is a financial concept covered in this article. Short-Term Amounts Owed to the Company by Related Entities or Individuals

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

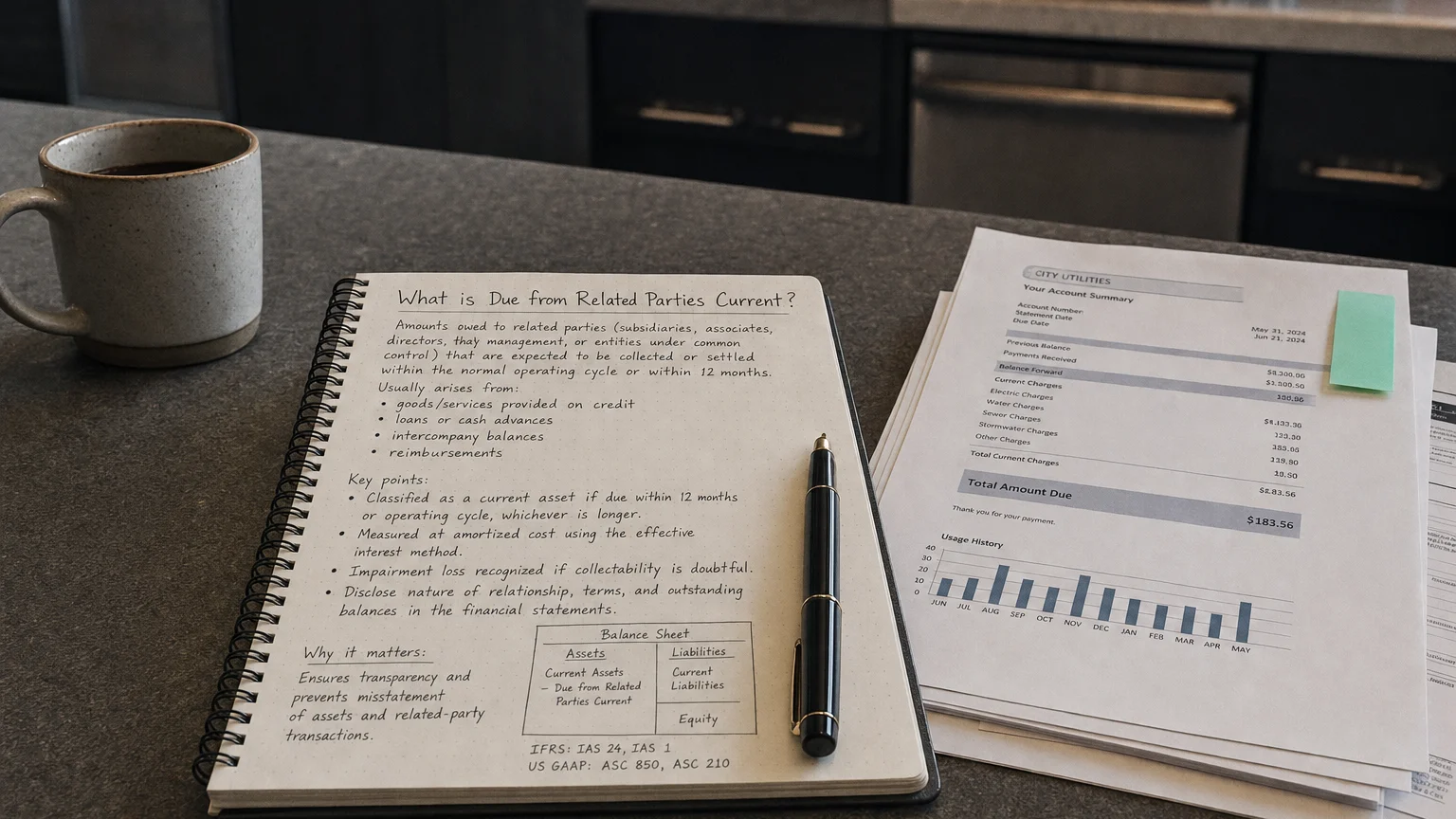

Due from Related Parties Current are amounts owed to the company by related parties—parents, subsidiaries, affiliates, joint ventures, key executives, or major shareholders—that are expected to be settled within 12 months or the operating cycle. These short-term receivables often come from intercompany transactions, loans, or operational support, and sit as current assets on the balance sheet.

What These Balances Represent

Think of Due from Related Parties Current as money the company has lent or advanced to its own corporate family or key insiders, with repayment expected soon.

The ‘current’ part means cash should come back within a year—making it part of working capital.

It’s the mirror image of ‘Due to Related Parties’—here the company is the lender.

Typical Situations You See This

- Parent loans cash to a subsidiary for short-term needs

- Central treasury advances funds to operating units

- Company sells goods/services to affiliate on credit

- Reimbursement due from joint venture partners

- Short-term advances to executives (relocation, travel)

- Cash pooling sweeps leaving temporary receivables

Very common in large groups with centralized finance or in private/family businesses.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

A Quick Example

ParentCo has a centralized cash pool. Subsidiary needs $5 million for inventory this quarter.

- Parent transfers 5M

- Subsidiary records ‘Due to Related Parties Current’ $5M

- Three months later subsidiary repays from sales cash → both balances zero out

Efficient internal funding, often cheaper than bank loans.

Accounting Rules

- Record at amortized cost (if loan)

- Impute interest if rate below market (except some intragroup under IFRS)

- Classify current if repayment within 12 months

- Assess impairment risk

- Full disclosure: who, how much, terms, interest

Rules force transparency because these deals aren’t always arm’s-length.

Where It Shows Up

Under current assets as:

- ‘Due from Related Parties Current’

- ‘Current Receivables from Related Parties’

- ‘Intercompany Receivables - Current’

- Sometimes in ‘Other Receivables’

Footnotes name the parties, explain terms, and show movements.

Why These Exist

- Fast, low-cost internal funding

- Central cash management efficiency

- Support struggling units without external debt

- Tax or currency optimization

- Operational integration in groups

What to Watch For

- Interest income (or lack—subsidized?)

- Repayment reliability (subordinate to external lenders?)

- Growth signaling heavier internal reliance

- Impairment if related party struggles

- Governance red flags (loans to executives)

Big or persistent balances can mean the company is propping up weaker parts of the group.