is a financial concept covered in this article. Contra-Asset Accounts Reducing Receivables to Net Realizable Value

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

Receivables Adjustments Allowances is a collective term for contra-asset accounts that reduce gross receivables to their estimated net realizable value. These allowances cover expected credit losses (doubtful accounts), sales returns, discounts, and other adjustments. They ensure the balance sheet reflects a realistic amount the company expects to collect from customers.

What These Allowances Cover

Companies rarely collect 100% of what customers owe. These contra-accounts adjust for expected shortfalls:

- Allowance for Doubtful Accounts / Credit Losses — customers who won’t pay

- Allowance for Sales Returns — products customers send back

- Allowance for Sales Discounts — early-payment or volume discounts

- Other adjustments — pricing disputes, billing errors

All reduce gross receivables to the amount management realistically expects in cash.

Net Receivables = Gross Receivables − Total Adjustments/Allowances.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (1934)

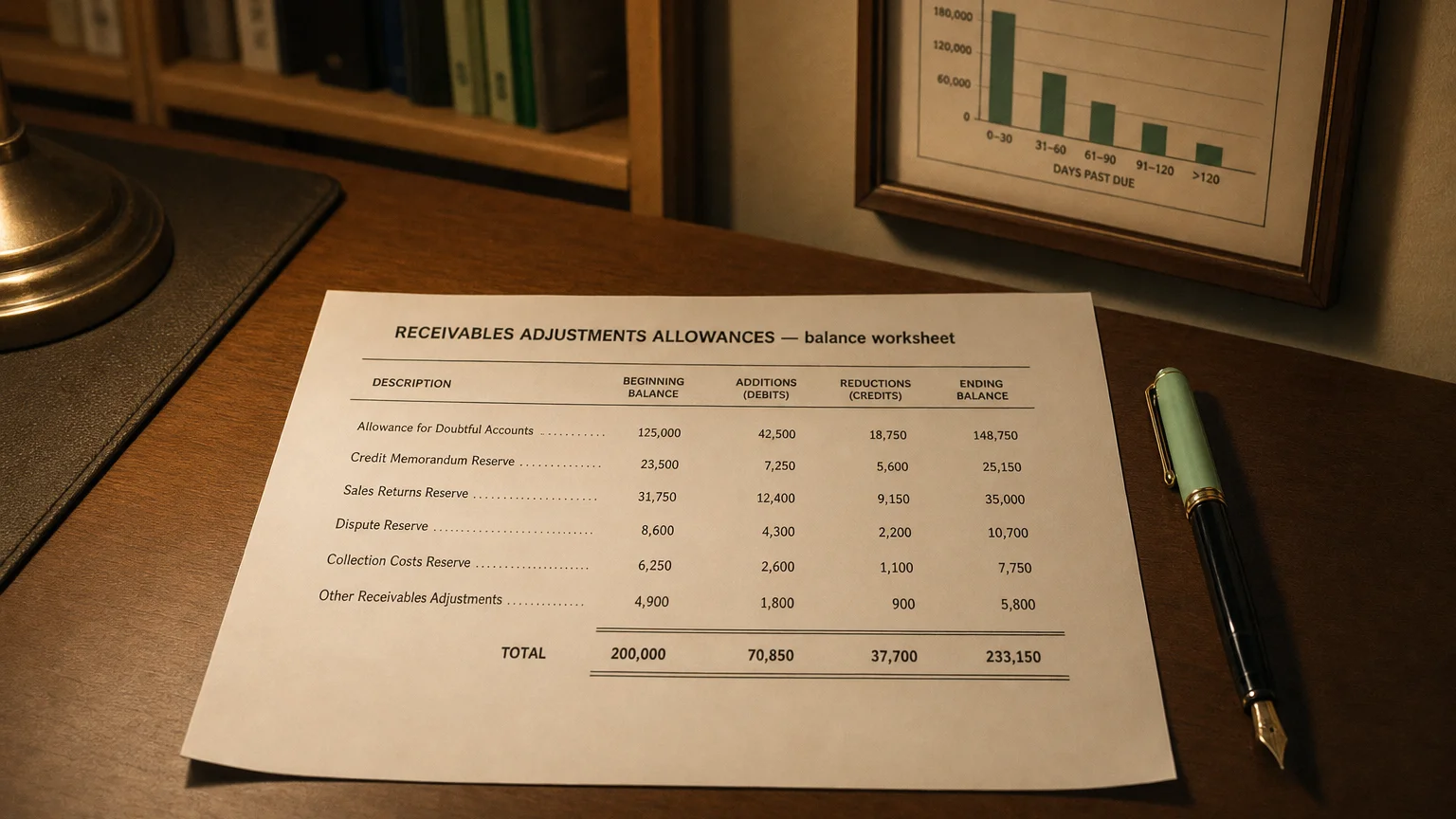

A Clear Example

Year-end gross accounts receivable: $10 million.

- Estimated uncollectible (bad debt): $300k

- Expected returns (historical 2%): $200k

- Volume/early payment discounts likely taken: $100k

Total Adjustments/Allowances = 9.4 million. The $600k hits various expense lines (bad debt, returns, discounts).

How Allowances Are Built

- Bad Debt/Credit Losses: Aging method, % of sales, or expected loss models (CECL/IFRS 9)

- Returns: Historical return rate applied to recent sales

- Discounts: Expected take-rate on offered terms

- Periodic review and adjustment to reflect current conditions

Actual write-offs or returns reduce both gross receivables and the allowance—no new expense.

Balance Sheet Presentation

Typically shown as:

- Deduction below gross receivables

- ‘Accounts Receivable, net of allowances of $X’

- Separate lines for major allowances

- Or grouped as ‘Receivables Adjustments Allowances’

Footnotes detail each allowance, method, and rollforward (beginning, additions, utilizations, ending).

Why Management Cares

- Conservative balance sheet (avoid overstating assets)

- Accurate profit matching (expense when sale recorded)

- Cash flow forecasting (net = expected collections)

- Compliance with GAAP/IFRS

What to Watch For

- Allowance % trend vs. historical (too low = aggressive revenue)

- Sudden releases boosting earnings (cookie-jar reserves?)

- Rising allowances signaling credit deterioration

- Industry comparison (retail higher returns, B2B lower)

- Aging schedule quality

Under-provisioning inflates assets and future write-offs hurt.

Q · 01What is Receivables Adjustments Allowances?+