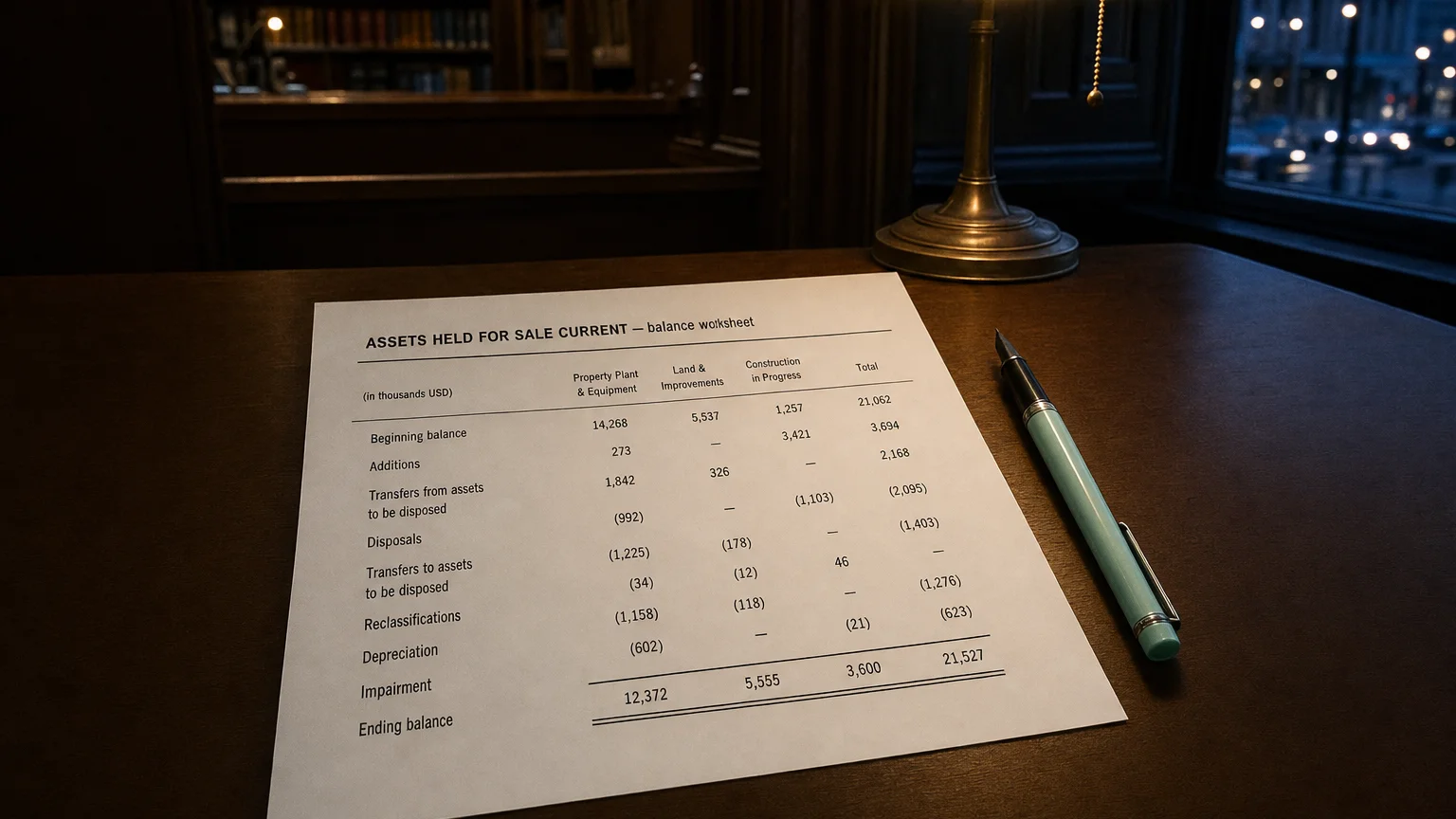

Assets held for sale current are non-current assets committed for divestiture, sale probable within 12 months. Reclassified as current assets on the balance sheet, measured at lower of carrying amount or fair value less costs to sell. Depreciation ceases on reclassification.

Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

Assets Held For Sale Current represent non-current assets (or disposal groups) that a company has committed to sell, with the sale highly probable within 12 months. They are reclassified from their original categories (e.g., PP&E, intangibles) and presented separately as current assets, measured at the lower of carrying amount or fair value less costs to sell.

What It Represents

Assets Held For Sale Current are assets (or groups including liabilities) management has decided to divest. They no longer support ongoing operations and are actively marketed for sale.

- Individual non-current assets (e.g., building, machinery)

- Disposal groups (business segment, subsidiary assets + liabilities)

- Investment properties or intangibles meeting criteria

Reclassification signals strategic shift—divestiture, restructuring, or portfolio cleanup.

Classification Criteria

Strict conditions must be met:

- Available for immediate sale in present condition

- Sale highly probable (committed plan, active marketing)

- Expected completion within one year (extensions possible)

- Management committed—no shopping around

Once met, reclassify even if sale later slips (unless exceptional).

“Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

Measurement Rules

- Lower of carrying amount or fair value less costs to sell

- Impairment loss if FV < carrying (to income, usually)

- No depreciation/amortization while classified

- Subsequent increases limited to prior impairments

Disposal group: Impairment allocated first to goodwill, then pro-rata.

Balance Sheet Presentation

Separate section in current assets:

- ‘Assets Held For Sale Current’

- ‘Assets Classified as Held for Sale’

- No offsetting with related liabilities (separate ‘Liabilities Held for Sale’)

Major classes disclosed on face or in notes.

Common Scenarios

- Divesting non-core business unit

- Selling surplus property or plant

- Spinning off subsidiary

- Restructuring operations

- Responding to regulatory requirements

Analytical Implications

- Upcoming corporate restructuring or portfolio shift

- Potential gain/loss on disposal

- Cleaner view of continuing operations

- Liquidity impact (cash expected soon)

- Impairment signals overvaluation of assets

Adjust ratios (ROA, debt-to-assets) excluding held-for-sale for ongoing performance.

Q · 01What triggers reclassification as assets held for sale?+

Q · 02How are assets held for sale measured on the balance sheet?+

Q · 03Where do assets held for sale appear on the balance sheet?+