Provision and Write-Off of Assets is a financial concept covered in this article. Non-Cash Charges for Expected or Confirmed Asset Value Reduction

It does not matter how frequently something succeeds if failure is too costly to bear.

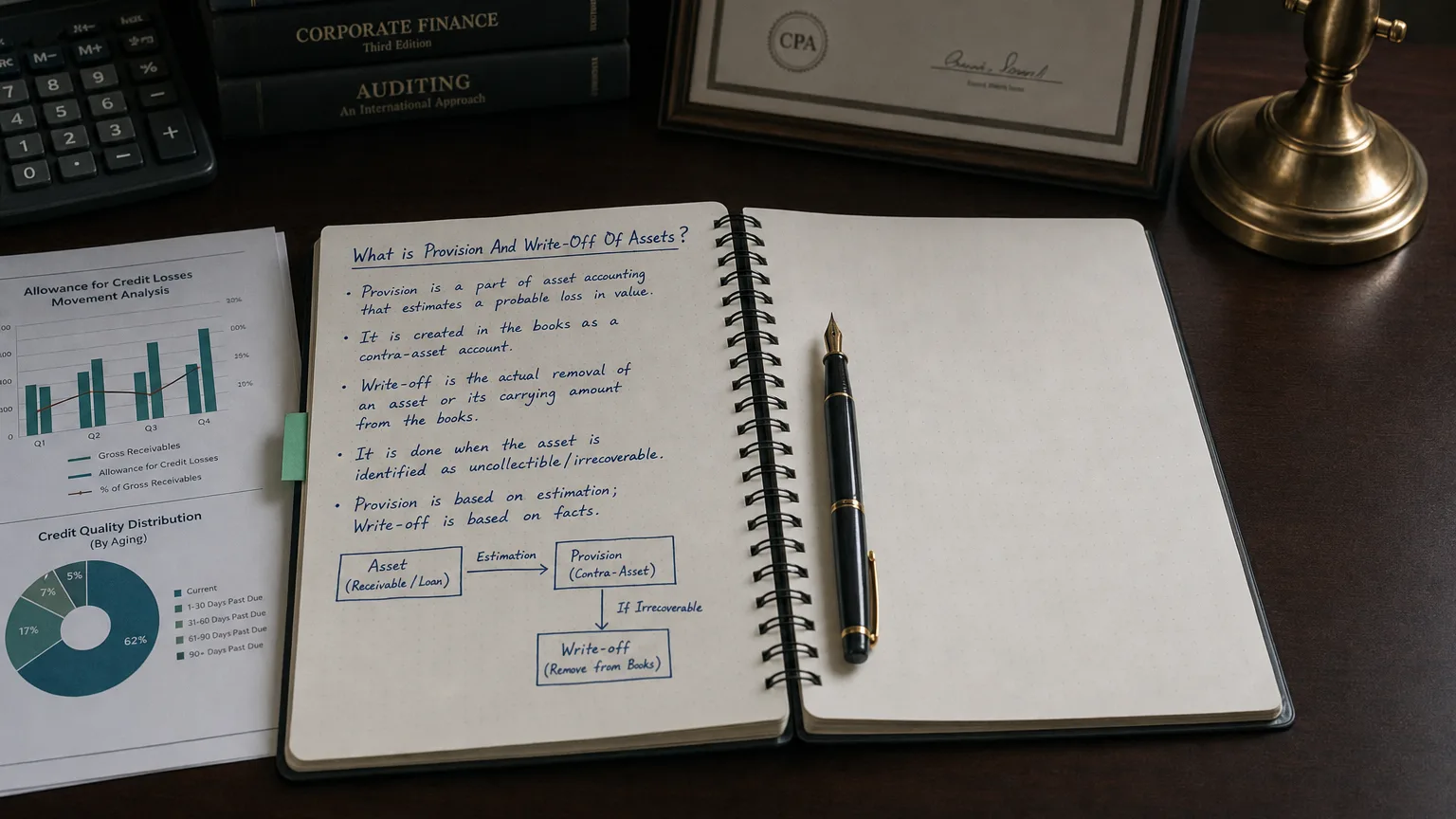

Provision and Write-Off of Assets is a non-cash expense line in the cash flow statement that captures charges taken when a company recognizes that certain assets—inventory, receivables, fixed assets, or intangibles—are impaired, obsolete, or uncollectible. Provisions are estimates of future losses, while write-offs are the actual removal of the asset when the loss is confirmed. Both add back to net income in operating cash flow since no cash left the company.

The Difference Between Provision and Write-Off

Companies don’t always know exactly when an asset goes bad—they estimate first.

A provision is the upfront estimate: you see trouble coming (slow-moving inventory, doubtful customer) and book a reserve/allowance now.

A write-off is the cleanup later: the inventory is truly obsolete or the customer definitely won’t pay—you remove the asset entirely.

Both are non-cash hits to earnings, added back in cash flow.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

Real Examples That Make It Clear

Fashion retailer:

- End of season: Last year’s styles unlikely to sell → provision $5M inventory reserve (expense now)

- Next year: Confirm styles unsellable → write-off $5M (reduce inventory and reserve—no new expense)

Tech company:

- Customer bankruptcy risk → provision $2M bad debt allowance

- Customer actually files → write-off $2M receivable

Manufacturer:

- Old machinery no longer usable → $10M impairment provision/write-off

Common Types of Provisions/Write-Offs

- Inventory obsolescence or shrinkage

- Bad debt / doubtful receivables

- Asset impairments (PP&E, intangibles, goodwill)

- Warranty or return reserves

- Restructuring charges (facility closure costs)

- Environmental or legal provisions

How It Flows in Cash Flow Statement

Indirect method operating activities:

- Net Income (reduced by provision/write-off expense)

-

- Provision and Write-Off of Assets (non-cash add-back)

- = Higher operating cash flow

Cash isn’t affected until actual payment (e.g., warranty claims paid).

Why Companies Take These Charges

- Conservative accounting (lower of cost or NRV/market)

- Matching principle (expense when value lost)

- Clean up balance sheet (remove dead assets)

- Regulatory requirement (impairment testing)

- Big bath restructuring (front-load losses)

What to Watch For

- Trend (rising = deteriorating asset quality?)

- Size vs. revenue (material = issues)

- Recurring large charges (chronic problems?)

- Reversals (boosting future earnings?)

- Link to industry cycle (tech obsolescence fast)

Frequent provisions followed by reversals can signal earnings management.