Other Cash Adjustment Inside Change in Cash is a financial concept covered in this article. Miscellaneous Items Included Within the Net Change in Cash

It does not matter how frequently something succeeds if failure is too costly to bear.

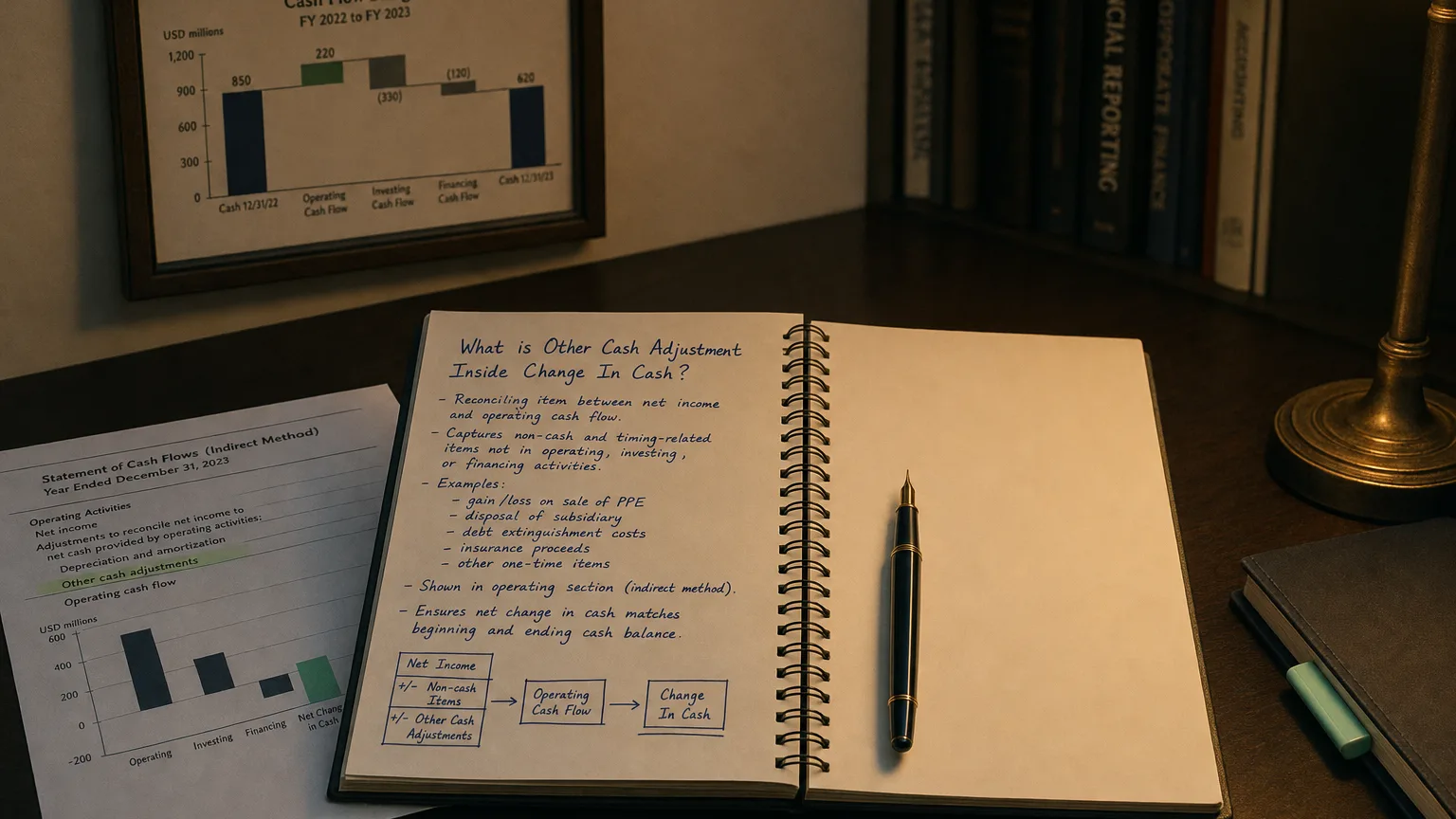

Other Cash Adjustment Inside Change in Cash captures smaller or miscellaneous cash flows that occur during the period and are part of the overall net increase or decrease in cash, but are not separately broken out in the main operating, investing, or financing sections of the cash flow statement. These adjustments are bundled into the reported ‘Change in Cash’ rather than shown outside the reconciliation like FX effects or restricted cash movements.

Why This Category Exists

Cash flow statements group major activities into operating, investing, and financing. But not every cash move fits neatly—or is big enough—to warrant its own line.

These ‘other’ adjustments inside the change in cash pick up the odds and ends that still affect actual cash but are too small, varied, or incidental to break out separately.

They’re ‘inside’ because they contribute to the net cash flow from the three main sections, unlike FX or restricted cash moves shown outside.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

Typical Items Included

- Cash overdraft changes (if classified as cash equivalent)

- Minor bank fees or service charges

- Small cash items in acquisitions/divestitures

- Cash settlements of non-derivative hedges

- Proceeds/expenses from minor asset sales not separately disclosed

- Other incidental operating or financing cash flows

They’re usually immaterial individually but collectively explain residual cash movement.

A Simple Example

Company’s cash flow statement shows:

- Operating cash flow: +$50M

- Investing: -$20M

- Financing: +$5M

- Net change before adjustments: +$35M

Actual cash increased 2M? A small cash receipt from selling old office equipment and minor bank fee refund—both too small for separate lines, so lumped as ‘Other Cash Adjustment Inside Change in Cash’.

Where It Shows Up

Usually in supplemental cash flow disclosures or footnotes:

- Within operating, investing, or financing sections as ‘Other’

- Reconciliation table breaking out the net change

- Not always explicitly labeled—sometimes just ‘Net cash provided by operating activities’ includes it

Larger companies may disclose components if material.

Contrast with ‘Outside’ Adjustments

Inside Change in Cash

- Actual cash transactions

- Part of O/I/F totals

- Affect net cash flow line

Outside Change in Cash

- Non-transactional (FX translation)

- Reclassifications (restricted cash)

- Added after net cash flow

What It Tells You

- Clean-up of small cash items

- Operational tidiness (or lack of detail)

- Potential for hidden positive/negative flows

- Materiality threshold of disclosures

- Full picture when reconciled to balance sheet

Large ‘other’ can merit footnote digging for unusual items.