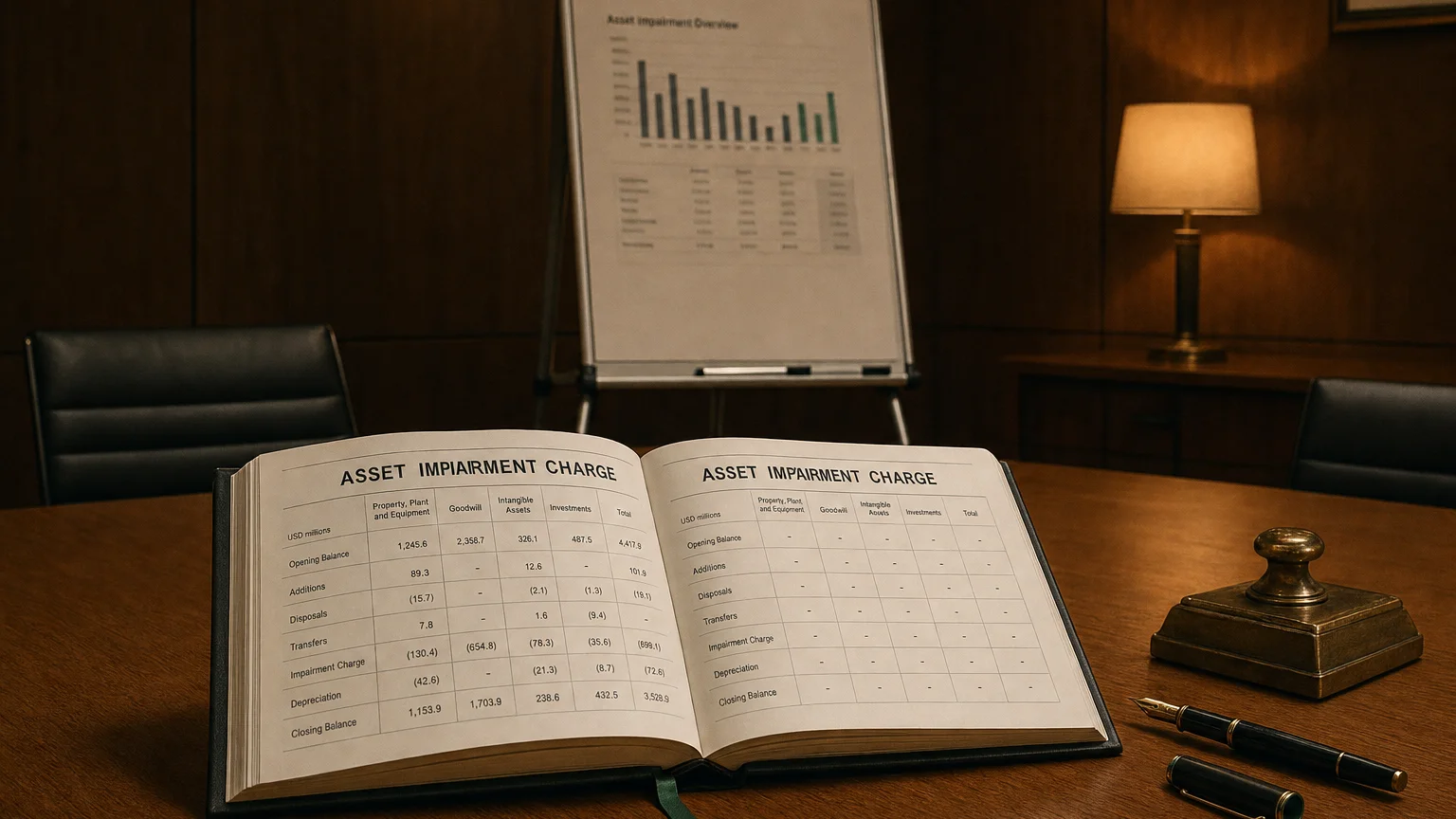

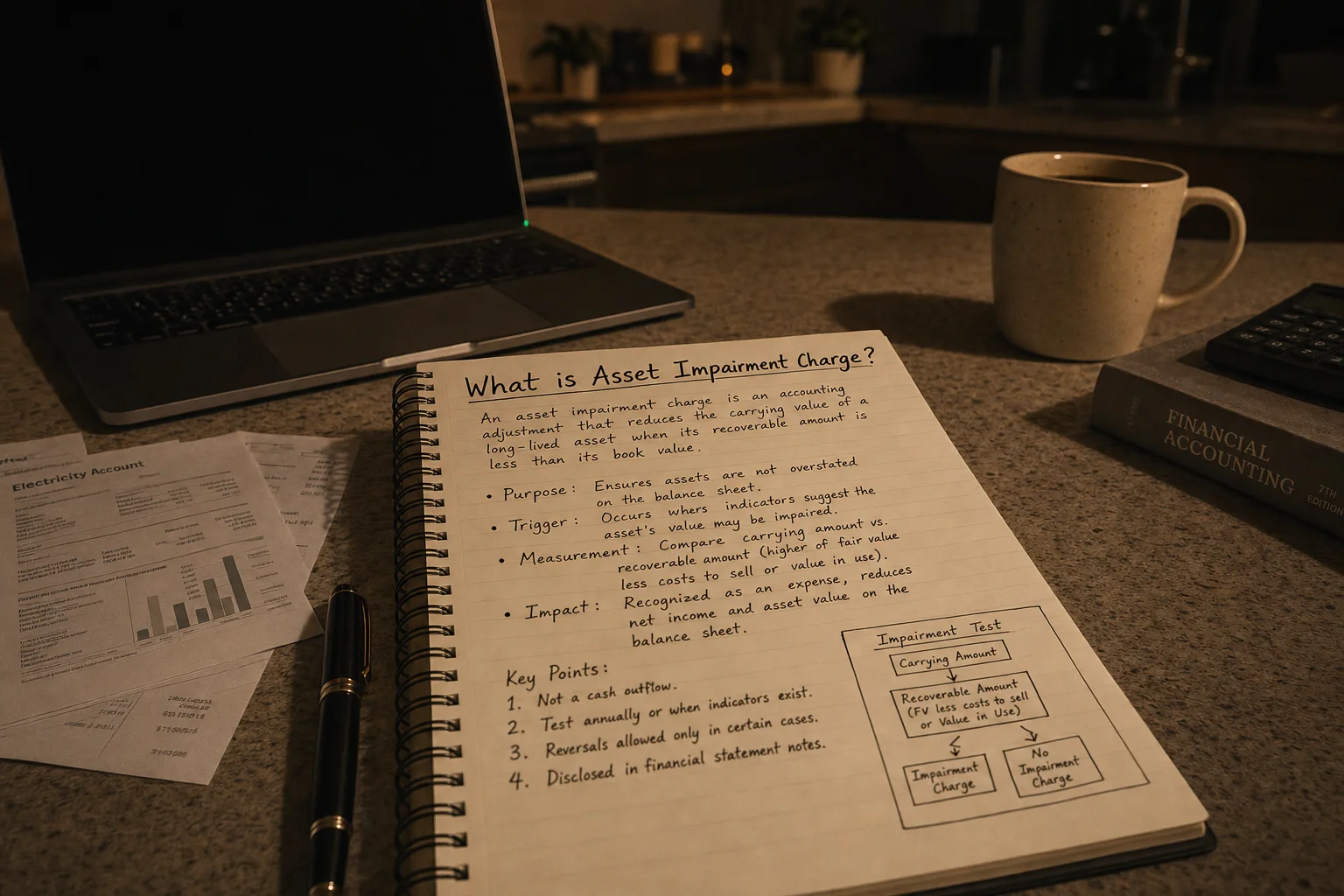

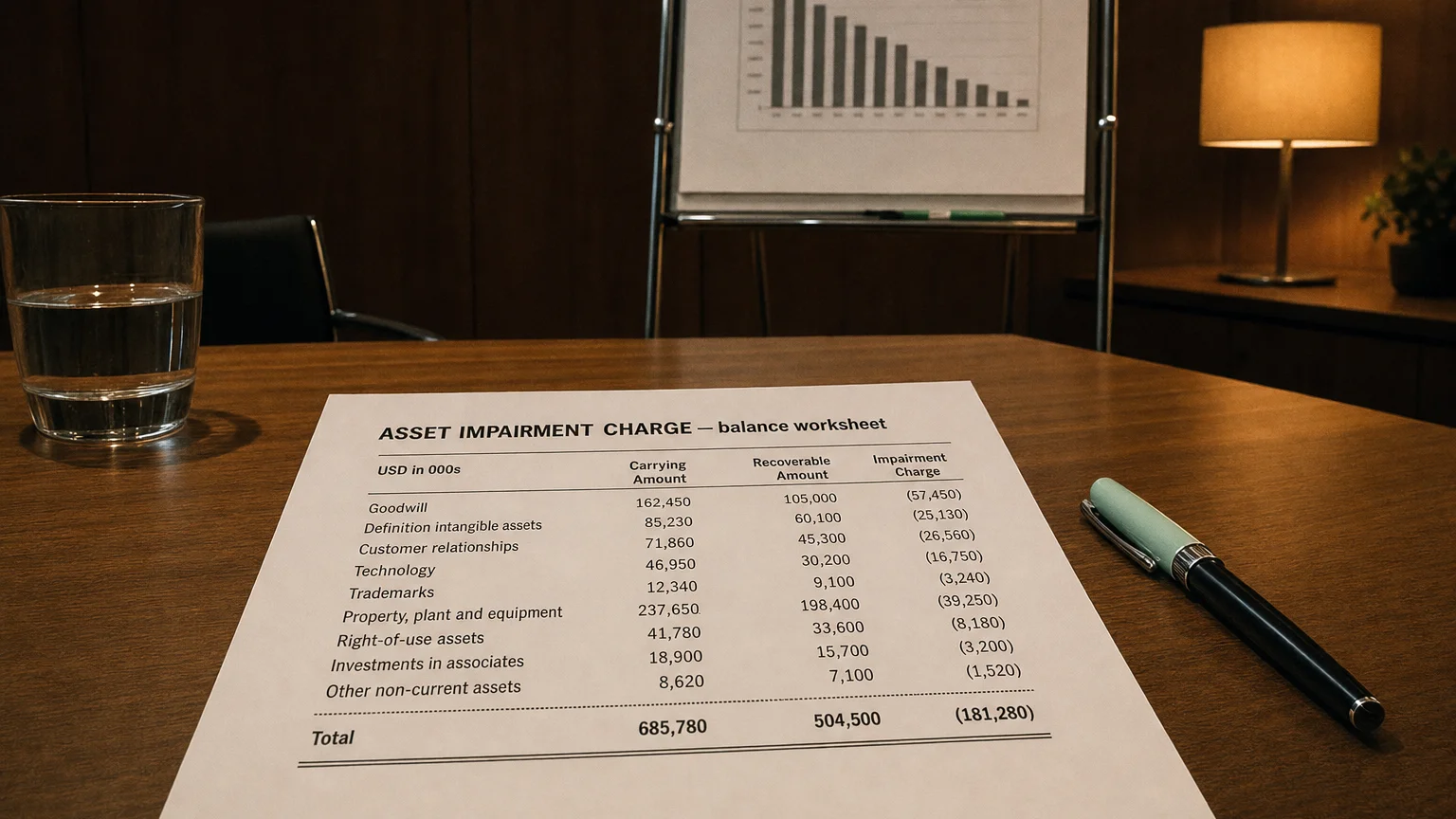

An asset impairment charge is a non-cash expense recorded when an asset's carrying value exceeds what the company can recover through use or sale. The charge writes the asset down to fair value, reducing earnings in the period recognized without any cash outflow.

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

Asset Impairment Charge is a non-cash expense recognized when the carrying amount of a long-lived asset (or asset group) exceeds its recoverable amount—meaning the company no longer expects to recover the recorded value through use or sale. It reflects a permanent decline in value and reduces the asset’s book value on the balance sheet while hitting earnings in the period it’s identified.

When and Why Impairments Happen

An asset’s value can drop permanently due to market changes, technology shifts, legal issues, or physical damage. Accounting rules force companies to test for impairment when ‘triggering events’ appear—don’t wait until sale.

