Cash flow from discontinued operations is the net cash—operating, investing, and financing—generated or used by a segment sold, closed, or held for sale. It is reported separately to preserve the clarity of continuing-operations cash flow.

Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

Cash Flow From Discontinued Operation represents the net cash provided by (or used in) operating, investing, and financing activities related to business components that have been disposed of or are classified as held for sale. These cash flows are reported separately from continuing operations to give a clear picture of the ongoing core business performance and the impact of exited or exiting segments.

What It Captures

When a company decides to exit a business line—selling a division, closing a plant, spinning off a unit—the cash flows from that part are reclassified as ‘discontinued’.

- Operating cash from the discontinued business until disposal

- Cash proceeds from selling the assets (investing inflow)

- Cash costs of shutdown or severance (often operating or investing outflow)

- Debt repayment tied to the disposed unit (financing)

The goal: let investors see cash generation from the remaining ‘continuing’ business.

Prior years’ cash flows are re-presented as discontinued for comparability.

A Real-Life Example

“Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

BigCorp sells its unprofitable widget division mid-year for $200M cash.

- Widget division generated $30M operating cash before sale

- Sale proceeds: $200M cash inflow

- Severance and shutdown costs: $15M outflow

- Net Cash Flow from Discontinued Operation: +$215M

This $215M appears separately—core business cash flow isn’t inflated by the one-time sale.

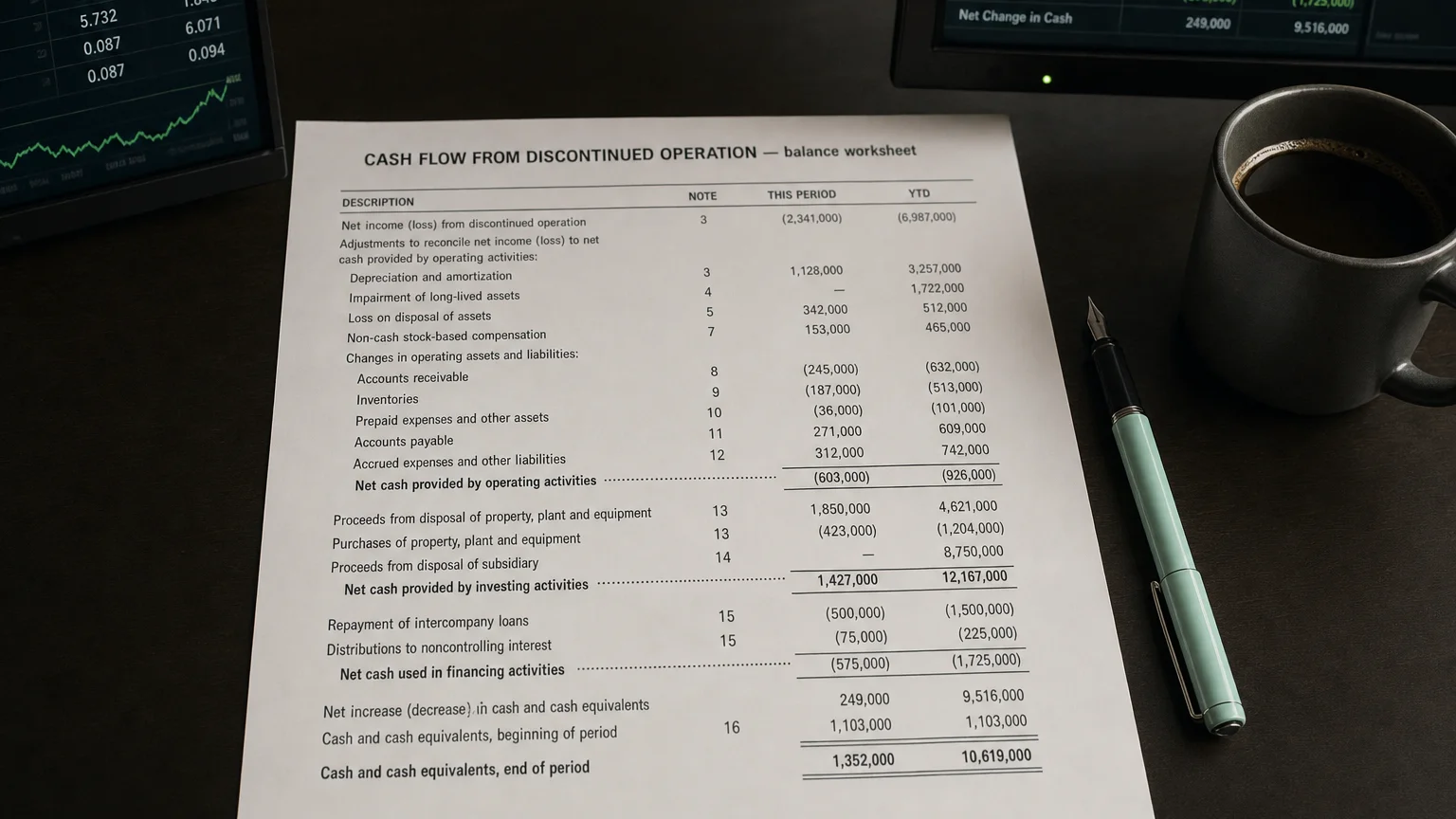

How It’s Presented

In the cash flow statement:

- Often a single net line: ‘Cash provided by (used in) discontinued operations’

- Or broken out: Operating, Investing, Financing from discontinued

- Subtotal for continuing operations above

- Total change in cash includes both

Footnotes detail components and nature of discontinued ops.

Why Companies Report It Separately

- Focus on sustainable core cash generation

- Avoid one-time sale proceeds boosting operating cash flow

- Highlight restructuring costs clearly

- Better valuation multiples on continuing business

- Comparability across periods

Common Scenarios

- Divestiture of non-core division

- Sale of underperforming segment

- Spin-off or closure of business line

- Regulatory-forced disposals

- Portfolio streamlining

What to Watch For

- Large positive from sale proceeds (one-time boost)

- Ongoing losses draining cash before disposal

- Shutdown costs offsetting proceeds

- Impact on continuing operations quality

- Recurring discontinued items (red flag for chronic issues)

Strip discontinued cash flows for true ongoing liquidity view.

Q · 01What triggers the separate reporting of discontinued cash flows?+

Q · 02Should analysts strip discontinued cash flows from valuation models?+

Q · 03What components make up discontinued operations cash flow?+