.

Loans Receivable represent amounts a company has lent to customers, employees, affiliates, or third parties under formal or informal loan agreements, with an expectation of repayment of principal plus interest (or imputed interest) over time. These are financial assets arising from direct lending activities or financing sales, classified as current or non-current based on repayment schedule.

What Loans Receivable Include

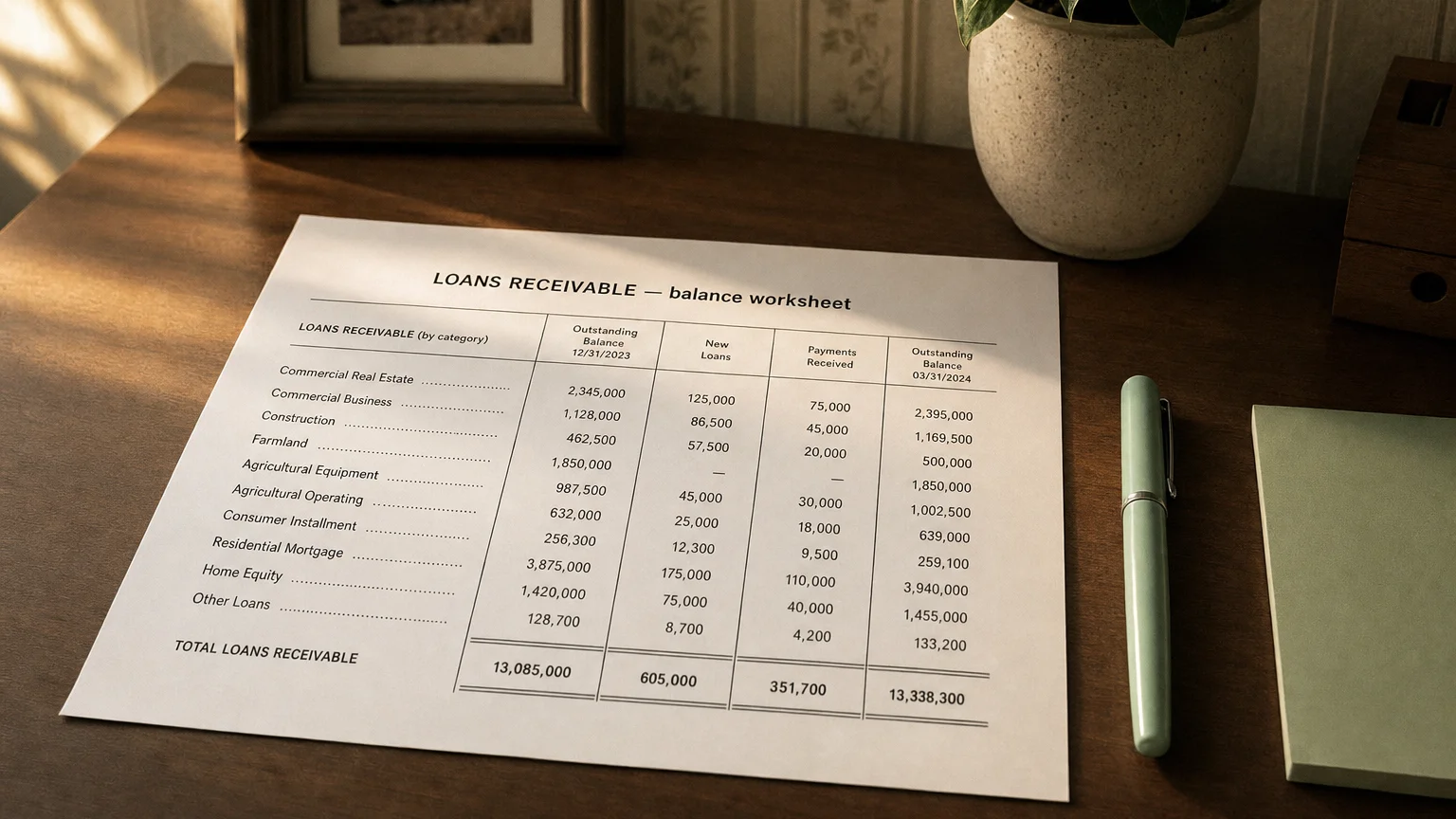

Loans Receivable cover a broad range of lending:

- Customer financing loans (e.g., auto, equipment, mortgage-style)

- Consumer installment loans

- Commercial loans to businesses

- Employee loans (relocation, advances)

- Loans to related parties or affiliates

- Mortgage loans held for investment

Often evidenced by promissory notes, but broader than just ‘notes receivable’.

Banks and finance companies have this as a core asset; non-financial firms from customer financing programs.

A Typical Example

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

A heavy equipment manufacturer sells a 800k over 5 years at 7% interest.

- Record 800k Loans Receivable

- Over 5 years: collect monthly payments, recognize interest income

- Classify portion due within year as current, rest non-current

- Build allowance for expected defaults

This boosts sales but ties up capital and adds credit risk.

Accounting Treatment

- Initial measurement at fair value (principal + fees - discounts)

- Subsequent: Amortized cost using effective interest method

- Interest income recognized over term

- Impairment via allowance (CECL/IFRS 9 expected loss model)

- Split current/non-current by repayment schedule

Below-market loans require interest imputation (discount to PV).

Balance Sheet Presentation

Under assets as:

- ‘Loans Receivable’

- ‘Loans and Advances’

- ‘Finance Receivables’

- Net of unearned income, allowance for credit losses

- Current and non-current portions separate

Footnotes detail aging, delinquency, allowance methodology.

Why Companies Extend Loans

- Drive sales (customer financing removes price barrier)

- Earn interest margin

- Build customer loyalty

- Competitive differentiation

- Core business for finance subsidiaries

Analytical Implications

- Interest income quality (recurring vs. one-time)

- Credit risk exposure (allowance adequacy)

- Liquidity (long collection cycle)

- Growth driver (financed sales inflate revenue)

- Economic sensitivity (defaults rise in downturns)

Rapid growth in loans receivable can signal aggressive sales or weakening credit standards.

Q · 01What is Loans Receivable?+