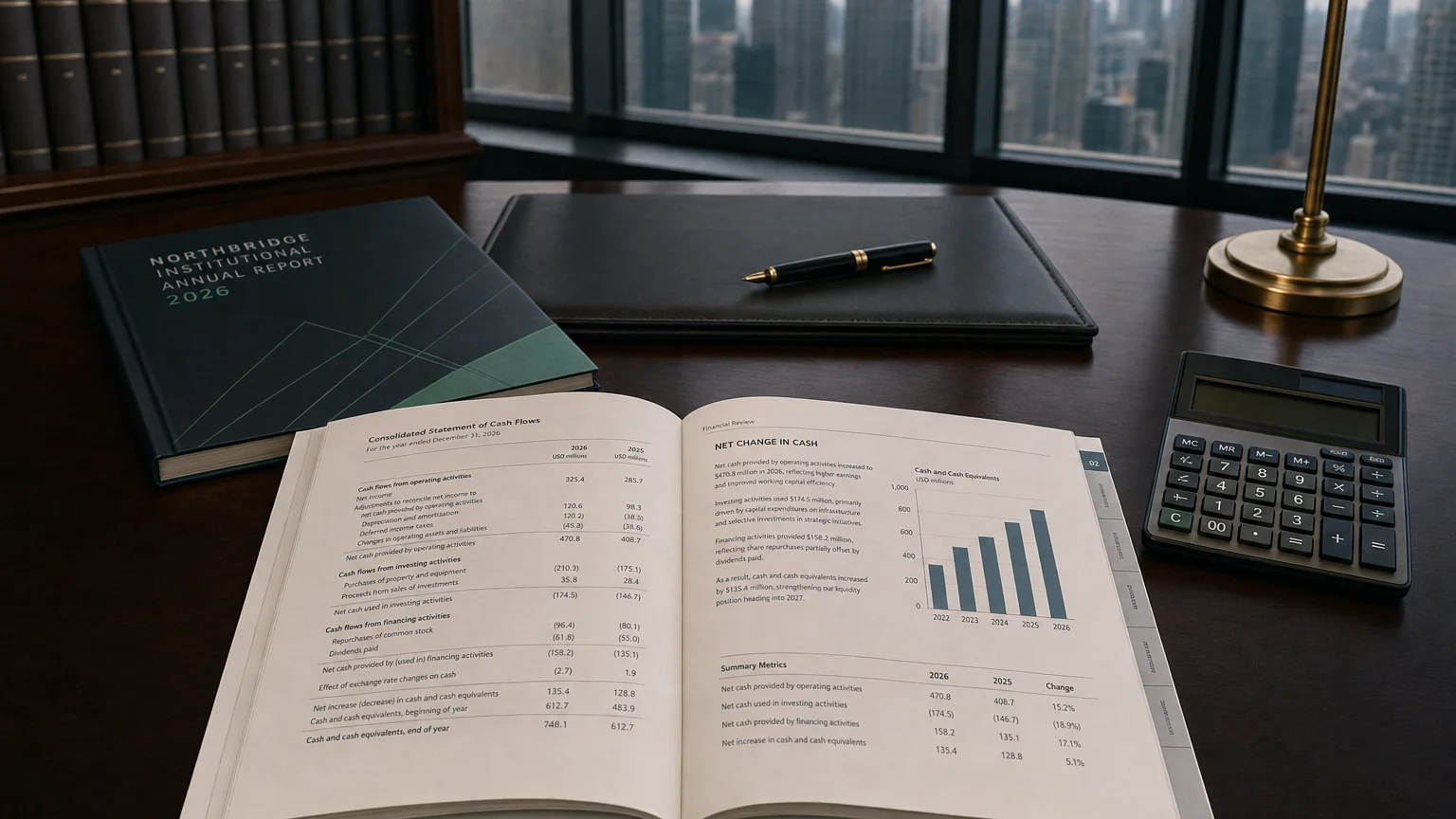

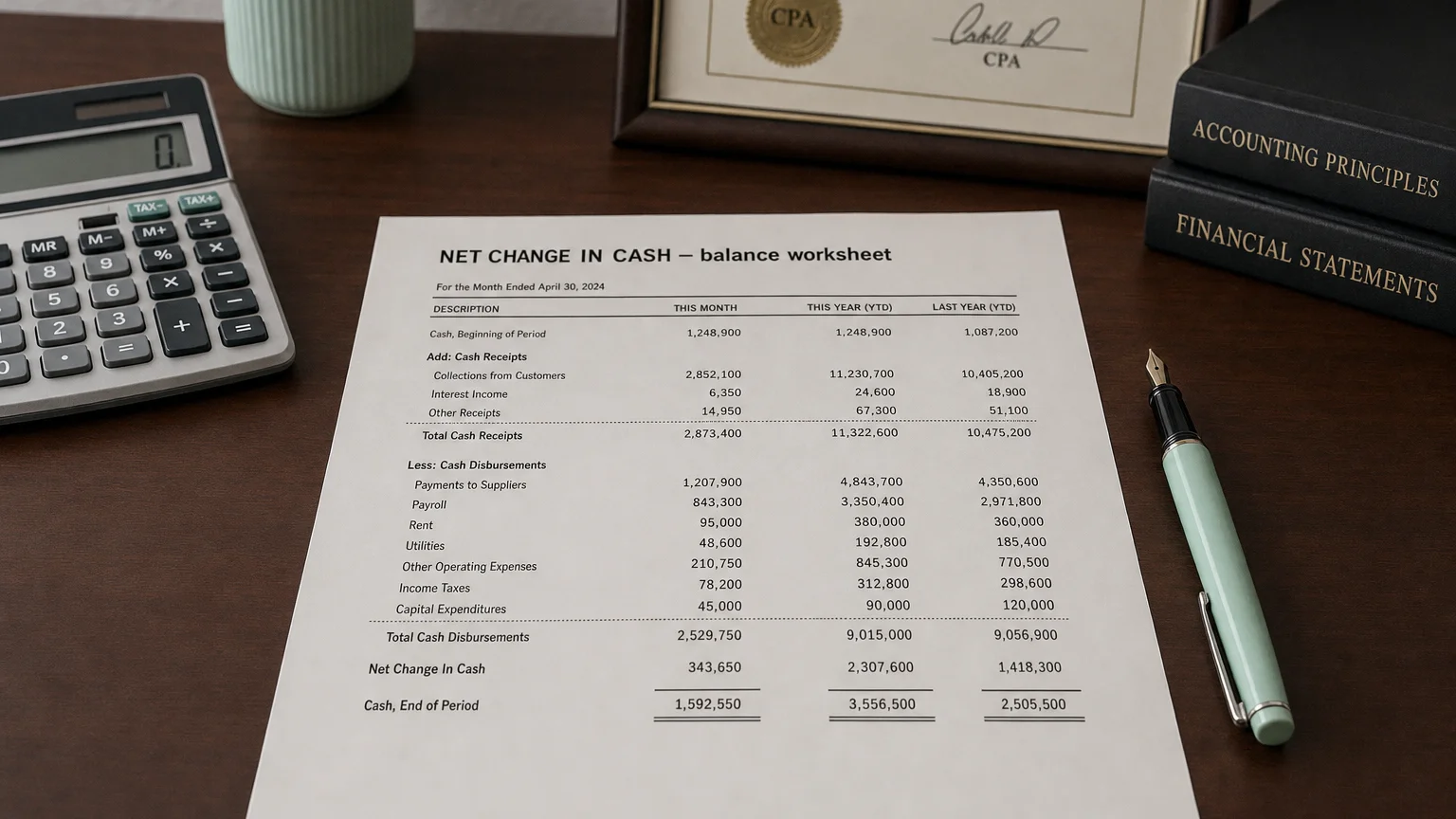

Net change in cash—also called net increase or decrease in cash—equals the sum of cash flows from operating, investing, and financing activities. A positive figure means cash grew during the period; a negative figure means the company consumed more cash than it generated.

In the short run, the market is a voting machine. In the long run, it is a weighing machine.

“Changes in Cash” (often labeled Net Change in Cash or Net Increase/Decrease in Cash and Cash Equivalents) refers to the net increase or decrease in a company’s cash balance over an accounting period. In simple terms, it measures how much the cash and cash equivalents on hand has grown or shrunk during that time. This figure is a key subtotal on the Statement of Cash Flows and reflects how the company’s cash position was affected by its operating, investing, and financing activities. A positive change means the company’s cash increased, while a negative change means its cash decreased.

Calculation and Presentation

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

The net change in cash is calculated by summing the net cash flows from the three core activities of a business. It represents the total of all cash that came into and went out of the company during the period.

Formula:

Where CFO is Cash Flow from Operating Activities, CFI is Cash Flow from Investing Activities, and CFF is Cash Flow from Financing Activities. This figure must also equal the difference between the ending and beginning cash balances for the period, serving as an internal check for the statement’s accuracy.

On the Statement of Cash Flows, this figure is shown near the bottom. After listing the net cash from operating, investing, and financing activities, these three amounts are totaled to produce the “Net Increase (or Decrease) in Cash.” This line is then used to reconcile the beginning and ending cash balances, providing a clear bridge from the start of the period to the end.

The Three Drivers of Cash Changes

The net change in cash is directly driven by the cash flows from the company’s operating, investing, and financing activities. Understanding each component is crucial for proper analysis.

- Operating Activities: Includes cash generated from a company’s core business operations, such as cash from sales minus cash paid for expenses. A positive number here is a sign of a healthy core business.

