Amortization Cash Flow Non-Cash Add-Back Explained

Amortization cash flow is the non-cash expense added back to net income on the cash flow statement. Learn why it boosts OCF and what analysts watch.

Overview

Amortization cash flow is the non-cash expense added back to net income on the cash flow statement. Learn why it boosts OCF and what analysts watch.

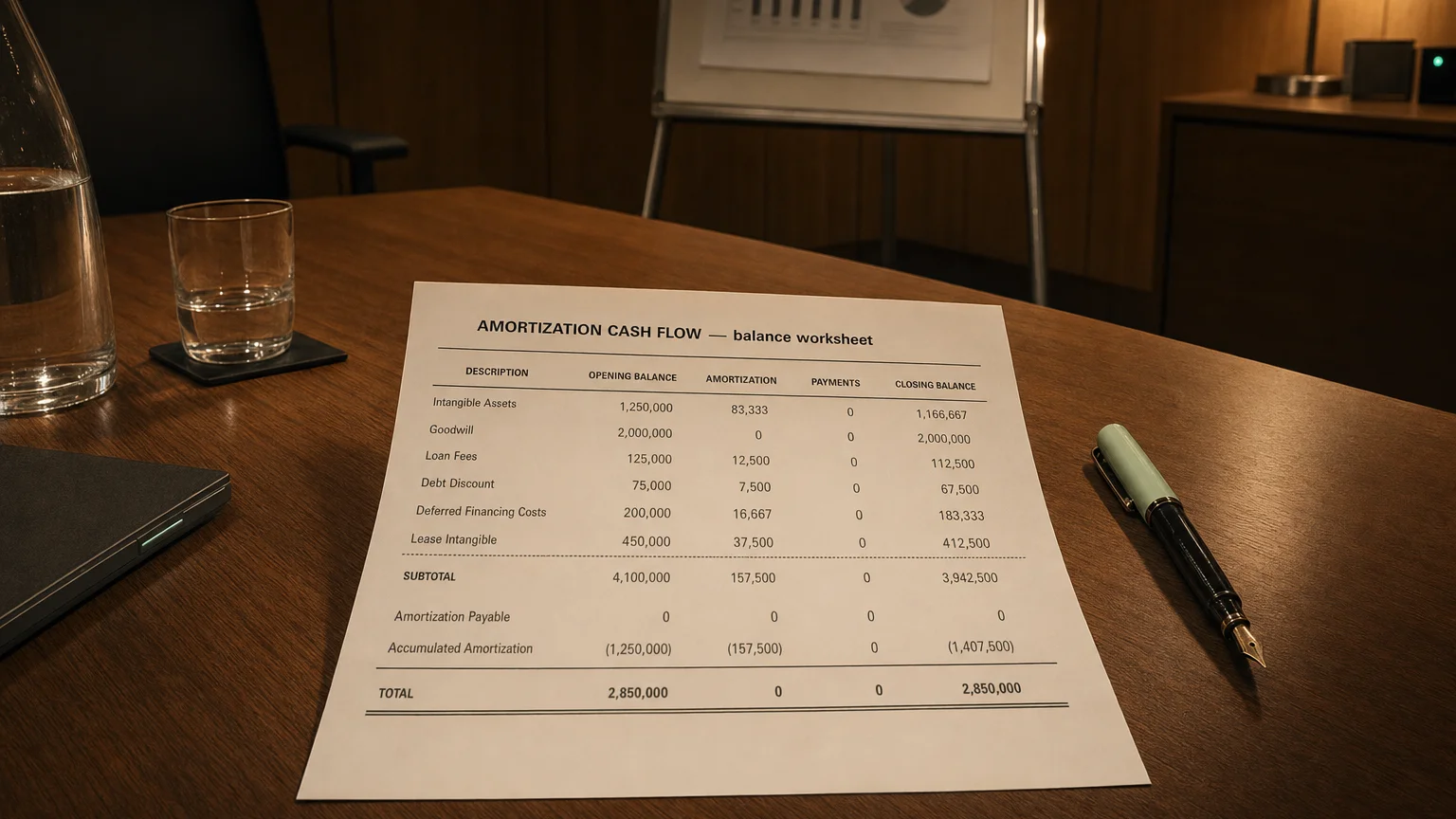

Amortization Cash Flow refers to the non-cash amortization expense added back in the operating activities section of the cash flow statement. It represents the systematic allocation of the cost of finite-life intangible assets (like patents, software, customer lists, or acquired contracts) over their useful lives. Even though it reduces reported profit, no cash actually leaves the company—making it a key add-back when converting net income to operating cash flow.

Why Amortization Is Non-Cash

When a company buys or creates an intangible asset with a limited life, the cost is capitalized on the balance sheet—not expensed immediately.

Amortization spreads that cost over the years the asset provides value, just like depreciation does for physical assets.

The cash was spent upfront (at acquisition)—future amortization is just an accounting entry moving cost from asset to expense.

That's why it's added back: profit is lower, but cash isn't affected this period.

A Simple Example

TechCo buys a patent for $50 million (5-year life).

