Non Current Accounts Receivable is a financial concept covered in this article. Trade Receivables Due Beyond One Year

The stock market is a device for transferring money from the impatient to the patient.

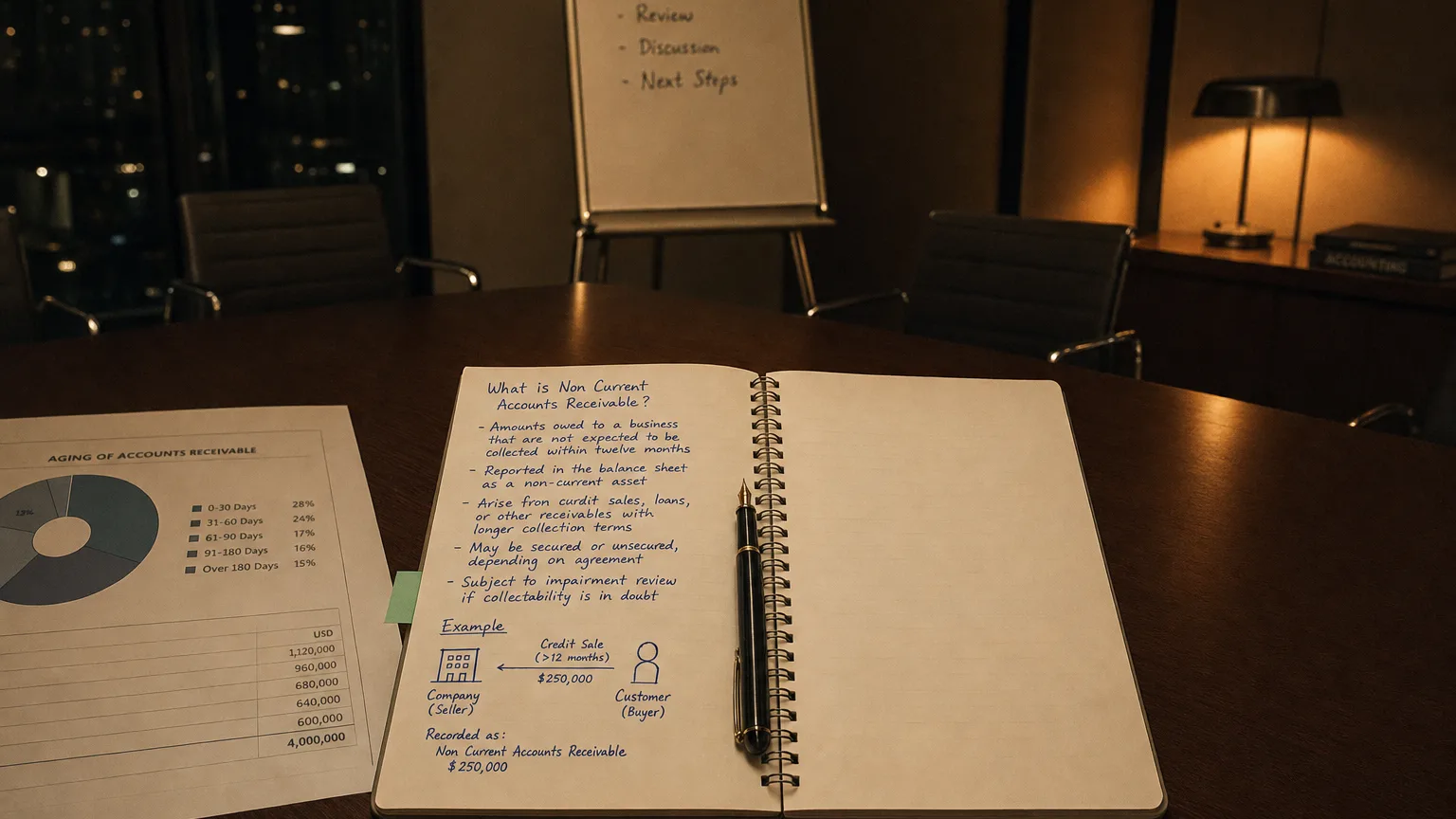

Non Current Accounts Receivable are amounts owed to the company by customers for goods or services already delivered, where payment is contractually due more than 12 months (or one operating cycle) after the balance sheet date. These long-term trade receivables are separated from regular (current) accounts receivable to reflect their extended collection timeline.

What They Represent

Non Current Accounts Receivable arise when a company sells goods or services on credit terms that stretch beyond one year. The customer has a contractual obligation to pay, but the timeline is long.

They are still ‘trade’ receivables (from normal business) but classified non-current due to maturity, unlike typical 30-90 day invoices.

Distinguished from notes receivable (formal promissory notes, often interest-bearing).

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Annual Report (1999)

Typical Scenarios

- Long-term construction or project contracts with progress billing over years

- Sale of high-value equipment with extended payment plans

- Real estate sales with seller-financed installments

- Government or large corporate contracts with deferred payment schedules

- Service agreements spanning multiple years

Heavy machinery makers or engineering firms often show meaningful non-current AR from multi-year delivery and payment cycles.

Accounting Treatment

- Initial recognition at transaction price (fair value of goods/services)

- If significant financing component → discount to present value (impute interest)

- Interest income unwound over term

- Classify current/non-current based on expected collection timing

- Allowance for expected credit losses applied

IFRS 15/US GAAP ASC 606 require assessing financing component for contracts >1 year.

Balance Sheet Presentation

Under non-current assets as:

- ‘Non Current Accounts Receivable’

- ‘Long-Term Trade Receivables’

- ‘Accounts Receivable - Non Current’

- Net of allowance and any discount

Current portion (due within year) shown in current assets.

Comparison with Notes Receivable

Non Current Accounts Receivable

- Open account/invoice-based

- Usually no formal note

- Often non-interest-bearing

Non Current Note Receivables

- Formal promissory note

- Typically interest-bearing

- Structured repayment

Analytical Considerations

- Customer financing strategy (competitive tool?)

- Liquidity impact (cash tied up long-term)

- Credit risk (longer horizon = higher uncertainty)

- Interest income potential (if discounted)

- Working capital cycle extension

Large non-current AR can strain cash flow and increase bad debt exposure.