Interest Paid CFO is a financial concept covered in this article. Cash Interest Payments Classified as Operating Activities

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

Interest Paid CFO (Interest Paid – Cash Flow Operating) is the actual cash outflow for interest on borrowings that a company classifies in the operating activities section of the cash flow statement. This treatment—required under IFRS and a common choice under US GAAP—views interest expense as part of day-to-day operations rather than purely a financing cost.

Why Interest Paid Goes to Operating

Think of interest as the ongoing cost of using borrowed money to run the business—paying suppliers faster, holding inventory, funding growth. IFRS says put it in operating because it’s tied to everyday activities.

Many US companies agree and choose operating too—it keeps Operating Cash Flow honest, showing the true cash drain from debt in core results.

Contrast: Some US firms shift it to financing, treating interest like repaying capital (boosts OCF).

Banks/insurers usually operating—interest is their core product.

A Clear Example

Company has 10M annual interest.

- IFRS or Operating choice: -10M

- Financing choice (US only): -$10M in Financing → OCF unchanged by interest

Operating classification shows the real cash burden of debt on operations.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Where It Shows Up

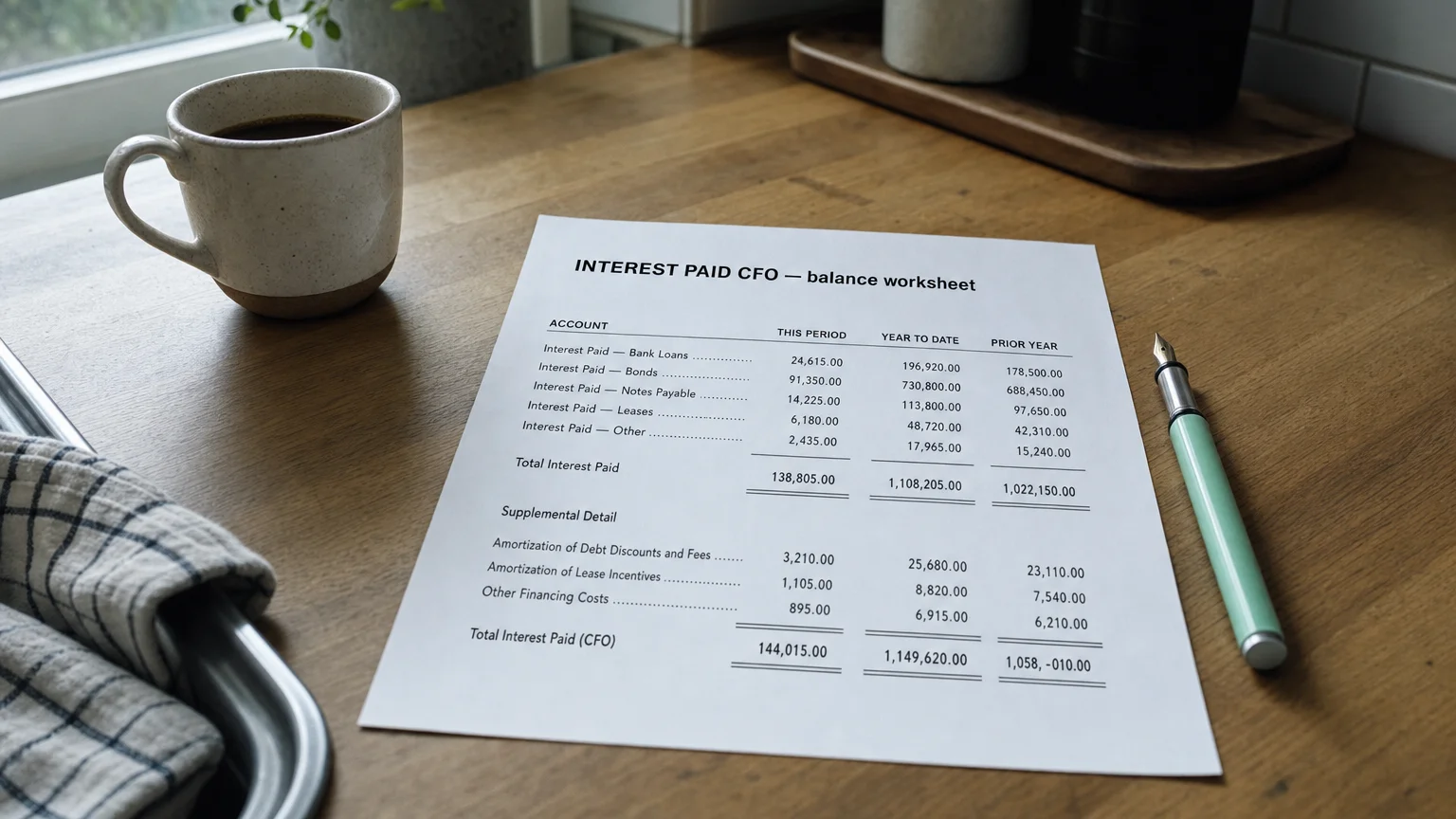

In the cash flow statement operating section:

- ‘Interest Paid’

- ‘Cash Paid for Interest’

- Direct method: explicit line

- Indirect: supplemental disclosure

Supplemental note shows total interest paid regardless of classification.

Who Uses Operating Classification

- All IFRS reporters (mandatory)

- Many US industrials, retailers, manufacturers

- Companies wanting transparent OCF

- Firms with interest as operational cost

Financial firms: operating (core business).

Pros and Cons

Advantages (Operating)

- Transparent OCF (shows full operating burden)

- Consistent globally (IFRS)

- Better comparability with peers

Advantages (Financing)

- Higher OCF

- Aligns interest with capital cost

What to Watch For

- Policy choice (US GAAP) and consistency

- Impact on OCF quality

- Comparison across companies (different classifications)

- Supplemental total interest paid

- Debt levels vs. OCF drag

Operating classification can make high-debt companies look weaker on OCF.

Q · 01What is Interest Paid Cfo?+