Interest Paid CFF is a financial concept covered in this article. Cash Interest Payments Classified as Financing Activities

Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

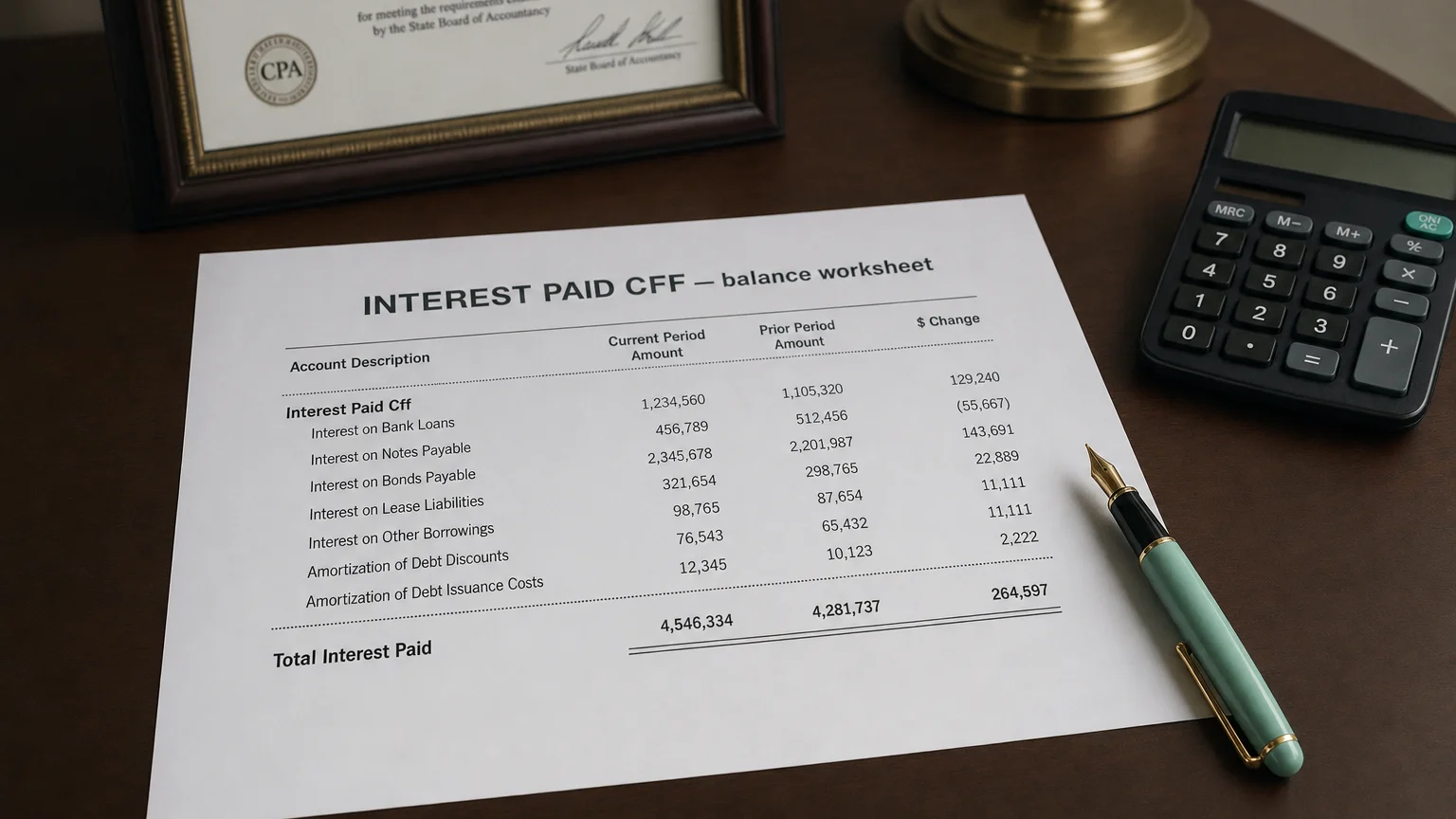

Interest Paid CFF (Interest Paid – Cash Flow Financing) is the actual cash outflow for interest expenses on debt that a company classifies in the financing activities section of the cash flow statement. This classification choice—allowed primarily under US GAAP—treats interest as part of the cost of obtaining capital rather than an operating expense, differing from the more common operating activities treatment.

Why Some Companies Put Interest in Financing

Under US GAAP, companies have a choice: treat cash interest paid as operating (like IFRS requires) or financing. Many pick financing because interest is the ‘cost of borrowing money’—similar to repaying debt principal.

Moving it to financing boosts reported Operating Cash Flow (OCF), a key metric watched by investors and often tied to executive bonuses.

IFRS mandates operating classification—no choice.

A Clear Example

Company has 5M annual interest expense.

- IFRS or Operating choice: 5M

- US GAAP Financing choice: $5M outflow in Financing Activities → OCF unchanged by interest

All else equal, the financing classification makes Operating Cash Flow look $5M stronger.

“Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

Where It Shows Up

In the cash flow statement financing section:

- ‘Interest Paid’

- ‘Cash Paid for Interest’

- Sometimes grouped in ‘Net Other Financing Charges’

- Supplemental note discloses total interest paid (regardless of classification)

Companies must disclose the policy in footnotes.

Who Uses This Classification

- Many large US non-financial companies (Apple, Walmart, etc.)

- Firms focused on OCF metrics or EBITDA-like views

- Companies with high debt but wanting strong operating cash appearance

Financial institutions (banks) usually classify interest as operating—it’s their core business.

Pros and Cons

Advantages

- Higher reported OCF

- Aligns with view of interest as financing cost

- Consistent with debt principal treatment

Drawbacks

- Reduces comparability with IFRS companies

- Financing section looks worse

- Can mask true operating cash needs

What to Watch For

- Policy consistency year-to-year

- Comparison to peers (mix of classifications common)

- Supplemental total interest paid (true cash outflow)

- OCF quality—add back if comparing across policies

- Debt levels vs. boosted OCF

High OCF from financing classification may overstate operational strength.

Q · 01What is Interest Paid Cff?+