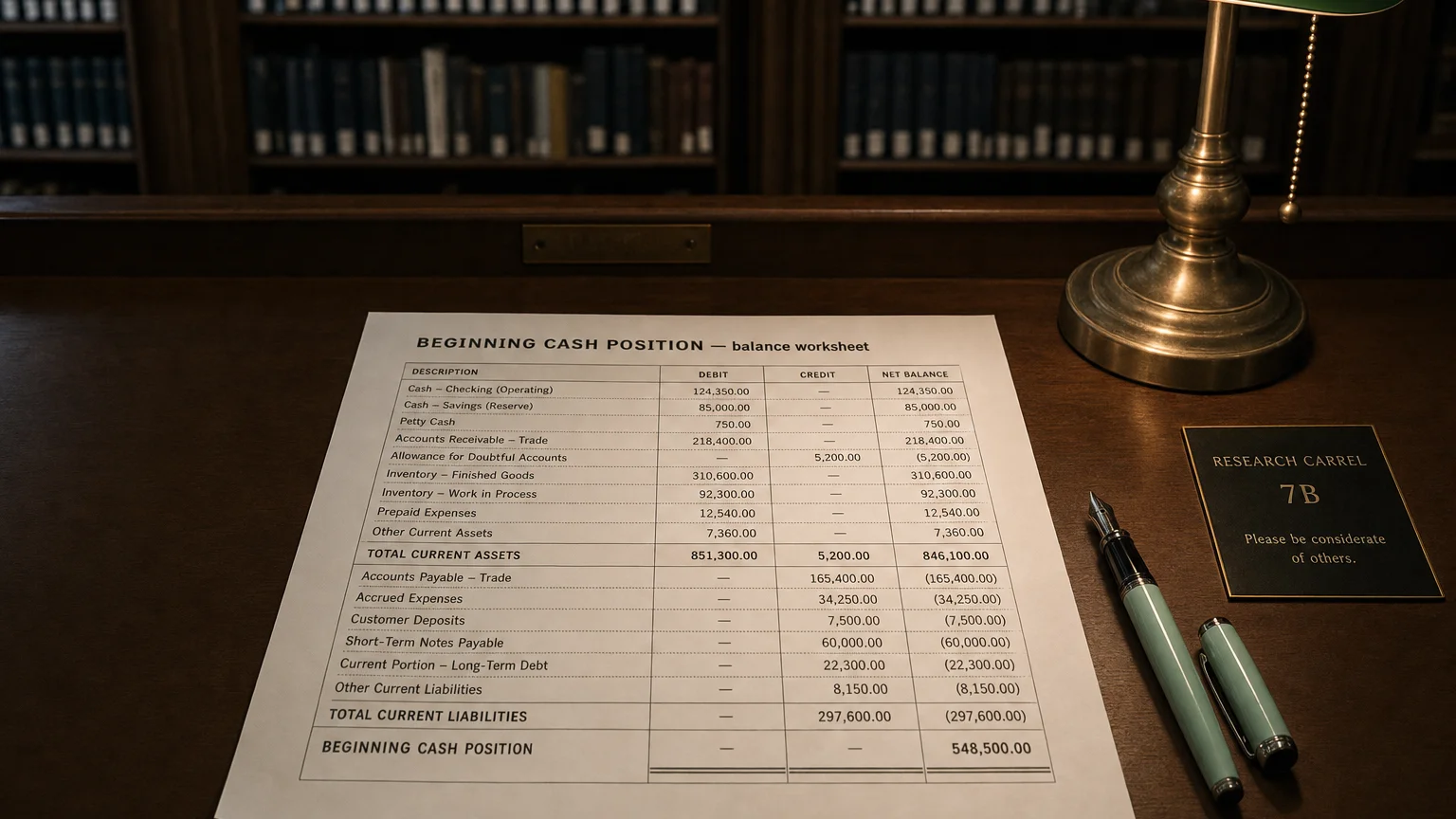

The beginning cash position is the total cash and cash equivalents a company holds at the start of an accounting period. It equals the ending cash balance of the prior period and serves as the base for calculating the current period's ending cash.

Survival comes first, truth, understanding, and science later.

The beginning cash position (also called the beginning cash balance or opening cash balance) is the amount of cash and cash equivalents a company has at the very start of an accounting period. In other words, it represents the cash on hand before any new cash inflows or outflows for the period occur. This figure includes both physical cash and highly liquid short-term investments, as financial statements typically group them together. The beginning cash position serves as the essential baseline from which all of the period’s cash activities are tracked and measured.

Derivation and Placement on the Cash Flow Statement

The beginning cash position isn’t calculated from scratch; it is directly pulled from the company’s prior financial records. Specifically, the beginning cash balance for the current period is always equal to the ending cash balance from the immediately preceding period. Last period’s closing cash becomes this period’s opening cash. This ensures a seamless and continuous record of a company’s cash over time.

On a Statement of Cash Flows, the beginning cash position is displayed near the bottom of the report. It is a key component of the cash reconciliation that summarizes the period’s activities. After detailing the net cash flow from operating, investing, and financing activities, the statement will show the following reconciliation:

- Net Increase (or Decrease) in Cash

- Plus: Cash and cash equivalents at beginning of the period

- Equals: Cash and cash equivalents at end of the period

“Survival comes first, truth, understanding, and science later.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Skin in the Game: Hidden Asymmetries in Daily Life (2018)

The Crucial Link to the Balance Sheet

The beginning cash position serves as a critical link between consecutive financial periods and directly ties the Statement of Cash Flows to the Balance Sheet. Since the beginning cash for this period is the same as the ending cash from the last period, it must match the ‘Cash and Cash Equivalents’ asset line item on the prior period’s balance sheet.

Ensuring Financial Statement Integrity

This continuity is essential for accurate financial reporting. Any discrepancy between a period’s ending cash on the balance sheet and the next period’s beginning cash on the cash flow statement would signal a significant error. This link ensures that the cash flow statement properly explains the change in the cash balance from one balance sheet to the next.

Why the Beginning Cash Position is Important for Analysis

Understanding the beginning cash position is fundamental for several reasons in financial analysis and management:

- Provides Financial Continuity: It ensures that the financial narrative is unbroken from one period to the next, giving users confidence that no cash has been accounted for incorrectly between periods.

- Acts as a Check for Accuracy: The cash reconciliation (Beginning Cash + Net Change = Ending Cash) serves as an internal check. If the calculation does not result in the correct ending cash figure that ties to the balance sheet, it indicates an error in accounting for cash inflows or outflows.

- Gives Context for Cash Flow Analysis: The opening balance provides crucial context for the period’s cash activities. For example, a 1 million in cash than for one that started with $50 million.

- Aids in Planning and Financial Management: For internal purposes, businesses rely on the beginning cash balance for budgeting and forecasting. Every cash plan for a new period starts with the opening cash balance to determine if the company has sufficient liquidity to meet its anticipated expenses and investments.

Q · 01Where does the beginning cash position appear on financial statements?+

Q · 02How is the beginning cash position calculated?+

Q · 03Why does the beginning cash position matter for financial analysis?+