- Year 1 cash: -$50M (investing outflow at purchase)

- Years 1-5: $10M annual amortization expense

- Each year cash flow: +$10M add-back (non-cash)

- Net income down $10M, but cash unchanged by amortization

The real cash hit was in year 1; later years just allocate the cost.

"Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray."

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman's Letter 2014 (2014)

Common Intangibles Amortized

- Acquired patents and technology

- Customer relationships and contracts

- Trademarks with finite life

- Capitalized software development

- Licenses and franchises

- Non-compete agreements

Goodwill and indefinite-life trademarks: no amortization (impairment test only).

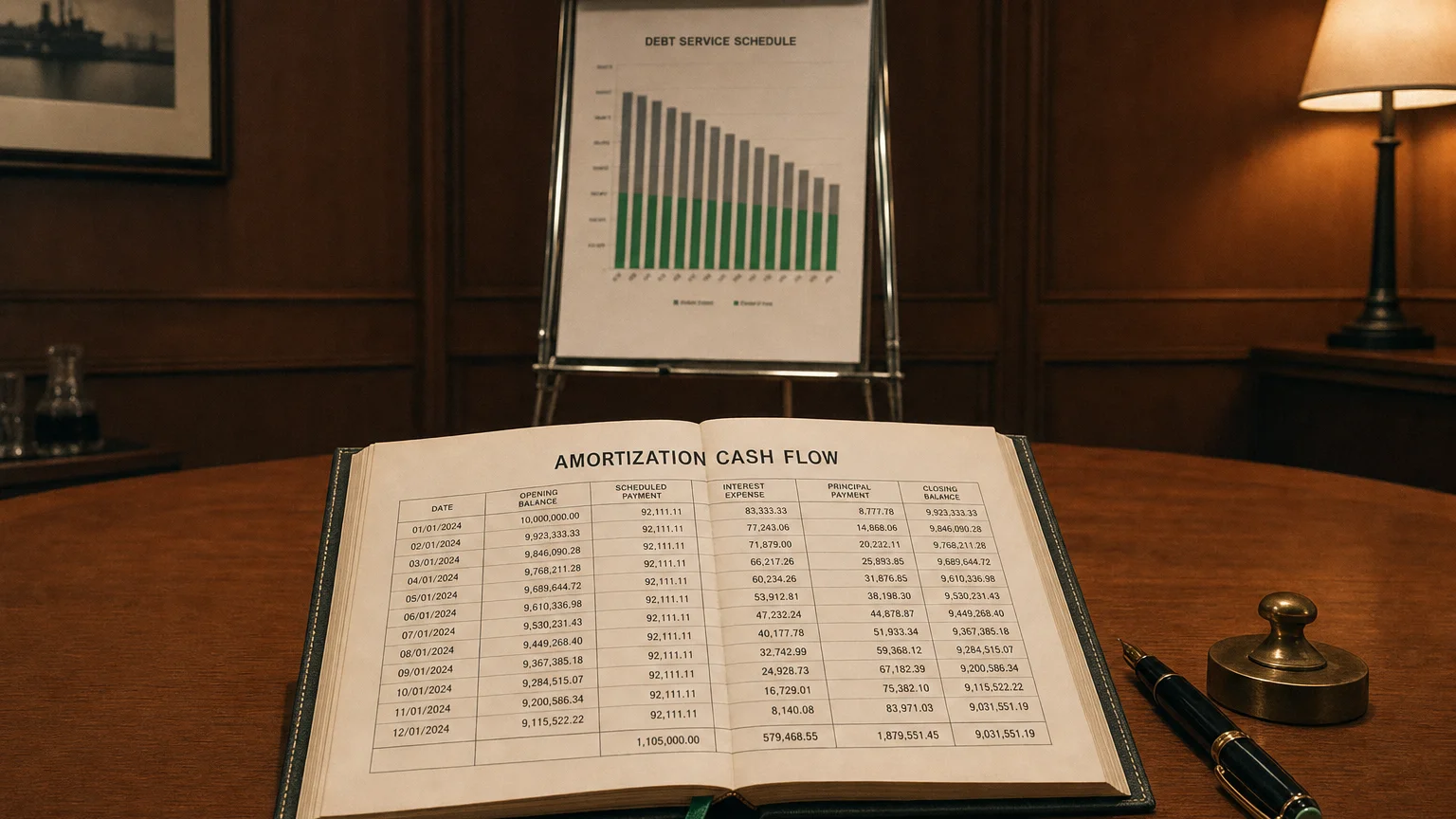

Where It Shows Up

Cash flow statement (operating, indirect method):

- Amortization (or in Depreciation & Amortization line)

- Part of 'Depreciation, Amortization, and Depletion'

Balance sheet: Reduces Other Intangible Assets.

Why Companies Have Amortization

- Match cost of acquired intangibles to revenue generated

- Reflect finite useful life of IP or relationships

- Acquisition accounting (most intangibles from M&A)

- Capitalized internal development (limited cases, e.g., software)

What to Watch For

- Trend (rising = more acquisitions?)

- Size vs. revenue (M&A heavy companies higher)

- Future drag (amortization continues years after purchase)

- Add-back magnitude (boosts OCF)

- Comparison to capex (intangible vs. tangible investment)

High amortization can mask underlying cash earnings power.