is a financial concept covered in this article. Cash Inflows from Non-Repayable Government Assistance

If we avoid the losers, the winners will take care of themselves.

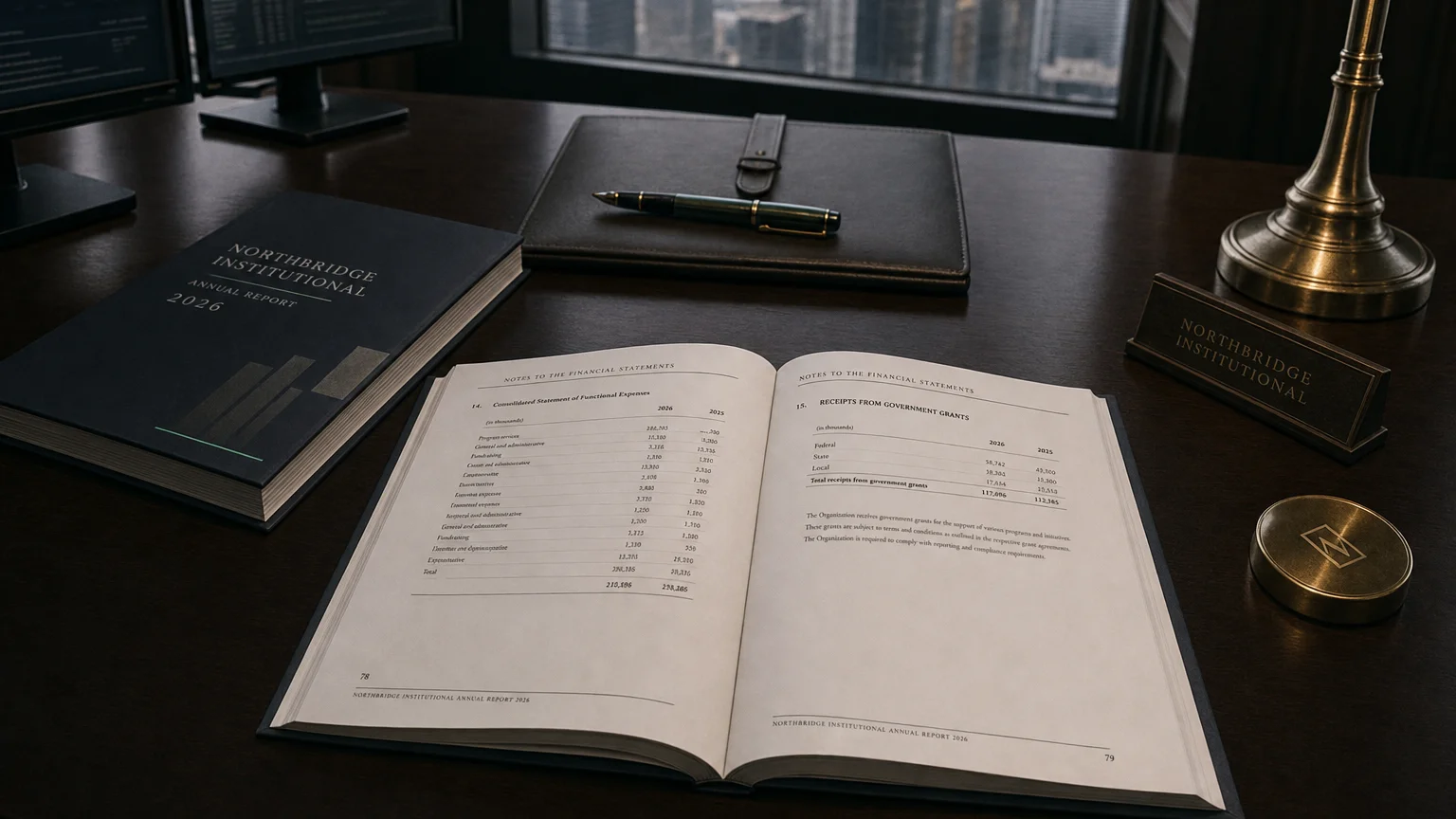

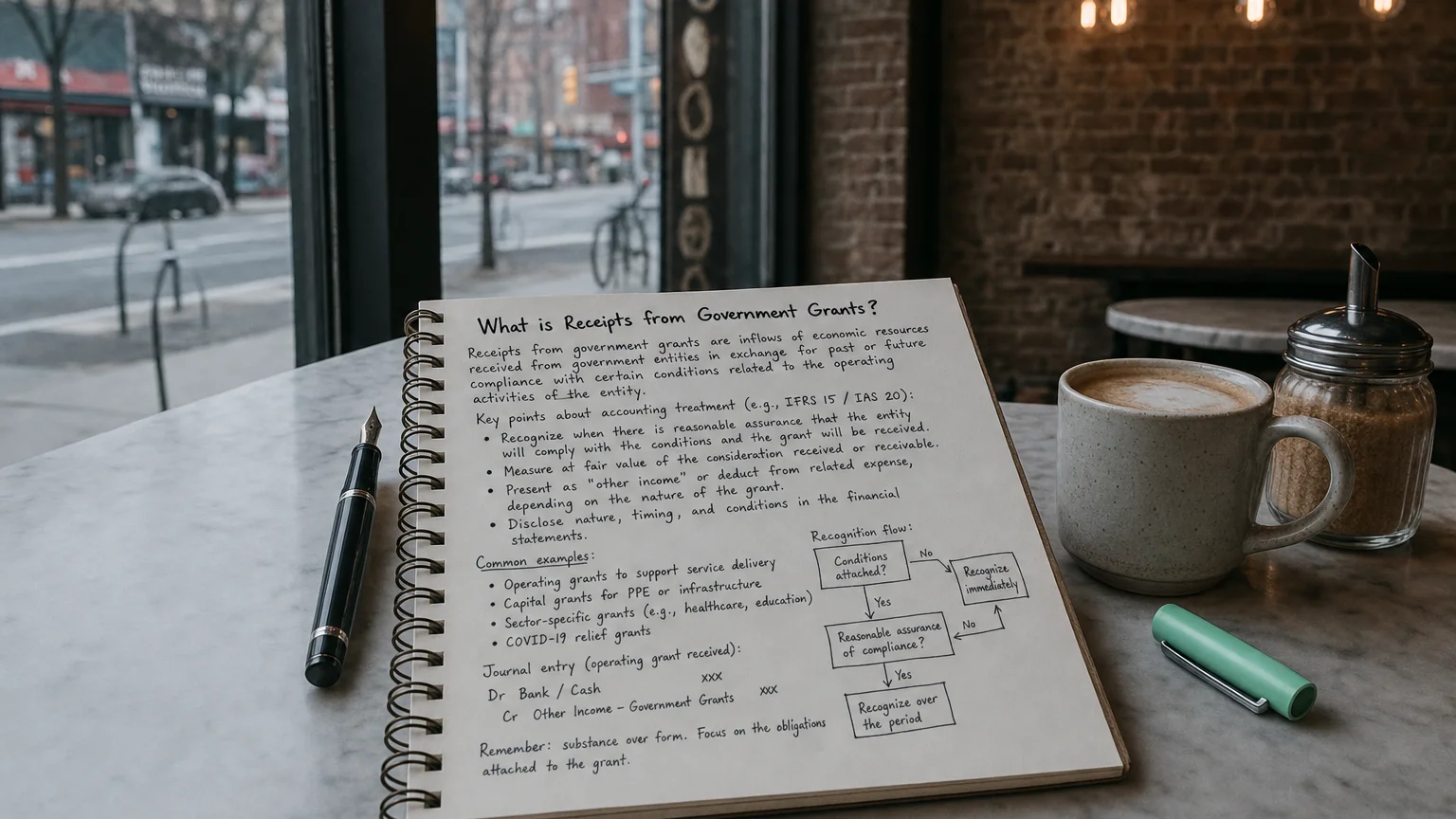

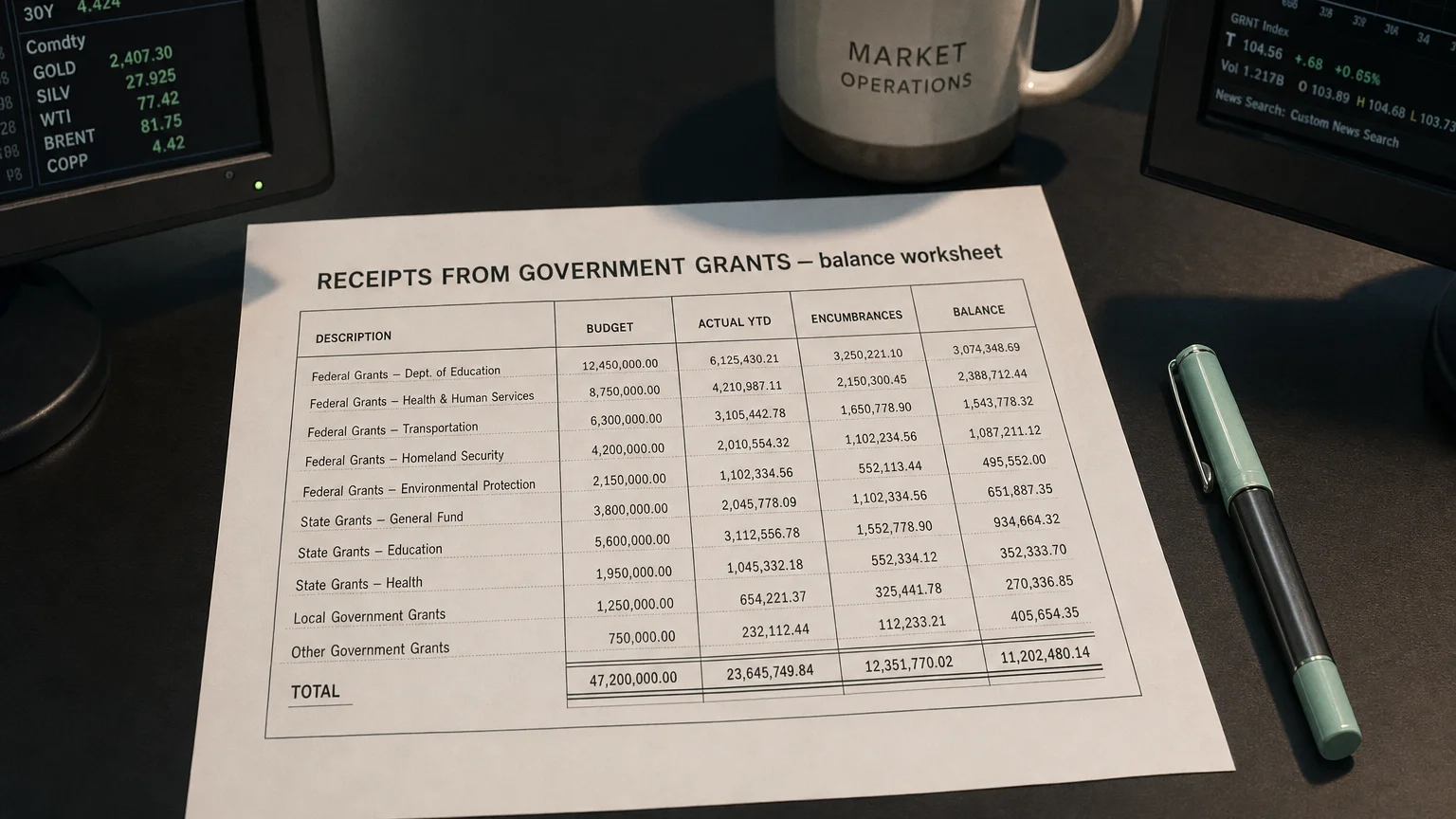

Receipts from Government Grants is the cash received from government entities as grants, subsidies, or other forms of financial assistance that do not require repayment. This line appears in the operating activities section of the cash flow statement (direct method) or as a supplemental disclosure, reflecting non-revenue cash support tied to operational objectives, research, employment, or capital projects.

What It Represents

Receipts from Government Grants are cash transfers from public authorities to support business activities—often with conditions like job creation, R&D spending, or environmental goals.

