The Allowance for Doubtful Accounts Receivable is a contra-asset that reduces gross accounts receivable to the amount realistically expected to be collected, matching estimated credit losses to the period of the related sales.

In the short run, the market is a voting machine. In the long run, it is a weighing machine.

Allowance for Doubtful Accounts Receivable (also called Bad Debt Allowance or Provision for Doubtful Accounts) is a contra-asset account that reduces gross accounts receivable to reflect the portion management expects will never be collected. It represents a prudent estimate of credit losses from customers who won’t or can’t pay their invoices, ensuring the net receivables on the balance sheet are stated at a realistic collectible amount.

Why the Allowance Exists

When you sell on credit, some customers inevitably won’t pay—bankruptcy, disputes, or just slow payment turning bad. You can’t wait forever to recognize this reality.

The allowance lets you estimate and reserve for these losses upfront, matching the bad debt expense to the same period as the related sales revenue.

Without it, receivables would be overstated and profits inflated until actual write-offs hit.

A Straightforward Example

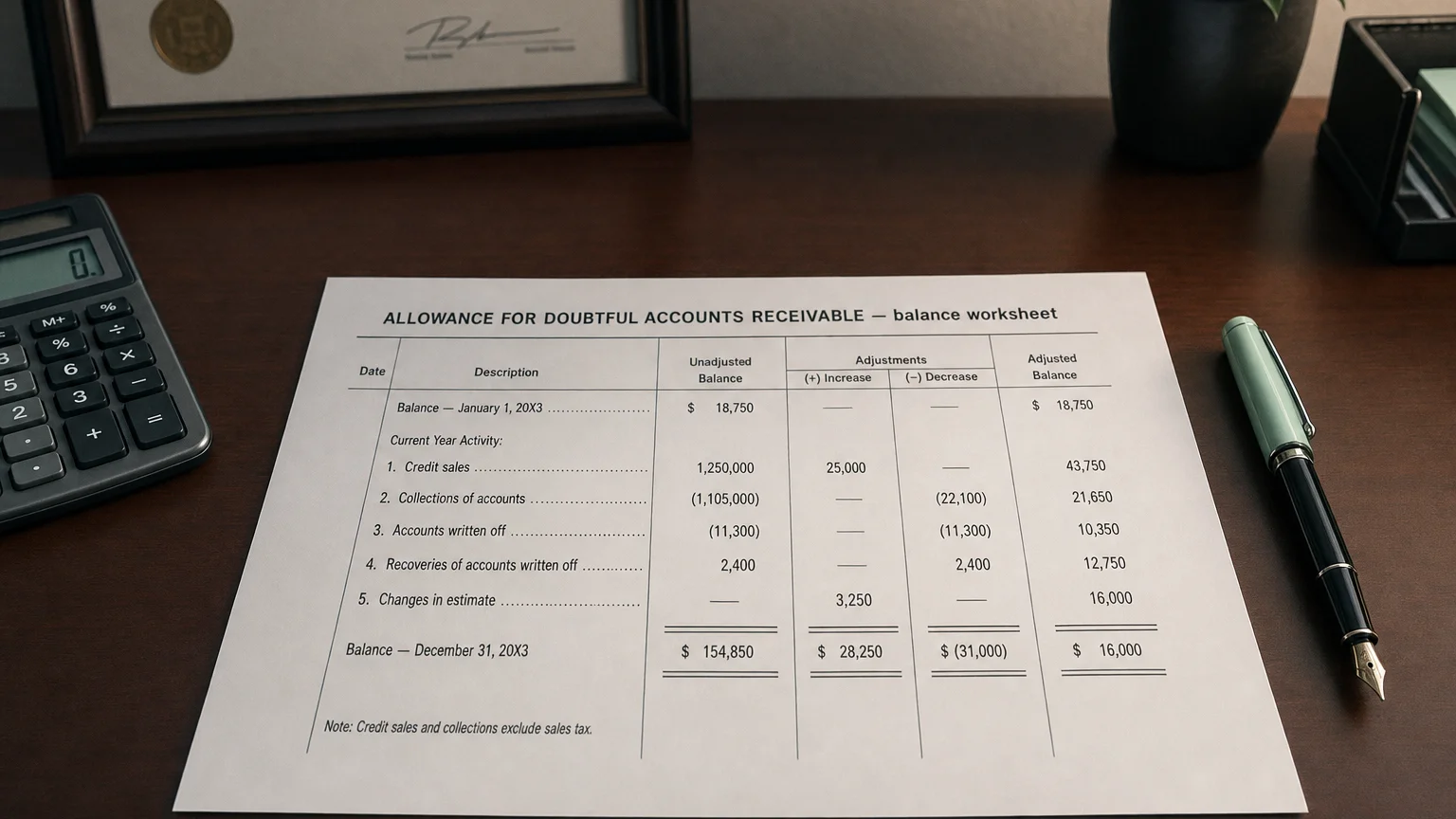

Your company has $1 million in gross accounts receivable at year-end.

- Based on history and aging, you estimate 5% ($50,000) will be uncollectible

- You record $50,000 Allowance for Doubtful Accounts

- Balance sheet shows: Gross AR 50k = Net AR $950k

- Income statement: $50k Bad Debt Expense reduces profit

Next year a 20k each. Net AR unchanged, no new expense.

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

Common Estimation Methods

- Percentage of Sales: Apply historical bad debt % to credit sales (income statement approach)

- Aging of Receivables: Higher % for older invoices (balance sheet approach)

- Risk-Based/Specific: Identify troubled customers individually

- Expected Credit Loss (CECL/IFRS 9): Forward-looking model including macro factors

Most companies blend aging with percentage for accuracy.

Accounting Entries

- Annual estimate: Debit Bad Debt Expense, Credit Allowance

- Actual write-off: Debit Allowance, Credit Gross AR

- Recovery of written-off: Reverse write-off then record cash

Write-offs don’t hit expense—they use the existing allowance.

Balance Sheet Presentation

Typically shown as:

- Deduction directly below Gross AR

- ‘Accounts Receivable, net of allowance of $X’

- Or separate contra-asset line

Footnotes detail method, aging schedule, and movement rollforward.

What to Watch For

- Allowance % of gross AR (too low = aggressive, too high = cookie jar)

- Trend vs. historical loss rates

- Aging quality (more in 90+ days = risk)

- Write-offs vs. allowance (under/over provisioned?)

- Macro impact (recessions spike losses)

Sudden allowance release can artificially boost earnings.

Q · 01How is the allowance for doubtful accounts estimated?+

Q · 02What happens when a bad debt is written off?+

Q · 03Why do analysts flag a falling allowance-to-receivables ratio?+