Amortization of intangibles is a non-cash expense that spreads the acquisition cost of finite-life assets—patents, customer relationships, licenses—over their estimated useful lives, reducing reported earnings without consuming cash.

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

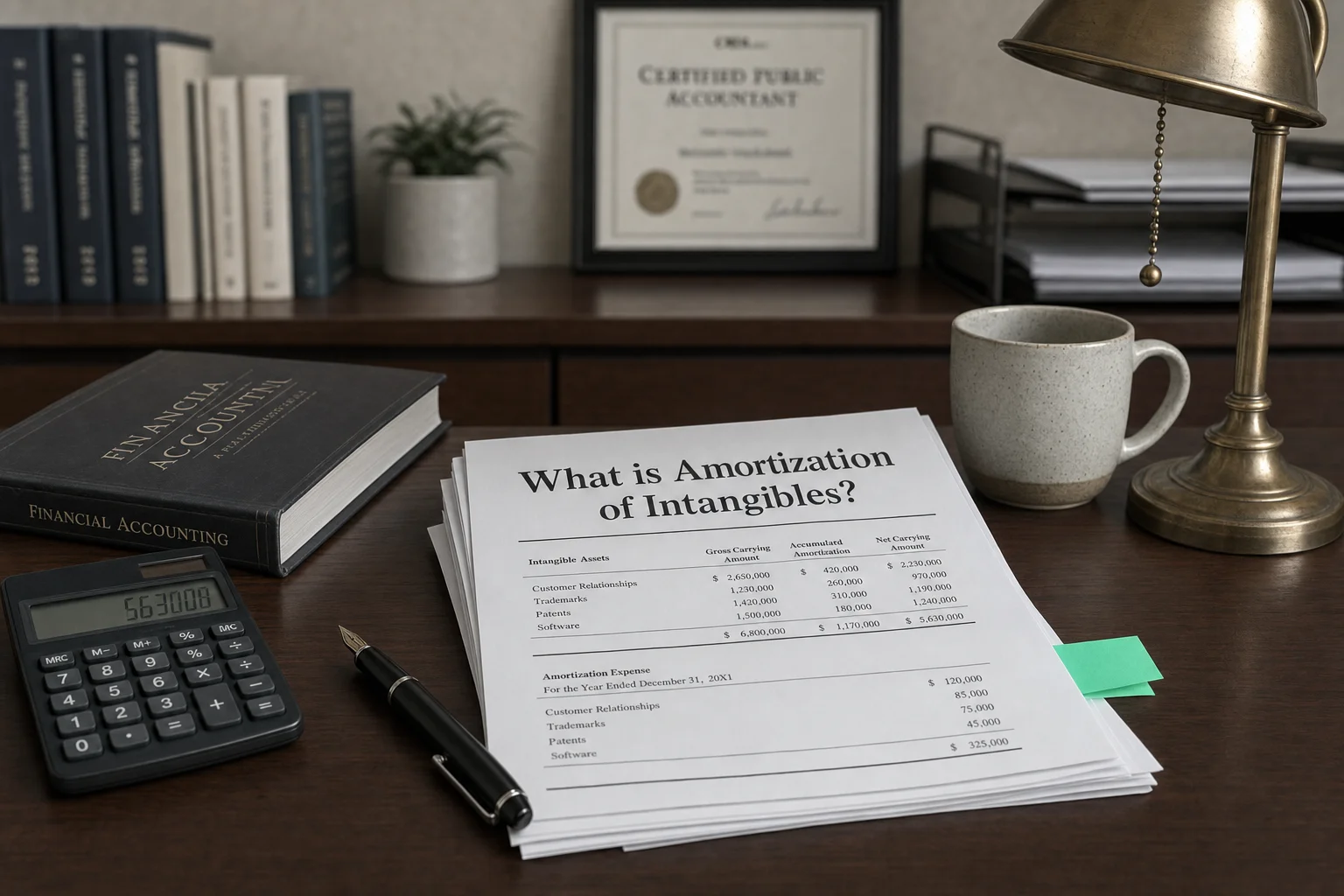

Amortization of Intangibles is the systematic, non-cash expense that allocates the cost of finite-life intangible assets—such as patents, customer relationships, acquired software, or licenses—over their estimated useful lives. It’s the intangible equivalent of depreciation for physical assets, reducing reported profit but preserving cash, and added back in operating cash flow.

Why We Amortize Intangibles

You pay big money for an acquired patent or customer list because it will drive revenue for years. Expensing it all upfront would crush earnings in the purchase year and overstate them later.

Amortization spreads the cost smoothly over the asset’s useful life, matching the expense to the periods that actually benefit.

The cash went out at acquisition—this is just accounting allocation.