Unlike loans (repayable), grants are free money, but strings attached mean you earn them by meeting targets.

Capital grants (for assets) may defer income; operating grants hit P&L sooner.

“If we avoid the losers, the winners will take care of themselves.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Common Types of Grants

- R&D tax credits or innovation grants

- Employment/wage subsidies (hiring or retention)

- Green energy or sustainability incentives

- Export promotion or regional development aid

- COVID/recovery support packages

- Investment grants for plant/equipment

Tech, manufacturing, and agriculture often benefit most.

A Practical Example

Electric vehicle battery maker:

- Receives $50M government grant to build new factory

- Conditions: create 500 jobs, meet production targets

- Cash received upfront or in stages

- Cash flow: +$50M Receipts from Government Grants (operating if tied to expenses)

- Income recognized as conditions met

Boosts cash without debt or dilution.

Accounting Treatment

- Operating grants: Income when conditions met

- Capital grants: Deferred and released over asset life

- Cash flow: Operating (revenue-like) or investing (asset-related)

- Direct method: Separate receipt line

- Indirect: Supplemental disclosure

IFRS IAS 20: Systematic recognition; US GAAP similar for non-exchange.

Presentation

Cash flow statement:

- Direct method: ‘Receipts from Government Grants’

- Indirect: Supplemental or in ‘Other operating receipts’

- Operating activities (most common)

Income statement: ‘Government grant income’ or offset expenses.

What It Signals

- Government support reliance

- Alignment with policy priorities (green, innovation)

- Cash boost without dilution

- Potential clawback risk if conditions missed

- Earnings quality (non-recurring?)

Heavy dependence can expose to policy changes.

Q · 01What is Receipts From Government Grants?+