Cash from discontinued financing activities records debt repayments, equity transactions, and borrowing proceeds tied to business units classified as discontinued or held for sale. Separating these from continuing operations reveals the core company's true financing profile.

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

Cash From Discontinued Financing Activities captures the cash inflows and outflows from financing transactions specifically tied to business components classified as discontinued operations or held for sale. These are separated from continuing operations to provide a clean view of how the ongoing core business is funded, isolating the financing impact of exited or exiting segments.

What It Includes

This line item covers financing cash flows directly attributable to the discontinued component:

- Repayment of debt specifically tied to the disposed business

- Proceeds from new borrowing allocated to the unit (pre-disposal)

- Dividend payments or equity transactions within the discontinued entity

- Intercompany financing settlements related to the exit

- Capital contributions or returns specific to the segment

Only financing clearly linked to the discontinued operation is separated.

Most common: debt payoff from sale proceeds or pre-sale refinancing.

A Practical Example

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

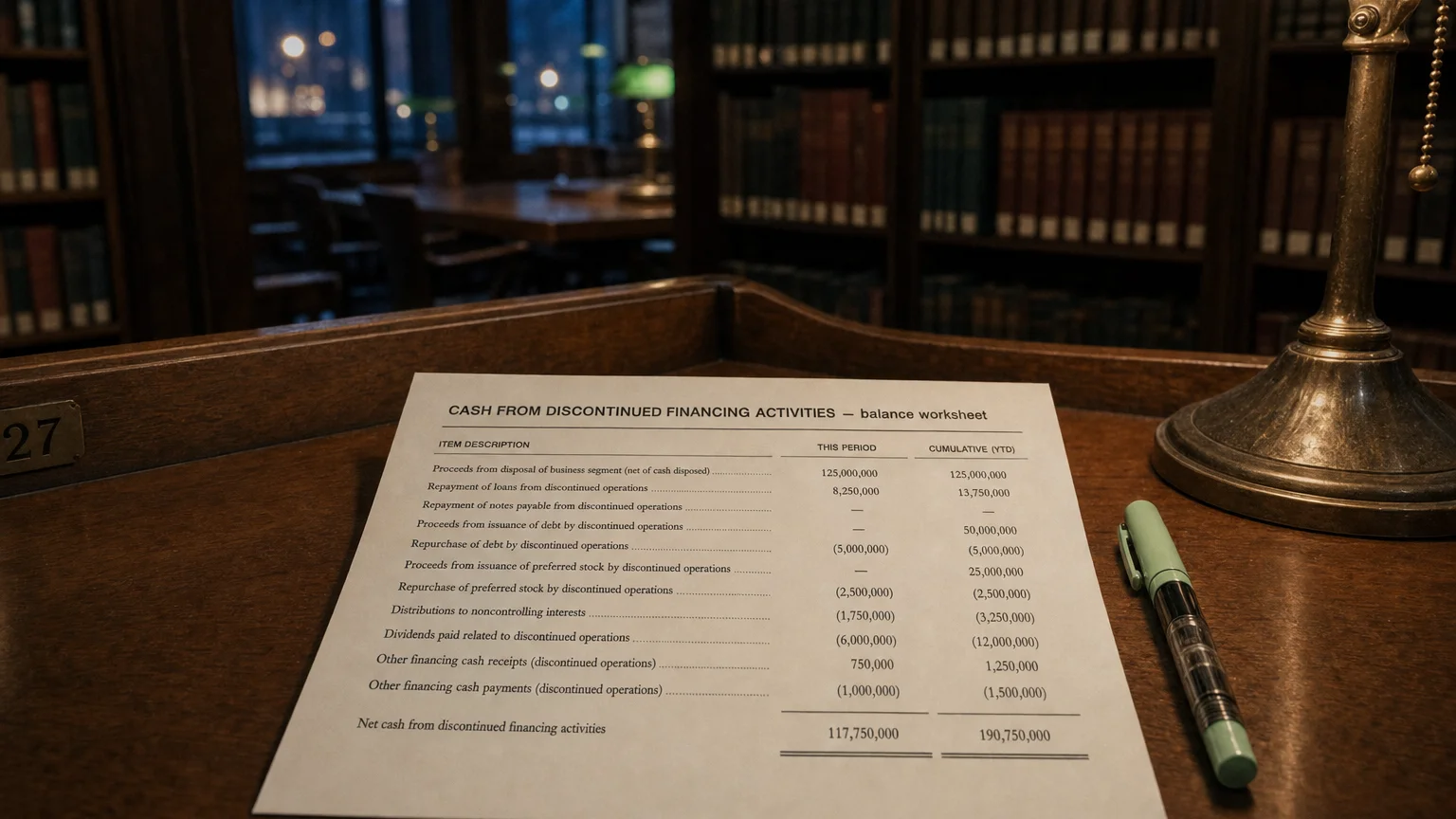

BigCorp sells its widget division for $300M cash.

- Widget division had $100M dedicated bank loan

- Sale agreement requires paying off the loan at closing

- Use 100M outflow in discontinued financing activities

- Remaining $200M proceeds → discontinued investing inflow

Core business financing cash flow remains unaffected by the debt payoff.

How It’s Presented

In the cash flow statement:

- Separate section or line for discontinued operations

- Often subtotaled: ‘Cash provided by (used in) discontinued financing activities’

- Or single net ‘Cash flows from discontinued operations’ with breakdown in notes

- Prior periods re-presented for comparability

Total cash change includes both continuing and discontinued.

Why Separate Reporting Matters

- Clean view of ongoing capital structure and funding needs

- Avoid one-time debt payoffs distorting continuing financing

- Better assessment of core leverage and dividend capacity

- Accurate free cash flow to equity for continuing ops

- Comparability across years despite divestitures

Common Scenarios

- Debt repayment from divestiture proceeds

- Pre-sale refinancing of disposed unit

- Equity transactions in subsidiary being spun off

- Intercompany loan settlements on disposal

- Capital lease terminations tied to closed facilities

What to Look For

- Large outflows = debt cleanup (positive for core leverage)

- Inflows = new borrowing for discontinued unit (rare post-classification)

- Net impact on total cash

- Comparison to continuing financing (core funding sources)

- Recurring discontinued items (ongoing restructuring?)

Exclude discontinued financing when evaluating ongoing capital structure.

Q · 01What qualifies as discontinued financing activity?+

Q · 02How does it differ from continuing financing activities?+

Q · 03Why exclude discontinued financing from valuation models?+