- Significant decline in market value

- Adverse changes in technology or regulation

- Physical damage or obsolescence

- Worse-than-expected performance

- Plans to dispose earlier than planned

The charge writes the asset down to what it’s really worth now.

A Real-Life Example

Oil company built a refinery for $2 billion.

- Oil prices crash, demand shifts to renewables

- Expected future cash flows drop sharply

- Fair value now $1.2 billion

- Impairment test fails → $800M Asset Impairment Charge

Earnings take 1.2B—no cash leaves, but value loss recognized.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Testing Process Simplified

US GAAP (PP&E):

- Trigger event → recoverability test (undiscounted cash flows < carrying?)

- If fails → measure impairment (fair value < carrying)

- Charge = difference

IFRS: Annual test for intangibles/goodwill; others when indicators → single step to recoverable amount (higher of fair value less costs or value in use).

Goodwill impairment separate but similar logic.

Where It Hits the Statements

- Income statement: ‘Asset Impairment Charge’ (often operating or ‘Other’)

- Balance sheet: Reduces asset carrying value

- Cash flow: Non-cash add-back in operating activities

Future depreciation lower (smaller base).

Common Scenarios

- Energy: Oil/gas reserves or rigs (price crashes)

- Retail: Store closures (e-commerce shift)

- Tech: Acquired patents obsolete

- Telecom: Network equipment stranded

- Manufacturing: Factory idled

What It Signals

- Permanent value destruction

- Strategic misstep or market shift

- Management admitting past over-optimism

- Cleaner balance sheet going forward

- Potential future margin improvement (lower depreciation)

Frequent or large charges may indicate poor capital allocation or industry headwinds.

Q · 01Does an asset impairment charge affect cash flow?+

Q · 02Can a company reverse an impairment charge?+

Q · 03What triggers an impairment test?+