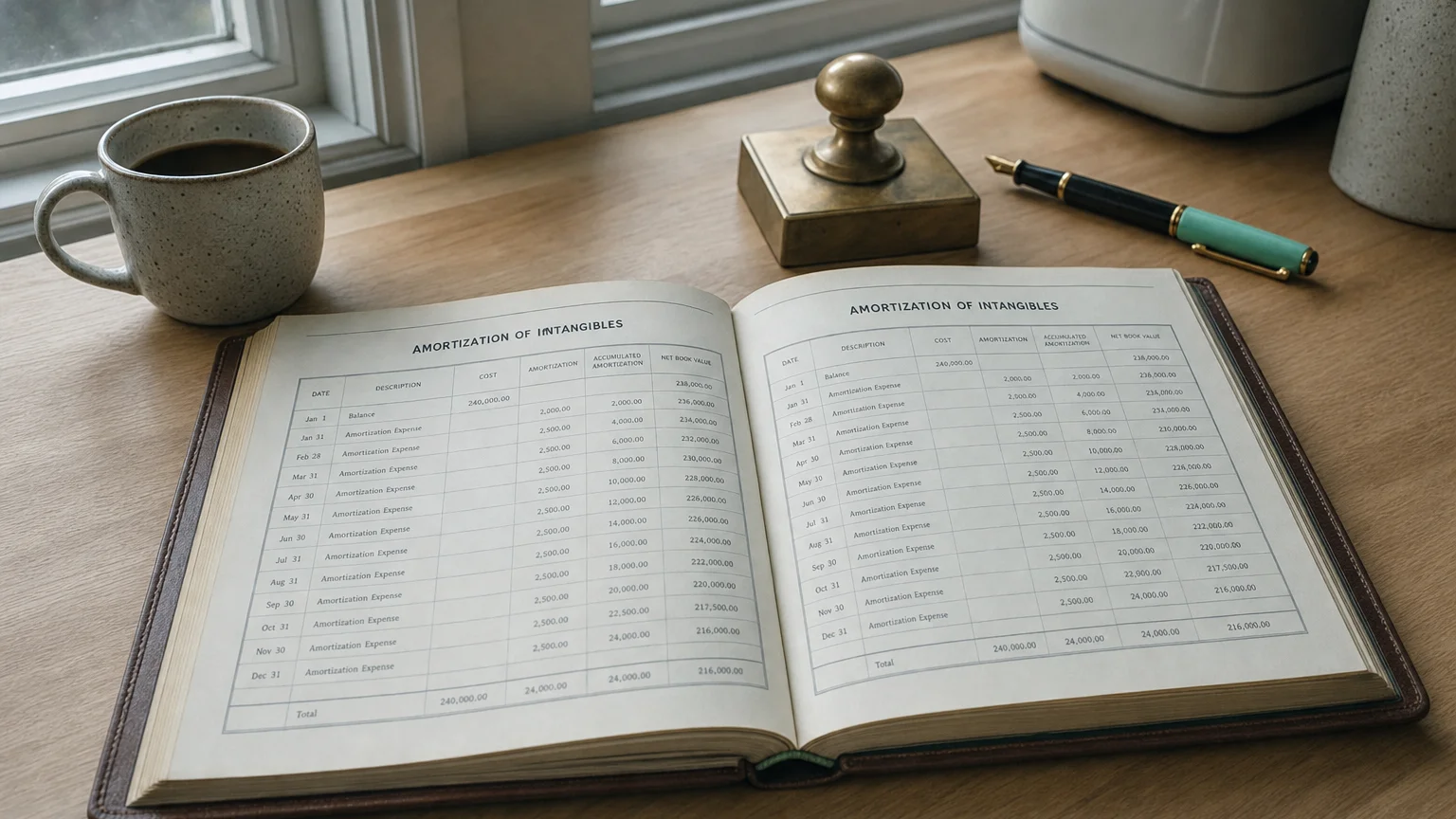

A Real Example to See It in Action

PharmaCo buys a smaller drug company for $1 billion.

- $400M allocated to an approved drug patent (10-year remaining life)

- Annual amortization: $40M expense

- Cash flow: +$40M add-back each year (non-cash)

- After 10 years: Patent fully amortized, book value zero

Earnings take a steady $40M hit annually, reflecting the patent’s declining value as it nears expiry.

