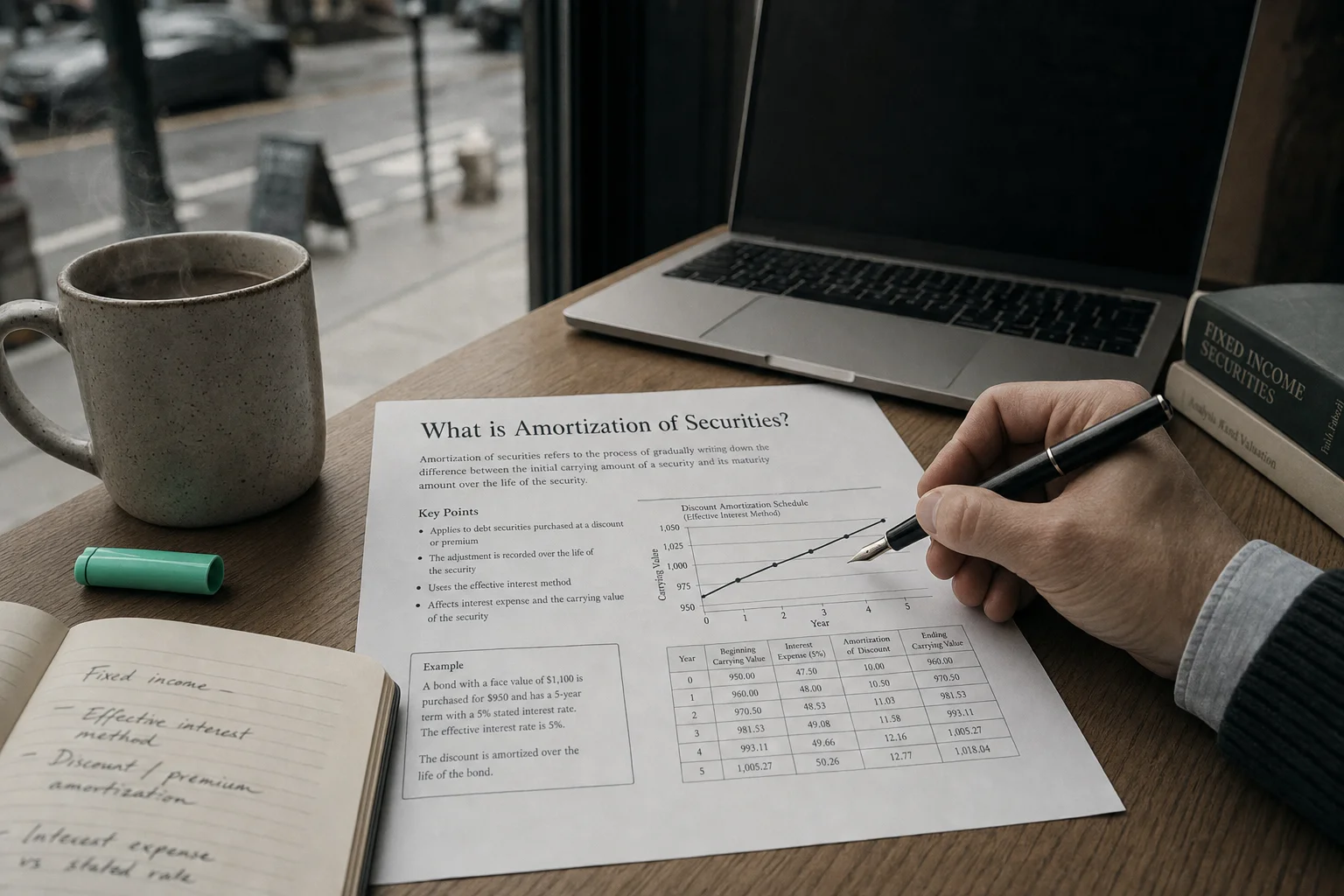

Amortization of securities adjusts a bond's carrying value from purchase price to face value via the effective interest method, matching reported income to true yield over the bond's life.

From the standpoint of an institution, the existence of a risk manager has less to do with actual risk reduction than it has to do with the impression of risk reduction.

Amortization of Securities is the non-cash process of gradually adjusting the carrying value of debt securities (bonds or notes) purchased at a premium (above face value) or discount (below face value) toward their face value over time until maturity. This amortization is recognized as an adjustment to interest income, aligning the effective yield with the actual cash interest received.

Why Amortization Happens

When you buy a bond at a price different from its face value, the yield you actually earn (effective yield) differs from the coupon rate.

Amortization spreads that premium or discount over the bond’s life so the reported interest income matches the true economic yield.

Without it, interest income would be distorted—too high for premium bonds, too low for discounts.

A Clear Example

You buy a 1,100 (premium).

- Cash interest: $50/year

- But you paid extra $100 → true yield <5%

- Each year: Amortize part of $100 premium

- Reduce carrying value toward $1,000

- Reported interest income = $50 cash − amortization

Discount bond ($900 purchase): Amortization adds to cash interest, boosting reported income.

By maturity, carrying value = face, total income = effective yield.

“From the standpoint of an institution, the existence of a risk manager has less to do with actual risk reduction than it has to do with the impression of risk reduction.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

The Effective Interest Method

Standard way (required):

- Calculate yield to maturity at purchase

- Apply constant yield to carrying value each period

- Interest income = Yield × Carrying value

- Amortization = Interest income − Cash coupon

Straight-line allowed only if immaterial difference.

Where It Shows Up

- Income statement: Adjustment to ‘Interest Income’

- Cash flow (indirect): Non-cash item in operating (premium reduces OCF add-back)

- Balance sheet: Reduces/increases carrying value of securities

- Footnote: Amortization schedule for material holdings

Which Securities Get Amortized

- Held-to-Maturity: Always (amortized cost)

- Available-for-Sale debt: Amortized cost basis, unrealized to OCI

- Trading/FVTPL: No amortization—full fair value through P&L

Equity securities: No amortization (no maturity).

What to Watch For

- Premium bonds → lower reported yield over time

- Discount bonds → higher reported yield

- Large portfolios → material income impact

- Rate environment (falling rates → more premium purchases)

- Cash vs. accrual interest difference

Amortization of premium reduces operating cash flow add-back.

Q · 01How does premium amortization affect interest income?+

Q · 02What is the effective interest method for securities?+

Q · 03Which securities require amortization under US GAAP?+

Q · 04How does bond amortization appear on the cash flow statement?+

Q · 05What distinguishes premium from discount amortization?+