- Investing Activities: Includes cash used for investments in long-term assets (like purchasing equipment, a negative flow) or cash received from selling those investments (a positive flow).

- Financing Activities: Includes cash received from or paid to investors and creditors. Issuing stock or borrowing money are inflows, while repurchasing stock, repaying loans, and paying dividends are outflows.

Apple Inc. (Fiscal Year 2022)

Apple’s cash flow statement for 2022 showed an “Increase (Decrease) in Cash” of -$$10,952 million. This overall cash decline was the combined result of its activities: a large positive cash inflow from operations was outweighed by significant cash outflows for its investing (e.g., asset purchases) and financing (e.g., massive share buybacks) activities. This shows that even a highly profitable company can see its cash balance decrease due to strategic decisions.

Why the Net Change in Cash Is Important

The net change in cash is a critical indicator of a company’s liquidity, cash management effectiveness, and overall financial health.

- Indicator of Liquidity: At a glance, this figure tells you if the company’s cash pile is growing or shrinking. A consistent decrease in cash might signal potential liquidity issues, whereas a consistent increase provides a greater safety cushion.

- Reflection of Cash Management: It reflects how well management is handling the company’s cash cycle. A large negative change could signal problems like declining sales, heavy expenses, or debt repayments straining cash, prompting further investigation.

- A Reality Check on Profitability: This metric is different from net income. A company can be profitable but have a negative change in cash if it spends heavily on investments or debt repayment. It shows the real-world cash consequence of all business activities, beyond accounting-based profit.

- Guide for Financial Planning: Management uses this trend to guide future decisions. A consistently negative change may force a company to cut costs or seek new funding, while a consistently positive change allows for planning strategic investments, debt reduction, or shareholder returns.

Q · 01What causes a company’s cash balance to decrease overall?+

Q · 02How is net change in cash verified for accuracy?+