“When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

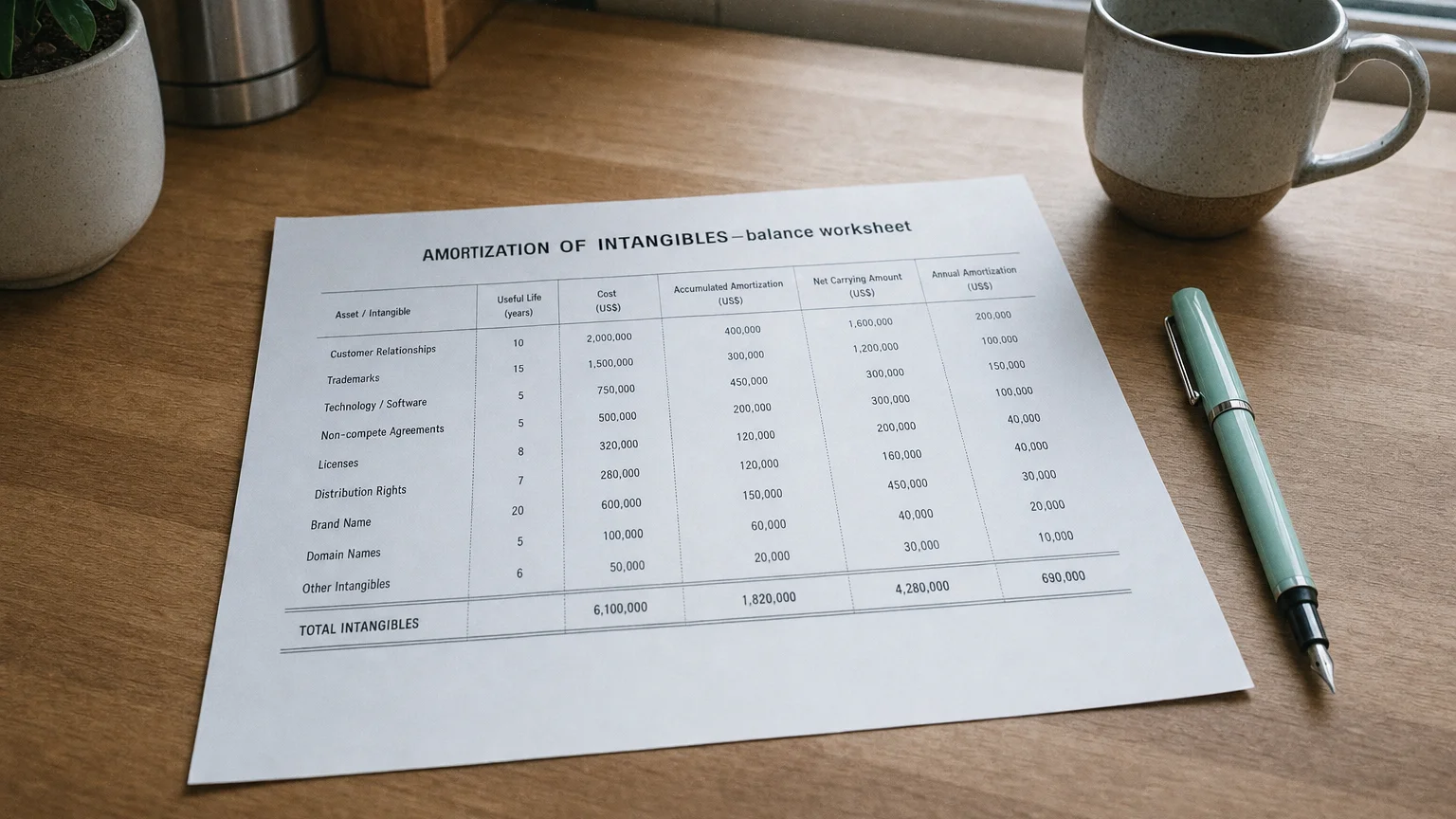

What Gets Amortized

- Acquired patents and technology

- Customer contracts and relationships

- Trademarks with finite life

- Capitalized software (acquired or certain internal)

- Licenses and franchises

- Non-compete agreements

- Favorable contracts

Goodwill and indefinite-life brands (like Coca-Cola trademark): no amortization—impairment test only.

How It’s Calculated

- Cost basis from acquisition allocation

- Estimate useful life (economic or legal life, shorter)

- Usually straight-line (even spread)

- Pattern matching consumption if better (rare)

- Residual value typically zero

Life reassessed if circumstances change.

Where It Appears

- Income statement: Operating expenses or COGS

- Cash flow: Non-cash add-back in operating activities

- Balance sheet: Reduces Other Intangible Assets

- Often grouped in ‘Depreciation & Amortization’

Footnotes detail major classes and remaining lives.

What a Rising Trend Signals

- Heavy recent acquisitions (more intangibles to amortize)

- Peak M&A period hitting earnings

- Future amortization drag (ongoing expense)

- Cash flow benefit (large add-back)

- Potential impairment risk if assets underperform

Sharp jump often follows big deals—check acquisition footnotes.

Q · 01Is amortization of intangibles a cash expense?+

Q · 02Which intangible assets are not amortized?+

Q · 03What method do companies use to amortize intangibles?+