“Available-for-sale (AFS) securities are investments held at fair value on the balance sheet. Unrealized gains and losses bypass the income statement, accumulating in Other Comprehensive Income (OCI) and shielding reported earnings from short-term market price movements.”

You can't take the same actions as everyone else and expect to outperform.

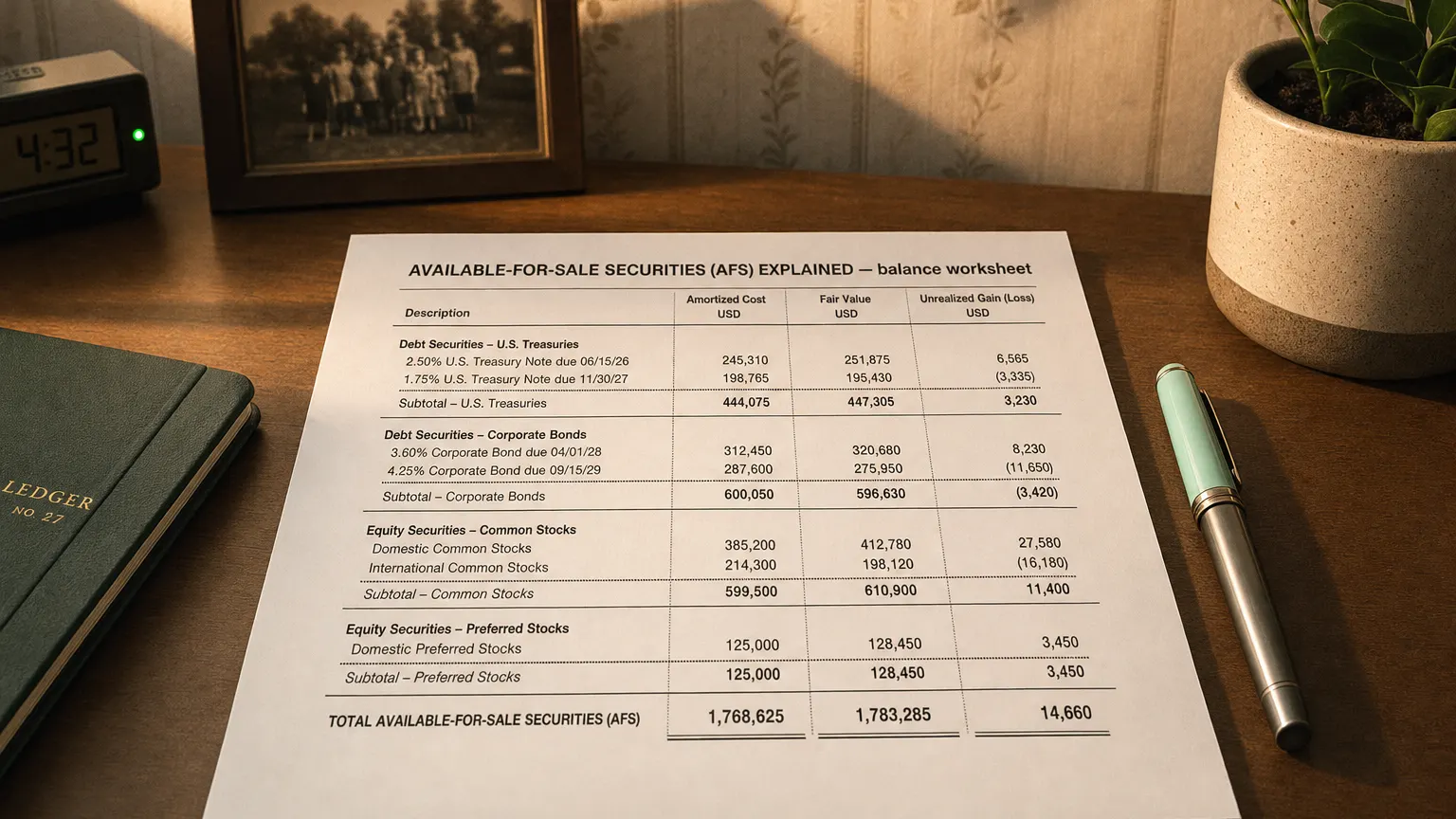

Available-for-sale (AFS) securities are investments (typically in debt or equity instruments) that a company intends to hold for an indefinite period rather than trade actively or hold to maturity. In accounting classification, AFS is essentially a “default” category for investments not qualifying as Trading or Held-to-Maturity. These securities are reported at fair value on the balance sheet, with any unrealized gains or losses (changes in market value before sale) recorded in the shareholders’ equity section as part of other comprehensive income (OCI) instead of in current earnings. This approach insulates net income from temporary market fluctuations.

The AFS ‘Middle-Ground’ Approach

The AFS classification provides a middle ground between the two other main investment categories under U.S. GAAP:

- Compared to Trading Securities: Trading securities are also reported at fair value, but all their unrealized gains and losses flow directly to the income statement, creating earnings volatility. AFS insulates the income statement from these fluctuations.

- Compared to Held-to-Maturity (HTM) Securities: HTM securities (debt only) are reported at amortized cost, ignoring market value changes entirely. AFS provides a more current valuation by using fair value on the balance sheet, but without the earnings impact of the Trading category.

Treatment under U.S. GAAP vs. IFRS

The concept of AFS has evolved differently under the two major accounting frameworks.

U.S. GAAP

Historically, AFS applied to both debt and equity securities. However, a 2016 update (ASC 321) now requires most equity investments to be measured at fair value through net income. This means that today, the AFS category under U.S. GAAP applies almost exclusively to debt securities. When an AFS debt security is sold, the cumulative gain or loss stored in OCI is ‘recycled’ into the income statement as a realized gain or loss.

IFRS (International Standards)

IFRS 9, which replaced the older IAS 39 standard, eliminated the AFS category. It was replaced by a new classification model. The closest equivalent is Fair Value through Other Comprehensive Income (FVOCI). While similar, a key difference exists for equity investments: under the IFRS FVOCI election, gains and losses are never recycled to the income statement upon sale; they remain permanently in equity.

“You can’t take the same actions as everyone else and expect to outperform.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘Dare to Be Great’ (2006)

Balance Sheet Presentation

AFS securities are listed as assets on the balance sheet at their current fair market value. The corresponding unrealized gains or losses are reflected in the shareholders’ equity section.

The Role of Accumulated Other Comprehensive Income (AOCI)

The unrealized gains and losses on AFS securities do not affect Retained Earnings. Instead, they are accumulated in a separate component of equity called Accumulated Other Comprehensive Income (AOCI). This transparently shows the impact of market fluctuations on the company’s net worth without distorting its reported net income for the period.

Common Examples of AFS Securities

Given the current rules, the most common examples of AFS securities under U.S. GAAP are debt instruments. This includes:

- Government Bonds: U.S. Treasury bonds and municipal bonds that a company plans to hold but may sell before maturity.

- Corporate Bonds: Debt issued by other corporations.

- Mortgage-Backed Securities: Many banks and financial institutions hold large portfolios of these securities and classify them as AFS to manage liquidity and interest rate risk while insulating earnings from short-term price swings.

Under older GAAP or IFRS rules, minority equity stakes in other companies were also common examples of AFS securities.

Q · 01“How do AFS securities differ from trading securities?”+

Q · 02“What happens to AFS gains and losses when a security is sold?”+