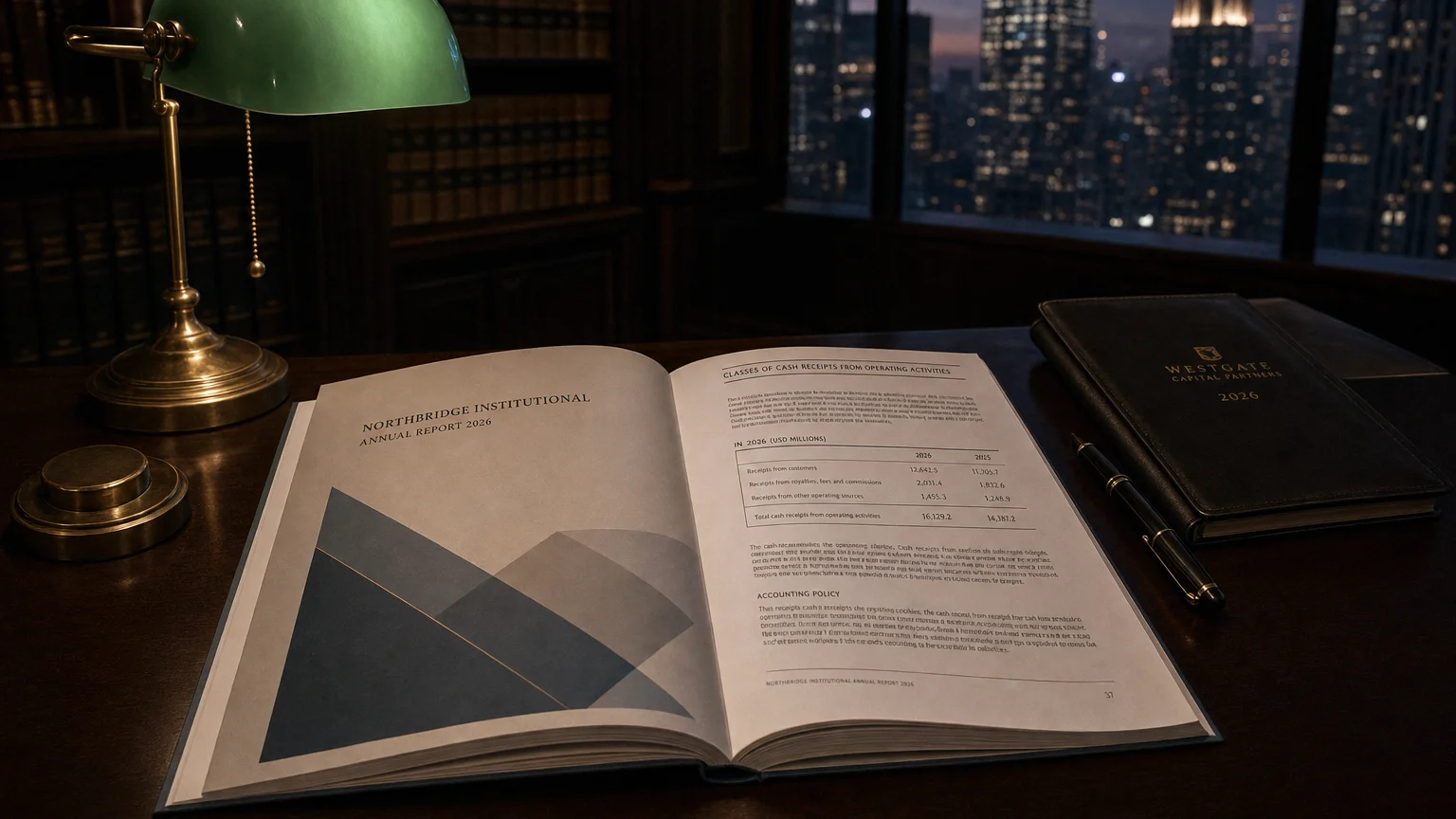

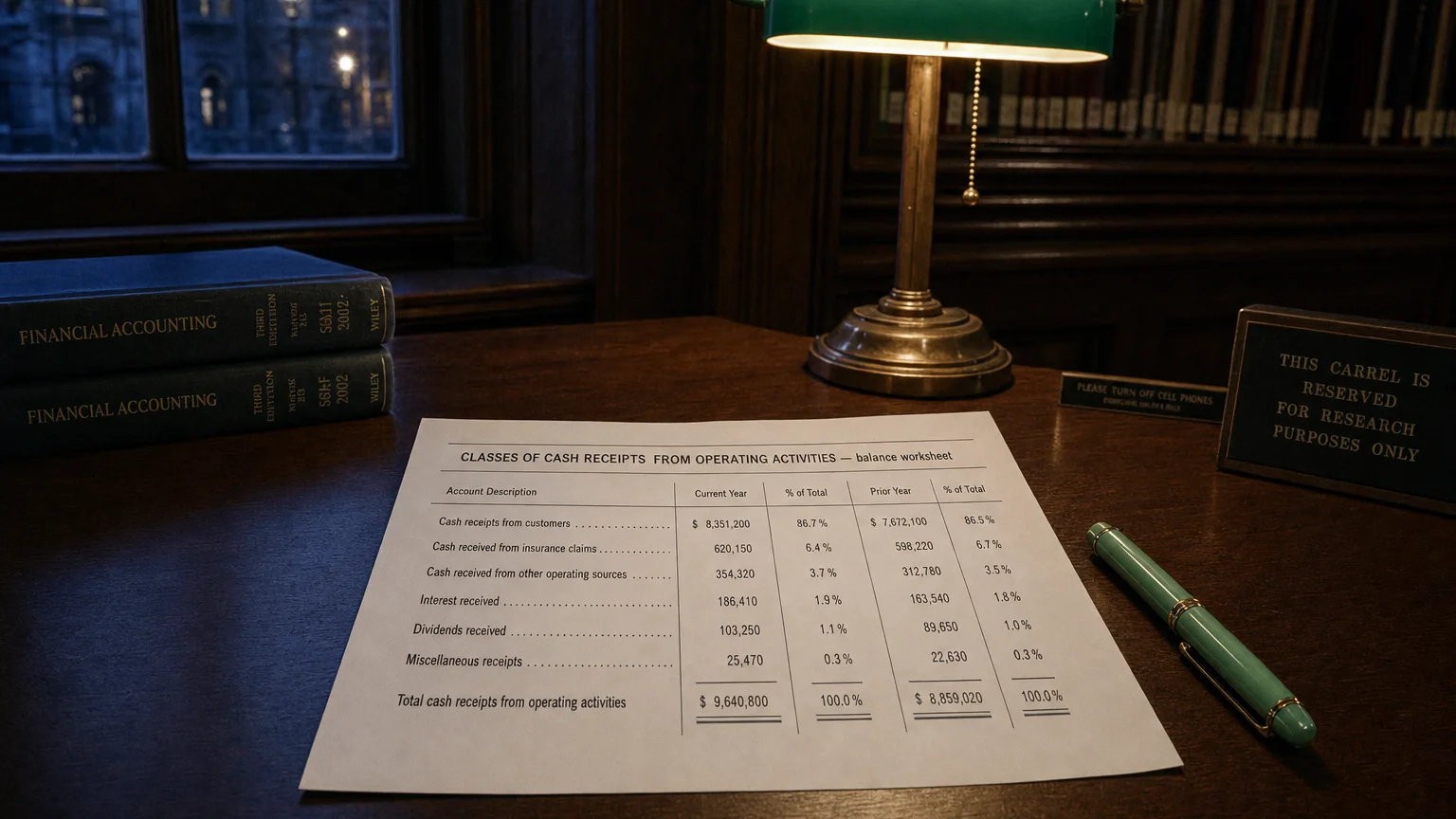

Classes of cash receipts from operating activities categorizes gross cash inflows under the direct method—chiefly receipts from customers, plus interest, dividends, or government grants when material. The total, minus cash payments, equals net operating cash flow.

In investing, you get what you don't pay for. Costs matter enormously.

Classes of Cash Receipts from Operating Activities refers to the breakdown of major types of cash inflows in the direct method presentation of operating cash flows. The direct method lists gross cash receipts grouped into logical classes—primarily from customers, but also interest, dividends, or other operating sources—to show exactly where operating cash is coming from.

What It Really Shows

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

The direct method flips the usual indirect approach on its head. Instead of starting with net income and tweaking for non-cash items, it lists the big buckets of actual cash coming in from operations.

Classes of cash receipts make those inflows crystal clear—mostly money from customers, but also other operating sources when material.

You see the raw cash engine of the business without accrual noise.

Typical Classes You’ll See

Main Class

- Receipts from customers (sales of goods/services)

Other Common Classes

- Interest received (if operating classification)

- Dividends received (if operating classification)

- Receipts from government grants

- Insurance proceeds or refunds

- Other operating cash receipts (royalties, settlements)

Companies add lines based on what’s big for them.

A Practical Example

Manufacturer using direct method:

- Receipts from customers: +$1,200M

- Interest received: +$15M

- Government subsidy grant: +$10M

- Other operating receipts: +$5M

- Total cash receipts: +$1,230M

Pair with payments to get net operating cash flow.

Direct Method Context

In direct method operating section:

- Classes of cash receipts (detailed lines)

- Minus classes of cash payments

- = Net cash from operating activities

Gross transparency—every major inflow visible.

Why Some Companies Use It

- Clearer picture of cash from customers

- Better insight into collection efficiency

- Highlights non-sales operating cash (grants, interest)

- Easier for non-accountants

- IAS 7 encourages it

Still uncommon—most prefer indirect for ease.

What It Tells You

- True cash from sales (vs. accrual revenue)

- Collection timing and effectiveness

- Non-sales operating income cash

- Subsidy or grant reliance

- Operational cash generation sources

Receipts lower than revenue = growing receivables or slow collections.

Q · 01What is the primary class of operating cash receipts?+

Q · 02Can interest received be classified as an operating receipt?+